Precious Metals

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

THE METAL KEEPING AI SERVERS FROM MELTING IS ONE THE U.S. MOSTLY IMPORTS.

The following content is sponsored by Outcrop Silver

In early 2026, the four largest hyperscalers (Amazon, Microsoft, Alphabet, and Meta) guided toward roughly $725 billion in capital spending for the year, up about 77% from 2025, most of it flowing into AI data centers. That build-out has hit a physical wall: power and heat. Every watt pushed through a densely packed AI rack must be delivered efficiently and moved away as heat, and the metal that does both jobs best is silver. A December 2025 report from The Silver Institute, researched by Oxford Economics, names data centers and AI as one of three structural growth pillars for industrial silver over the next five years, alongside solar and EVs. It is the newest leg of a demand story this publication has tracked through solar, EVs, and silver's addition to the U.S. critical minerals list.

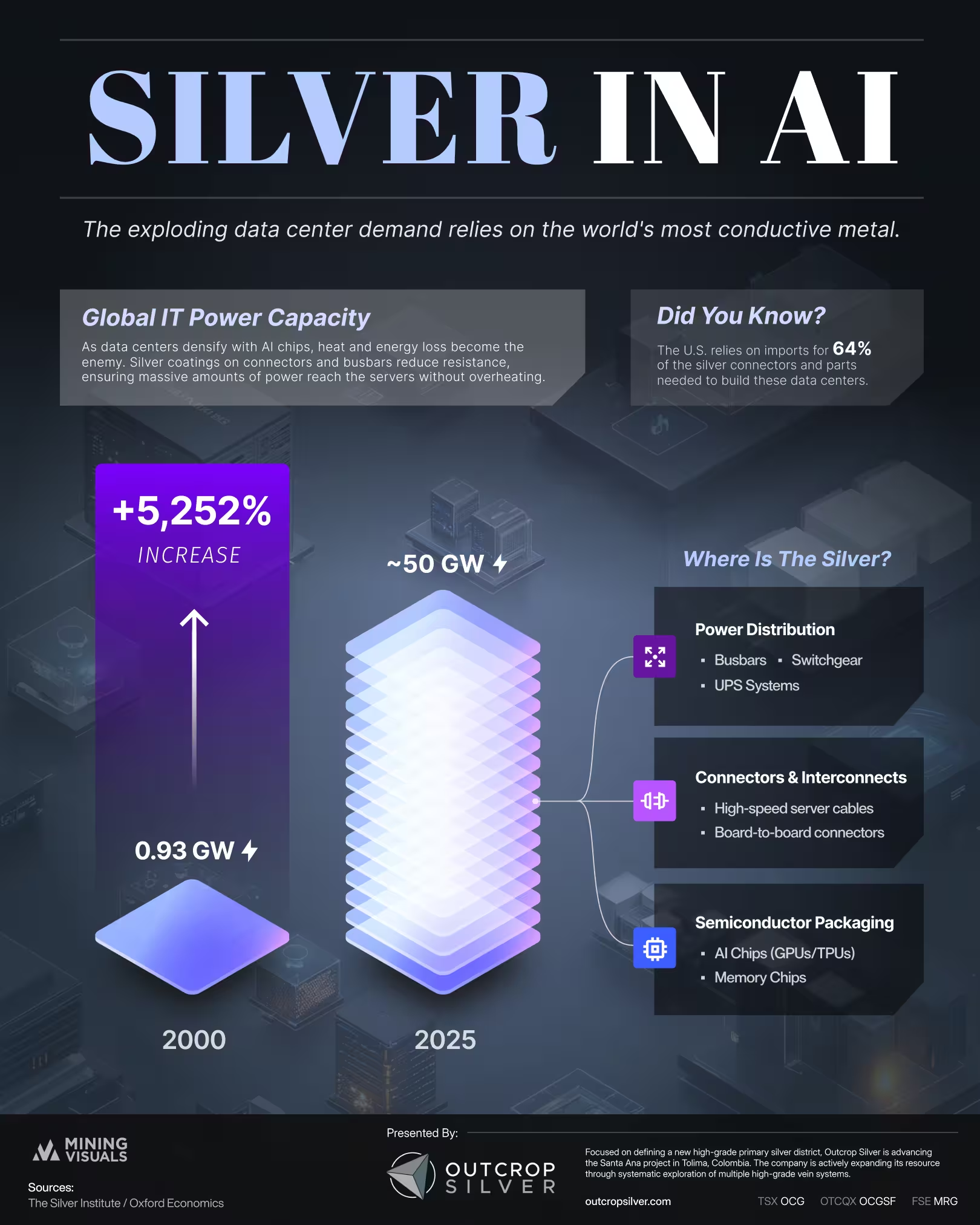

The figure anchoring this story is the growth in global IT power capacity, from 0.93 GW in 2000 to nearly 50 GW in 2025. The Silver Institute is explicit about why it leans on this number: there is an absence of precise silver-loading data per facility, so power capacity serves as the proxy, since more installed compute means more servers, interconnects, and power hardware, and consequently more silver.

What the chart does not show is how recent and steep the acceleration is. U.S. data center construction spending reached a monthly rate of $45.1 billion by December 2025, up 85% in two years, and a meaningful share of planned 2026 capacity is expected to slip because grid interconnection and construction cannot keep pace. The bottleneck has shifted from software to the physical plant, the layer where silver lives.

On the two properties that matter most inside a data center, silver is the best available material. It holds the highest electrical conductivity of any metal, minimizing the resistive losses that turn delivered power into waste heat, and the highest thermal conductivity, around 429 W/m·K, roughly 7% better than copper, which pulls heat away from the working silicon in GPUs and TPUs. That edge looks small on a spec sheet, but in facilities that cannot tolerate downtime and where cooling already consumes a large share of the energy budget, the marginal metal that cuts both loss and heat is difficult to design out.

It also appears at three levels. At the power distribution layer, silver routes bulk electricity through busbars, switchgear, and UPS systems while resisting the oxidation and arc erosion that degrade high-current contacts. At the connector layer, silver-plated cabling holds low contact resistance at the data rates AI clusters run on. At the semiconductor packaging layer, it binds chips and helps draw heat from GPUs and TPUs. Three different jobs, one element, is what makes the demand hard to displace: substitution is not one decision but many.

The build-out runs into a supply question the U.S. has only recently treated as strategic. According to USGS data, the country imported 64% of the silver it consumed in 2024. It is worth being precise: this is net import reliance for silver as a commodity, the same metal that goes into server boards, not a count of finished components. Visual Capitalist, drawing on the USGS "Key Minerals in Data Centers" analysis, places silver at that 64% level alongside tin at 73% for the server-board category.

That dependency is why silver's November 2025 addition to the USGS critical minerals list, which expanded to 60 minerals, matters here. The data center is the concrete illustration: the country leading the global AI build-out relies on imports for most of a metal embedded in the hardware that build-out requires. Set against the multi-year structural deficit already established in this market, the import reliance is a constraint to manage, not a solved problem.

Outcrop Silver is a leading explorer and developer focused on advancing its flagship Santa Ana high-grade silver project in Colombia. Leveraging a disciplined and seasoned team of professionals with decades of experience in the region. Outcrop Silver is dedicated to expanding current mineral resources through strategic exploration initiatives.

At the core of our operations is a commitment to responsible mining practices and community engagement, underscoring our approach to sustainable development. Our expertise in navigating complex geological and market conditions enables us to consistently identify and capitalize on opportunities to enhance shareholder value.

With a deep understanding of the Colombian mining landscape and a track record of successful exploration, Outcrop Silver is poised to transform the Santa Ana project into a significant silver producer, contributing positively to the local economy and setting new standards in the mining industry.

Learn more about Outcrop Silver at https://outcropsilver.com/

MiningVisuals Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice.

Somewhere inside a pressurized-water reactor, an alloy that is four-fifths silver is absorbing neutrons to keep the core in check, a job most silver investors have never heard of. It is a useful reminder that the metal people picture as coins and jewelry mostly works elsewhere, across industry.

Mexico remained the world's top silver-producing country in 2025, mining 172.9 million ounces (Moz), roughly a fifth of global supply, according to the World Silver Survey 2026, produced for the Silver Institute by Metals Focus. But Mexico's lead narrowed: its output fell 5% for a third straight year, while second-place Peru climbed 7%. Global mine production rose 3% to 846.6 Moz, even as the ranking's top tier told a story of one leader sliding and its closest rival closing in.

Most of silver's 2026 story has been told from the supply side: a sixth straight year of structural deficit and a record price near $121 in January. Less examined is where the next leg of industrial demand actually comes from. With solar, silver's largest industrial use, now facing thrifting and substitution, the Silver Institute points to a quieter end-use picking up the slack: the automotive sector. A December 2025 study from Oxford Economics and the Silver Institute quantifies that shift, and the engine behind it is the electric vehicle.

For the fifth year running, the world used more silver than it produced in 2025, and the World Silver Survey 2026 expects 2026 to extend that streak to six. The report, released in April by the Silver Institute and researched by the London consultancy Metals Focus, pegs the 2025 deficit at 40.3 million ounces and forecasts a wider gap of 46.3 million ounces this year. Each shortfall draws on above-ground stocks, leaving less metal readily available even as total inventories have held up.