Precious Metals

May 21, 2026

2 min

Precious Metals

The following content is sponsored by The Silver Institute

Key takeaways

- The 2025 Turnaround: Global coin and net bar demand rebounded by 14% to 217.7 Moz, marking the first annual increase in three years.

- Regional Divergence: The 2025 recovery was fueled by a 33% surge in Indian physical investment, while the US market dropped by 46%.

- Strong 2026 Forecast: Demand is projected to grow by an additional 18% in 2026 to reach 257.6 Moz, driven by safe-haven buying and a forecasted 57% recovery in the US.

Silver had a strange year. After two years of investors walking away from the physical market, 2025 saw them come back. Not in a trickle, but in a rush concentrated into the final four months, as prices ripped through one record after another and dealers started rationing inventory.

According to the World Silver Survey 2026, global coin and net bar demand jumped 14% to 217.7 Moz in 2025, the first annual increase since 2022. It happened against a market where liquid silver was getting harder to find. Identifiable bullion inventories actually rose in aggregate, but a growing share was locked up in exchange-traded products (ETPs) or sitting in CME vaults rather than circulating in London. By October the squeeze was visible in the lease rates. Where the ETP story we covered earlier this year tracked institutional vault demand, this is about something different: retail investors physically walking into dealers and buying coins and bars.

What turned the tide? Three things, mostly arriving together. Inventories got tight enough to start showing up in lease rates. Interest rate expectations softened. And from September onwards, with silver clearing $40 and gold pushing through $4,000, a wave of retail money showed up chasing the move. Some of that was value-seeking, silver had lagged gold badly through the first half of the year. Some of it was straightforward fear of missing out.

A Tale of Two Markets: East vs. West

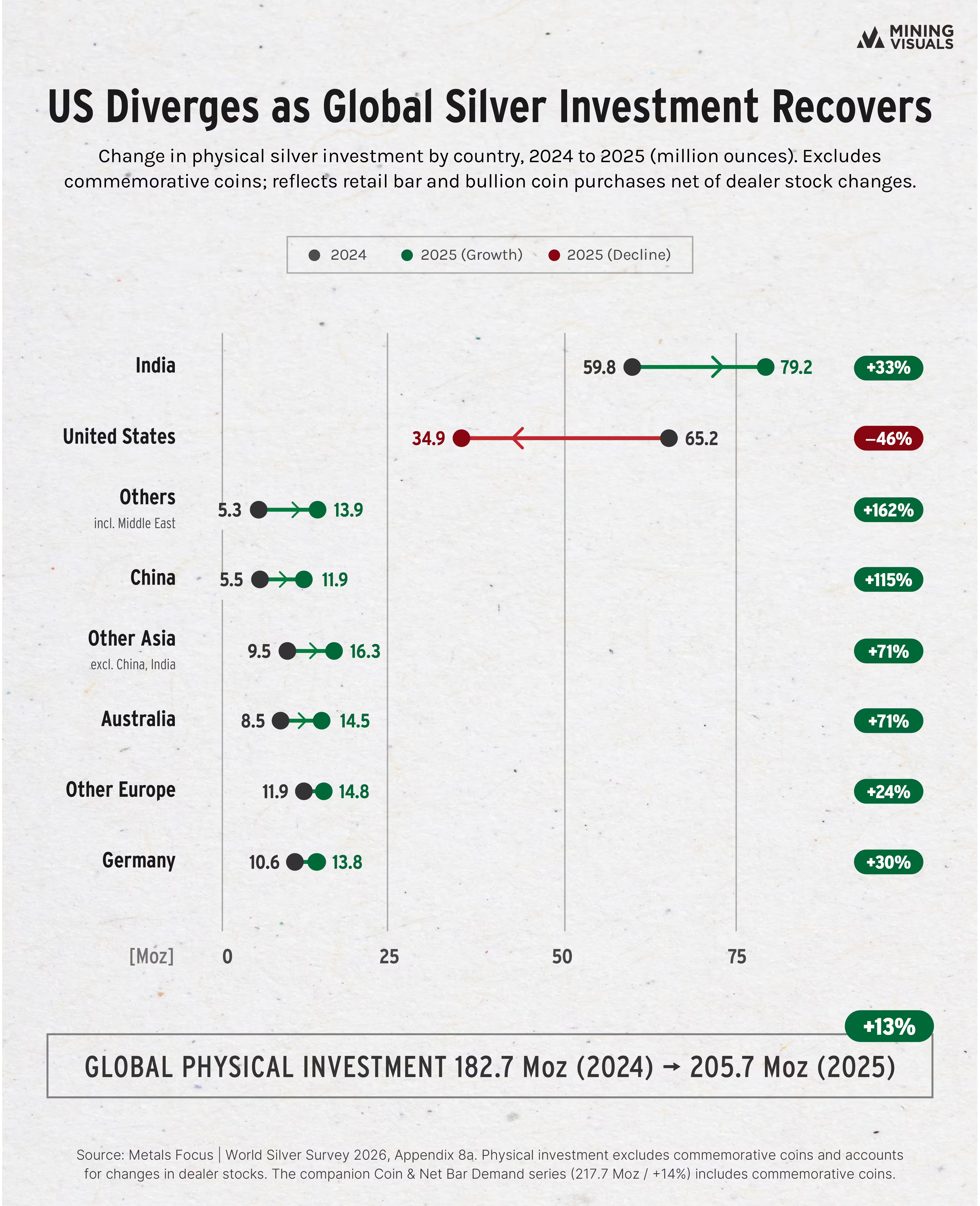

The global rebound masked a sharp geographic split. The 2025 recovery was led by Asia. Indian physical investment rose 33%. Chinese demand more than doubled to 11.9 Moz. Middle East demand tripled to a record 11.4 Moz, with buying showing up in countries like Saudi Arabia, Iran, and Egypt that have historically been gold-only markets.

Meanwhile, in the United States, retail investors did something close to the opposite. US physical investment nearly halved, falling 46% to its lowest level since at least 2010. The Survey's explanation is partly political. Republican-leaning retail investors, who make up a big share of the US silver buyer base, disengaged from precious metals after the election. Partly it's that with prices grinding higher all year, US buyers sold into the rally instead of chasing it.

By Country: Where the Buying Actually Happened

(Country-level data is reported under the "Physical Investment" series, which excludes commemorative coins. The headline 14% / 217.7 Moz figures earlier in this article come from the broader "Coin & Net Bar Demand" series. Both series tell the same story: a 2025 recovery driven by Asia, with the US as a sharp exception.)

The 10-Year Volatility Cycle

Zooming out over the historical surveys, coin and bar demand reveals itself as a highly volatile, sentiment-driven component of the market. Over the last decade, demand has routinely fluctuated between 150 Moz and 340 Moz.

The market reached a 10-year peak of 339.5 Moz in 2022, driven by post-pandemic safe-haven buying and inflation fears. When prices remained high but stagnant through 2023 and 2024, retail demand quickly saturated, retreating to a recent low of 190.9 Moz. The 2025 data confirms that when macroeconomic conditions align, such as rising geopolitical risks and a breakout in spot prices, retail investors aggressively return to physical assets.

The 2026 Outlook

Looking ahead, the momentum established in late 2025 is expected to carry forward. The Silver Institute projects coin and net bar demand will grow by an additional 18% in 2026, reaching 257.6 Moz, the highest level since the 2022 peak.

The growth is expected to be driven by a 57% recovery in the US market, though this only erases 2025's losses rather than reaching prior peaks. Price pullbacks attract bargain hunters and ongoing policy unpredictability reignites the need for portfolio diversification. While industrial demand faces headwinds from technological thrifting, robust physical investment will likely ensure the global silver market remains in a structural deficit throughout the year.

Sponsored by:

The Silver Institute is a global organization dedicated to promoting the use, study, and understanding of silver. It provides in-depth research on silver’s supply, demand, and pricing trends across various industries such as industrial applications, jewelry, investment, and solar energy. One of the institute’s key publications is the World Silver Survey, an annual report that offers detailed statistics and analysis on the global silver market.

For further information, you can visit the official Silver Institute website.

MiningVisuals Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Always conduct your own research.

Sources: World Silver Survey 2026, World Silver Survey 2025, Historical Silver Surveys, Silver Supply & Demand Overview

Explore More

View All

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Somewhere inside a pressurized-water reactor, an alloy that is four-fifths silver is absorbing neutrons to keep the core in check, a job most silver investors have never heard of. It is a useful reminder that the metal people picture as coins and jewelry mostly works elsewhere, across industry.

Ranked: The Countries That Produced the Most Silver in 2025

Ranked: The Countries That Produced the Most Silver in 2025

Mexico remained the world's top silver-producing country in 2025, mining 172.9 million ounces (Moz), roughly a fifth of global supply, according to the World Silver Survey 2026, produced for the Silver Institute by Metals Focus. But Mexico's lead narrowed: its output fell 5% for a third straight year, while second-place Peru climbed 7%. Global mine production rose 3% to 846.6 Moz, even as the ranking's top tier told a story of one leader sliding and its closest rival closing in.

Electric Vehicles Are Set to Become the Auto Industry's Biggest Silver Consumer by 2027

Electric Vehicles Are Set to Become the Auto Industry's Biggest Silver Consumer by 2027

Most of silver's 2026 story has been told from the supply side: a sixth straight year of structural deficit and a record price near $121 in January. Less examined is where the next leg of industrial demand actually comes from. With solar, silver's largest industrial use, now facing thrifting and substitution, the Silver Institute points to a quieter end-use picking up the slack: the automotive sector. A December 2025 study from Oxford Economics and the Silver Institute quantifies that shift, and the engine behind it is the electric vehicle.

Silver Market Balance: A 2026 Update

Silver Market Balance: A 2026 Update

For the fifth year running, the world used more silver than it produced in 2025, and the World Silver Survey 2026 expects 2026 to extend that streak to six. The report, released in April by the Silver Institute and researched by the London consultancy Metals Focus, pegs the 2025 deficit at 40.3 million ounces and forecasts a wider gap of 46.3 million ounces this year. Each shortfall draws on above-ground stocks, leaving less metal readily available even as total inventories have held up.