Copper

March 25, 2026

1 min

Copper

Key takeaways

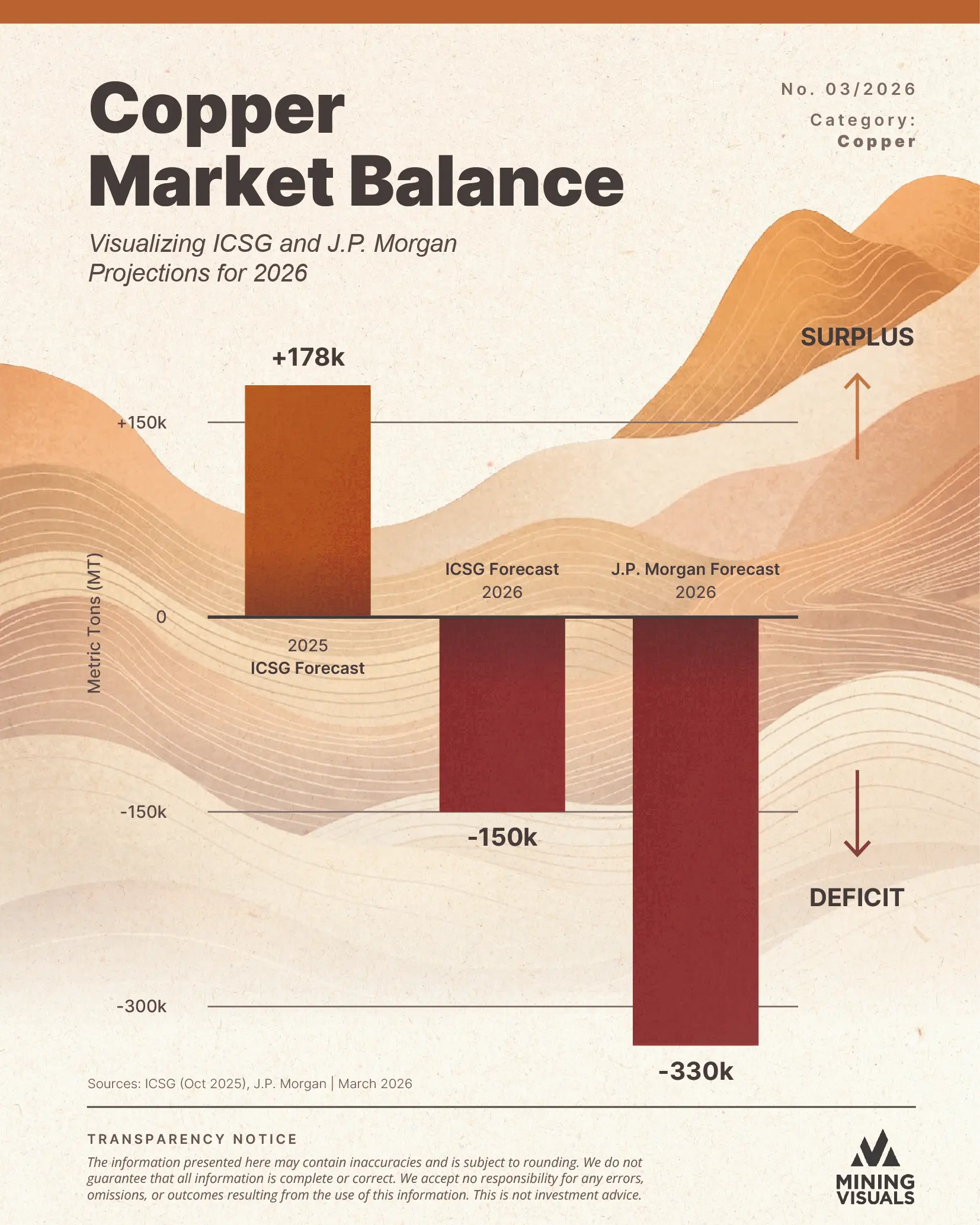

- The ICSG Reverses Course: The International Copper Study Group has abandoned its previous surplus projections, now officially forecasting a 150,000 metric ton copper deficit for 2026.

- AI Demand Deepens the Deficit: J.P. Morgan projects an even steeper 330,000 metric ton shortfall, driven heavily by the massive material demands of new hyperscale data centers.

- Supply Continues to Stumble: Global production is struggling to keep pace, weighed down by prolonged mine closures and downgraded output guidance from major operations in Chile.

For years, analysts modeling the global copper market were comforted by the expectation of a reliable buffer of surplus supply. But as our latest data visualization reveals, market balance forecasts show a sharp shift from a projected surplus to a deficit in 2026. The International Copper Study Group (ICSG) has officially abandoned its projected surplus for 2025, now forecasting a 150,000-metric-ton deficit for 2026—pointing to the market's first structural shortage since 2009. Wall Street is bracing for an even harsher reality. J.P. Morgan's models push the anticipated shortfall to a staggering 330,000 metric tons. Driven by an unprecedented surge in hyperscale AI infrastructure and cascading mine closures, this massive shift in the outlook from green to red has already pushed current prices to historic highs, signaling that the era of abundant copper may be definitively over.

J.P. Morgan’s Deep Deficit

The deepest bar on the chart, the 330,000 MT deficit, belongs to J.P. Morgan's forward models. This steep drop is largely tied to a sudden change in global computing infrastructure.

J.P. Morgan estimates data centers will siphon approximately 475,000 metric tons of copper in 2026. The Copper Development Association notes that new hyperscale AI facilities—housing advanced, power-dense systems like Nvidia's HGX, require up to 50,000 tons each. This highly concentrated, novel source of demand is dragging the global balance sheet deep into the negative.

The Supply-Side Collapse

A structural deficit requires both rising demand and failing supply. The red and orange bars on our chart are essentially locked into place by ongoing operational failures across the global mining sector.

Compounding this projected deficit, the Grasberg Block Cave remains shuttered under force majeure until Q2 2026, removing critical tonnage from the market. Furthermore, Anglo American's recent Q4 2025 downgrade for its Chile operations (dropping guidance to 390,000–420,000 tonnes) underscores just how problematic replacing lost production has become. This operational reality persists even as Cochilco reports a seemingly stable overall baseline of ~5.5 million tonnes from Chile in 2024–2025, proving that top-line stability can mask underlying supply fragility.

Final Synthesis

While a 150k to 330k MT deficit represents only ~0.5% to 1.1% of a 28.7 million ton global market, commodity pricing is ruthlessly dictated by the margins. In physical markets with inelastic demand, the "marginal ton" of supply determines the price for the entire market; therefore, even a minor structural deficit typically triggers a disproportionate surge in spot prices to balance the books.

MiningVisuals Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice.

Explore More

View All

Ranked: The World's Largest Copper Mines (2025)

Ranked: The World's Largest Copper Mines (2025)

Copper has spent 2026 setting records, touching an intraday COMEX high of $6.71 per pound on May 13 amid AI-driven demand and supply shocks, against a backdrop where the ICSG now forecasts a 150,000-tonne deficit for 2026. In a market this tight, where the deficit thesis turns on lost tonnes, the question of where the world's copper actually comes from carries unusual weight.

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper has spent most of 2026 doing something it had not done in a quarter century: setting fresh records every few weeks. The COMEX contract printed an intraday all-time high of $6.71 per pound on May 13, and the May monthly close looks set to land at the top of the historical chart. In London, copper traded above $14,000 per tonne in mid-May, touching $14,196.50, within reach of the LME's January 29 record of $14,527.50.

The Cost of Mining Copper: A 2024–2025 Update

The Cost of Mining Copper: A 2024–2025 Update

Copper futures touched an all-time high above $6.58 per pound on May 12, 2026, capping a 40.86% gain over the prior twelve months as supply tightness collided with structural demand from grid build-out, electric vehicles, and AI data centers. Earlier in the year, the LME benchmark rallied 22% to a record $13,387 per tonne on January 6, 2026. Behind the price action lies a less-discussed story: what it actually costs the world's largest miners to pull a pound of copper out of the ground.

Copper Production Q4 2025

Copper Production Q4 2025

As power-hungry AI data centers drive a projected 2-million-ton surge in global copper demand by 2030, market attention remains fixated on the supply side. Fourth-quarter 2025 metrics provide a definitive look at how the world's top miners closed out the year. While overall volumes remain heavily concentrated among a few historic industry giants, the true Q4 narratives emerged further down the list, as mid-tier producers leveraged flagship asset expansions to hit multi-year highs and offset the sector's ongoing struggle with declining ore grades.