Copper

June 1, 2026

2 min

Copper

Key takeaways

- A New All-Time High. Copper futures on the COMEX touched an intraday record of $6.71 per pound on May 13, 2026, with the metal up roughly 35% year-on-year as the May monthly close shaped up to be the highest on record.

- One Mine, One Quarter of the Deficit. Freeport-McMoRan's Grasberg force majeure has already cost the market about 525,000 tonnes of supply across 2025 and 2026 per Goldman Sachs, turning a projected surplus into a deficit almost overnight.

- Tariffs Reshape the Trade Map. 50% Section 232 tariffs on semi-finished copper took effect on August 1, 2025, with refined copper still under review for a phased tariff that could begin January 2027.

Copper has spent most of 2026 doing something it had not done in a quarter century: setting fresh records every few weeks. The COMEX contract printed an intraday all-time high of $6.71 per pound on May 13, and the May monthly close looks set to land at the top of the historical chart. In London, copper traded above $14,000 per tonne in mid-May, touching $14,196.50, within reach of the LME's January 29 record of $14,527.50.

Three forces have converged on the copper market over the past twelve months: AI infrastructure demand, an acute supply incident at Grasberg, and the introduction of US Section 232 tariffs. The sections below cover each in turn.

AI Is the New Demand Accelerant

The newest leg of the bull case is also the most concentrated. Per Bloomberg Intelligence, AI-ready data centers consume between 27 and 33 tonnes of copper per megawatt of applied power, and North American build-out alone could add 1.1 to 2.4 million tonnes of demand by 2030. As covered in The 17.9-Year Lag, a single hyperscale AI facility can require up to 50,000 tonnes of copper, and the timing mismatch with new mine development (18 to 23 months versus 17.9 years on average) is the structural problem driving the deficit thesis.

The Grasberg Shock

The acute trigger came on September 8, 2025, when 800,000 tonnes of wet material rushed into Freeport-McMoRan's Grasberg Block Cave in Indonesia. Freeport declared force majeure on September 24 and guided 2026 production at the world's second-largest copper mine to be 35% below prior estimates, with full recovery not expected before 2027. Goldman Sachs subsequently estimated a 525,000-tonne supply loss across 2025 and 2026, flipping the 2025 balance from a 105,000-tonne surplus to a 55,500-tonne deficit. The ICSG now officially forecasts a 150,000-tonne deficit for 2026, the first structural shortage since 2009.

Tariffs Reshape the Map

On July 30, 2025, the Trump administration issued a Section 232 proclamation imposing a 50% tariff on the copper input value of semi-finished and intensive derivative products, effective August 1. Refined copper, ores, and scrap remain exempt for now. A Commerce Department update is due to the President by June 30, 2026, and could trigger a phased universal duty on refined copper, starting at 15% from January 1, 2027 and rising to 30% a year later. According to the Council on Foreign Relations, the United States imports roughly 45% of its copper, led by Mexico, China, and Canada.

Final Synthesis: The Other View, and What to Watch

Not every analyst is positioned for the rally to continue. Goldman Sachs Research expects copper prices to decline somewhat in 2026 from recent records, and S&P Global cites StoneX's Natalie Scott-Gray noting that LME net longs are approaching record levels while Chinese traders sit at their widest net-short since 2021.

Three upcoming developments are scheduled to shape the rest of 2026: the Commerce Department's June 30, 2026 report on refined copper, which will inform any phased tariff on cathode imports; Freeport's phased Grasberg ramp-up through 2026 and 2027, which will determine how much of the 525,000-tonne supply loss returns to the market; and ongoing signals from Chinese physical demand, where S&P Global cites StoneX flagging LME positioning approaching record levels alongside the widest Chinese net-short position since 2021.

MiningVisuals Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Always conduct your own research.

Sources: Trading Economics, Investing News Network, Bloomberg, Bloomberg Intelligence, Mining.com, Reuters via Yahoo Finance, Goldman Sachs Research, White & Case, Council on Foreign Relations, Fastmarkets, S&P Global, MiningVisuals: Copper Market Balance, MiningVisuals: The 17.9-Year Lag.

Explore More

View All

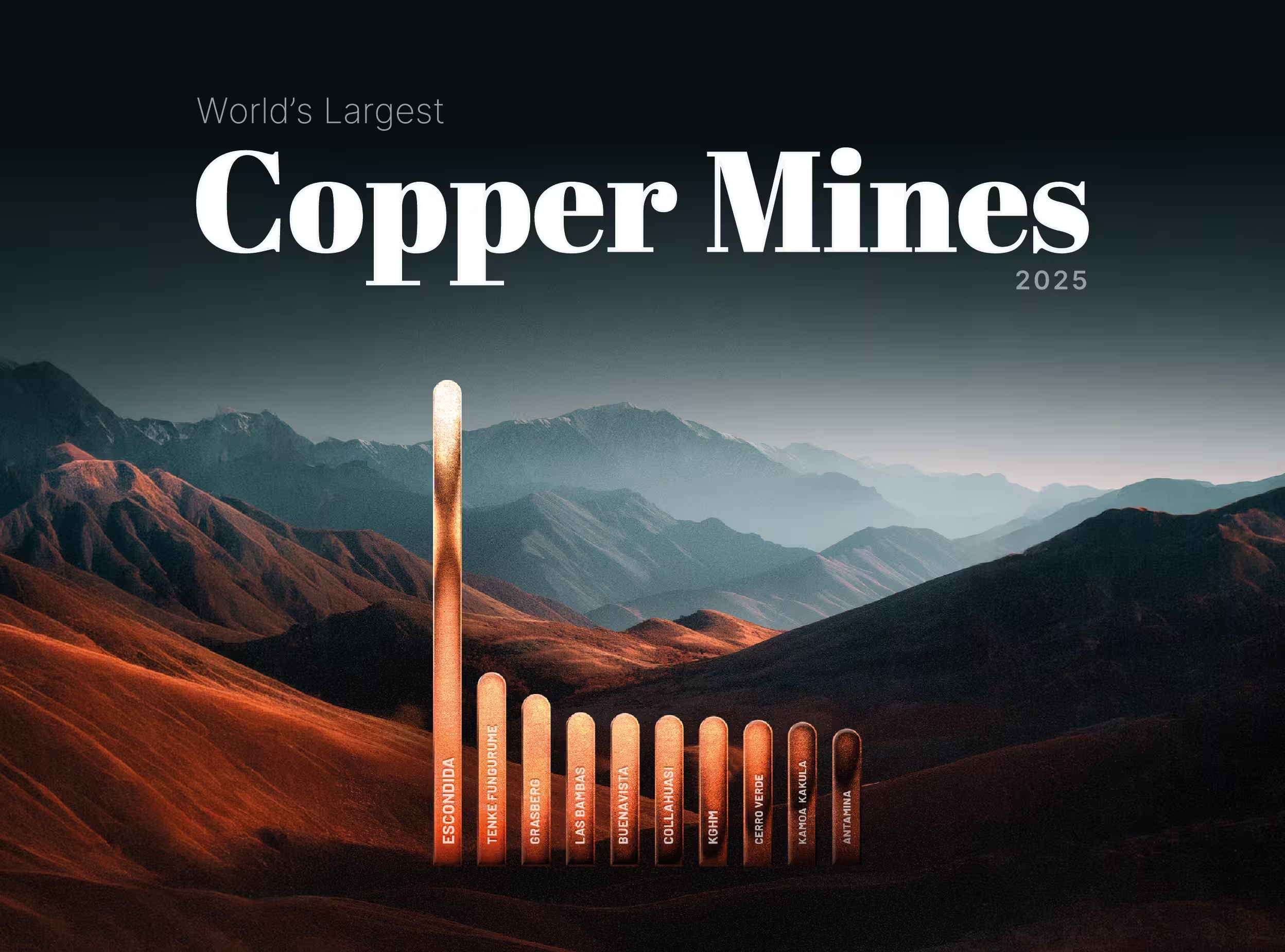

Ranked: The World's Largest Copper Mines (2025)

Ranked: The World's Largest Copper Mines (2025)

Copper has spent 2026 setting records, touching an intraday COMEX high of $6.71 per pound on May 13 amid AI-driven demand and supply shocks, against a backdrop where the ICSG now forecasts a 150,000-tonne deficit for 2026. In a market this tight, where the deficit thesis turns on lost tonnes, the question of where the world's copper actually comes from carries unusual weight.

The Cost of Mining Copper: A 2024–2025 Update

The Cost of Mining Copper: A 2024–2025 Update

Copper futures touched an all-time high above $6.58 per pound on May 12, 2026, capping a 40.86% gain over the prior twelve months as supply tightness collided with structural demand from grid build-out, electric vehicles, and AI data centers. Earlier in the year, the LME benchmark rallied 22% to a record $13,387 per tonne on January 6, 2026. Behind the price action lies a less-discussed story: what it actually costs the world's largest miners to pull a pound of copper out of the ground.

Copper Production Q4 2025

Copper Production Q4 2025

As power-hungry AI data centers drive a projected 2-million-ton surge in global copper demand by 2030, market attention remains fixated on the supply side. Fourth-quarter 2025 metrics provide a definitive look at how the world's top miners closed out the year. While overall volumes remain heavily concentrated among a few historic industry giants, the true Q4 narratives emerged further down the list, as mid-tier producers leveraged flagship asset expansions to hit multi-year highs and offset the sector's ongoing struggle with declining ore grades.

Copper Market Balance: A Look at 2026 Deficit Forecasts

Copper Market Balance: A Look at 2026 Deficit Forecasts

For years, analysts modeling the global copper market were comforted by a reliable buffer of surplus supply. But as our latest data visualization reveals, that cushion has violently evaporated. The International Copper Study Group (ICSG) has officially abandoned its projected surplus for 2025 to officially forecast a 150,000-metric-ton deficit for 2026—the market's first structural shortage since 2009. Wall Street is bracing for an even harsher reality.