Zinc

June 9, 2026

2 min

Zinc

The following content is sponsored by Eloro Resources

Key takeaways

- Critical Mineral Status Renewed: The U.S. Geological Survey retained zinc on its 2025 Critical Minerals List.

- 410,000 Tonnes of New Demand: The IZA forecasts that much extra annual zinc demand from autos and die casting by 2030–2035.

- Batteries Hit Commercial Scale: Zinc batteries reached multi-hundred-MWh orders in 2025, led by Eos Energy's 228 MWh deal with Frontier Power.

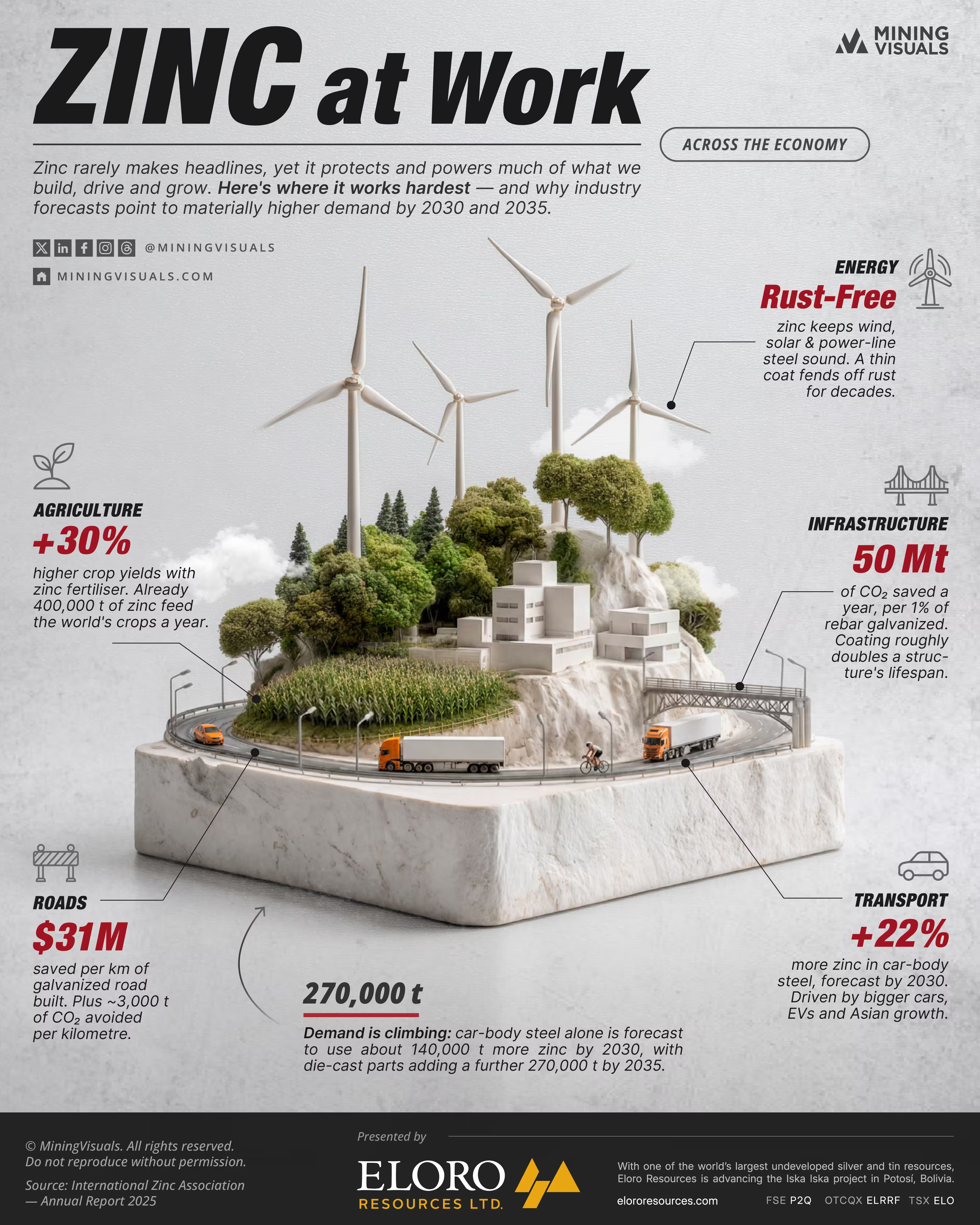

We've covered zinc's role in energy, health, and sustainability before, alongside the supply base concentrated in a handful of mega-mines and the production map that has shifted toward Asia since the mid-1990s. The story of 2025 is what changed on the demand side. In November, the U.S. Geological Survey retained zinc on its final 2025 List of Critical Minerals. At the same time, Fastmarkets reported that the global zinc market stayed tight through 2025, with new demand emerging from stationary energy storage. The structural case stopped being theoretical and started showing up as purchase orders.

Galvanising: The Decarbonisation Numbers

About half of all refined zinc goes into galvanising steel. According to the International Zinc Association's Zinc Enables Decarbonization programme, roughly 50 million tonnes of CO₂ are prevented annually for every 1% of global steel rebar that is galvanised. Building one kilometre of road with galvanised rebar avoids around $31 million in lifetime repair costs and roughly 3,000 tonnes of CO₂, while doubling the road's lifetime costs about 1% of initial construction.

China remains the centre of this demand. Fastmarkets notes that Beijing has committed more than $300 billion to grid modernisation over the past four years, with another $80 to $100 billion earmarked for 2025, and that continued urbanisation under the 15th Five-Year Plan will keep requiring galvanised steel.

Cars, EVs, and Die Casting

The IZA projects a 22% increase in zinc demand for automotive steel by 2030, equating to about 140,000 tonnes of additional zinc per year, driven by larger vehicles, EVs, and growth in China and India. The association's die-casting outlook adds a forecast 17% rise by 2035, or roughly 270,000 tonnes more demand.

These IZA forecasts sit against the near-term market picture. Investing News Network reports that the International Lead and Zinc Study Group projects only around 1% growth in global refined zinc demand in 2026, while Morgan Stanley has set a 2026 average price forecast of $2,900 per tonne against a 2025 LME average of $3,218 per tonne.

Zinc Batteries: From Contender to Customer Orders

The lithium-alternative angle is one we've covered before, but 2025 is when it stopped being theoretical. On 31 October 2025, Eos Energy Enterprises announced a 228 MWh order from UK developer Frontier Power, the first conversion under a previously announced 5 GWh framework agreement. The California Energy Commission followed with a $14 million grant to Pacific Steel Group to deploy a zinc-hybrid storage system at the $630 million Mojave Micro Mill, a zero-emission rebar plant. In India, TechCrunch reports that startup Offgrid Energy Labs closed a $15 million Series A in September 2025 to commercialise its ZincGel chemistry, with a 10 MWh UK demonstration facility planned for Q1 2026.

Lithium-ion still dominates grid storage, but zinc batteries have moved from demonstrators to multi-hundred-MWh purchase orders.

Fertiliser and Yields

The IZA's Zinc Nutrient Initiative reports that zinc-micronutrient fertilisers raise yields by 20 to 30%, and that fertiliser applications already account for 400,000 tonnes of annual zinc demand. A 2025 IZA project in Udaipur, India trained more than 200 farmers, with reported wheat yield gains of 30% and maize gains of 20%. India also cut its Goods and Services Tax on zinc fertilisers from 12% to 5% during the year, lowering the cost barrier for adoption.

The Bottom Line: Structural Demand Meets Cyclical Pressure

Zinc's 2025 was two stories in parallel. The IZA's structural case is one of widening application across EVs, infrastructure, grid batteries, and fertiliser, with the USGS critical-mineral classification underlining the strategic stakes. The cyclical case, told through LME prices and ILZSG projections, is one of near-term oversupply and modest 2026 demand growth as new Chinese smelting capacity comes online. The question heading into 2026 is whether structural demand materialises fast enough to absorb the supply currently entering the market.

Sponsored by:

Eloro Resources Ltd. is a mineral exploration company advancing a world-class silver and tin project in Bolivia’s historic Potosí Department. Its flagship asset, the Iska Iska Project, ranks among the top five undeveloped global resources in terms of scale for both tin and silver.

This significant grassroots discovery remains open in multiple directions, offering substantial potential for continued expansion and resource enhancement. Iska Iska benefits from strong infrastructure access and a deeply rooted presence in Bolivia, supported by an experienced management team and meaningful community engagement.

Eloro’s strategy is focused on resource growth, strategic partnerships, and establishing a leading position within the global mining sector.

Learn more about Eloro Resources at: http://elororesources.com/

Sources:

- USGS — Final 2025 List of Critical Minerals (Federal Register)

- Investing News Network — Zinc Price Forecast: Top Trends for Zinc in 2026

- Fastmarkets — Why the global zinc market remained tight in 2025

- Fastmarkets — Base metals demand outlook under China's 15th Five-Year Plan

- Eos Energy Enterprises Form 8-K (SEC, 31 October 2025)

- California Energy Commission — Long Duration Energy Storage Program

- TechCrunch — India's Offgrid raises $15M to make lithium optional for battery storage

- International Zinc Association — Driving Growth Across Markets: Annual Report 2025

MiningVisuals Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice, nor an offer or solicitation to buy or sell any security or commodity. Always conduct your own research and consult a qualified advisor.

Forward-Looking Statements: This article contains forward-looking information, including zinc demand, price, and commercial deployment projections to 2030 and 2035 attributed to the International Zinc Association, BloombergNEF, the International Lead and Zinc Study Group, Morgan Stanley, and Fastmarkets. Forward-looking statements are based on assumptions and are subject to known and unknown risks and uncertainties; actual results may differ materially from those projected. All figures are sourced from the cited publications and are presented for informational purposes only. Neither MiningVisuals nor the sponsor undertakes any obligation to update forward-looking information.

Explore More

View All

Apple Outweighs Every Listed Miner on Earth, and It Is Not Even the Biggest Company

Apple Outweighs Every Listed Miner on Earth, and It Is Not Even the Biggest Company

One consumer-electronics company is now worth more than every publicly traded mining company on Earth combined. The graphic above captures the June 5 snapshot, when the 317 publicly traded miners tracked by CompaniesMarketCap were worth about $3.48 trillion

Three Weeks Public, SpaceX Already Approaches the Value of Every Listed Miner on Earth

Three Weeks Public, SpaceX Already Approaches the Value of Every Listed Miner on Earth

For 24 years SpaceX stayed private. Then, on June 12, 2026, it began trading on the Nasdaq in the largest IPO in history, priced at a $1.77 trillion valuation. Barely three weeks later the rocket and satellite maker is worth even more. As of early July, SpaceX carried a market capitalization of about $2.1 trillion, the seventh-highest of any public company on Earth, and it joins the Nasdaq-100 on July 7

Lithium Use Cases: Batteries Now Consume 88% of Global Supply

Lithium Use Cases: Batteries Now Consume 88% of Global Supply

In February 2026, the U.S. Geological Survey put a fresh number on a transformation that has been building for a decade: batteries now account for 88% of global lithium end-use, up from 87% a year earlier. The metal that once quietly toughened ceramics and thickened industrial greases has been almost entirely repurposed by the battery economy. As covered in our reporting on the shift from surplus to deficit, the supply side of this story is tightening.

Sort First, Grind Later: The sensor technology reshaping polymetallic processing

Sort First, Grind Later: The sensor technology reshaping polymetallic processing

Sensor-based sorting lets miners reject barren rock before it's ever crushed, saving energy, water, and tailings volume at industrial scale. Polymetallic deposits, the orebodies that carry multiple economically valuable metals in a single rock, present a distinctive processing challenge: the valuable minerals are locked together with each other and with vast volumes of barren rock, demanding both heavy grinding and complex multi-stage separation.