Copper

February 2, 2026

3 min

Copper

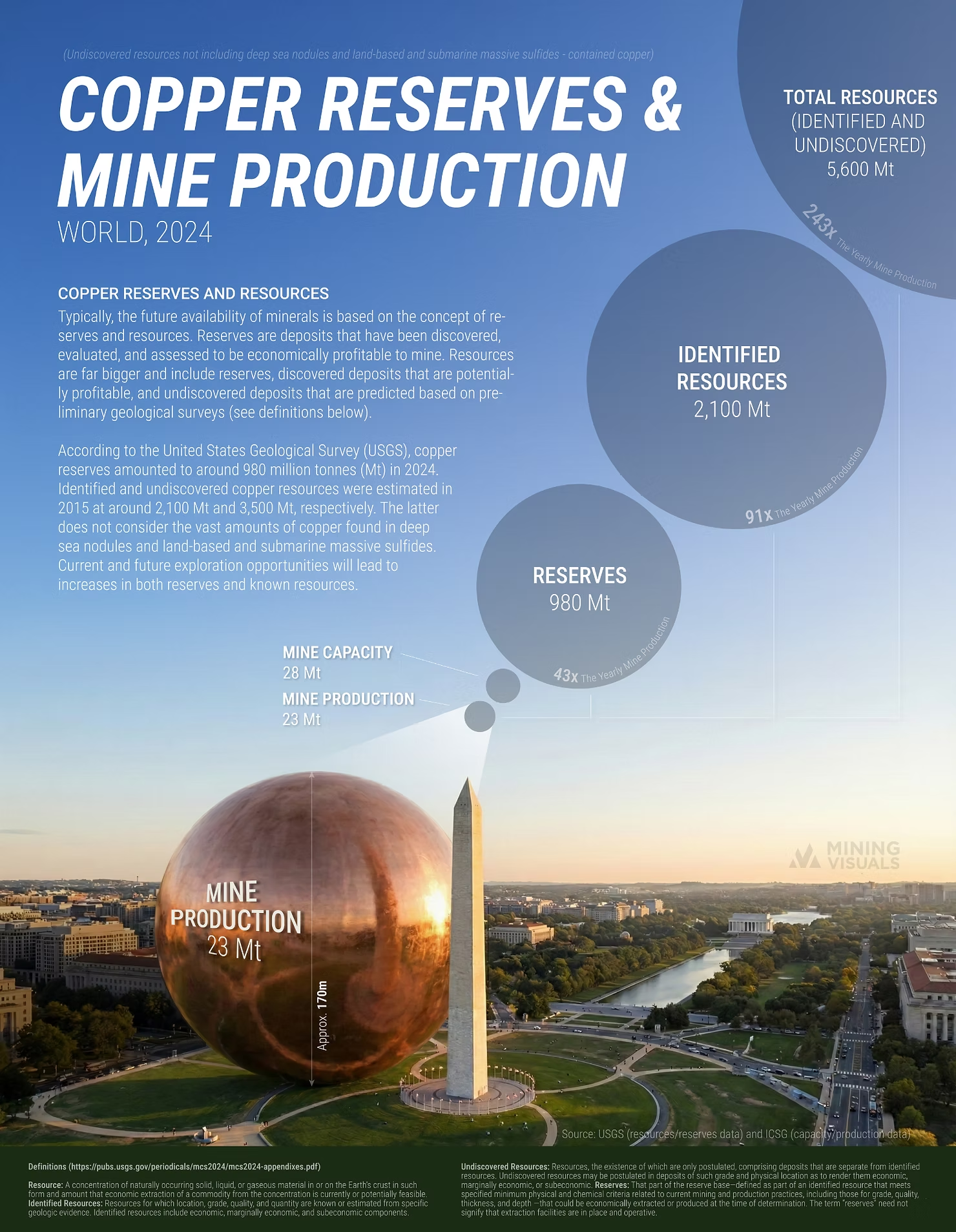

The global copper market presents a striking contradiction: we possess enough copper to sustain humanity for centuries, yet the industry warns of looming deficits. The answer lies in the massive gap between geological abundance and economic availability.

To understand this, one must distinguish between "Resources" (what exists in the Earth) and "Reserves" (deposits profitable to mine today). According to the International Copper Study Group (ICSG), total identified and undiscovered resources amount to 5,600 million tonnes (Mt) . With annual mine production at just 23 Mt, the world holds roughly 243 times more copper in the ground than we extract each year. Even focusing strictly on identified resources, there are 2,100 Mt available.

Table 1: The Geological vs. Economic Reality

The Dynamic Nature of Supply

A common fallacy is dividing current reserves by annual production to conclude we have only ~40 years of supply left. Historical data refutes this; since 1960, the world has consistently maintained about 40 years of reserves despite rising demand.

Reserves are dynamic. As exploration and technology advance, resources are continually upgraded into "bankable" reserves. Between 2000 and 2024, the world mined 441 Mt of copper, yet global reserves actually grew by 547 Mt . We are finding viable copper faster than we are extracting it.

Why Access is the Real Bottleneck

The "supply crunch" stems from operational hurdles, not geological scarcity. Converting resources into active production is increasingly difficult due to declining ore grades in mature regions like the U.S. and Chile, which require moving more rock for the same metal output. Environmental factors compound these challenges, as many large deposits are in water-scarce regions where securing water rights is critical. Additionally, complex permitting and political risks have significantly lengthened the timeline for bringing new supply online.

The Demand Super-Cycle

These supply constraints collide with a demand "super-cycle" driven by the clean energy transition. Technologies essential for decarbonization are far more material-intensive than fossil-fuel counterparts. Infrastructure for renewables and grid expansion relies heavily on copper for conductivity, while the shift to electric vehicles (EVs) is a major driver of new consumption.

Table 2: Copper Intensity in Vehicle Electrification

[Source: International Copper Association via Copper.org]

The "Urban Mine" Solution

To bridge the gap, the market turns to the circular economy. Copper can be recycled infinitely without performance loss. This "Urban Mine" of scrap metal already meets about one-third of global usage. Beyond supply, recycling offers immense efficiency, requiring up to 85% less energy than mining new ore.

The Bottom Line

We are not running out of copper. The challenge is not geological scarcity, but the economic and logistical feat of unlocking these resources, through timely mine development and enhanced recycling, to meet the soaring demands of an electrified future.

Sources & Further Reading

Primary Data:

- International Copper Study Group (ICSG): The World Copper Factbook 2025. This annual publication provides the core statistics on global production, refining, and recycling capacities used throughout this article.

- U.S. Geological Survey (USGS): Mineral Commodity Summaries 2024 & 2025. The primary source for global geological reserves, identified resources, and production estimates.

Market Analysis & Forecasts:

- International Energy Agency (IEA): Global Critical Minerals Outlook 2025. Provides data on long-term demand scenarios (STEPS, APS) driven by the energy transition, including EV and grid requirements.

- BHP Insights: How Copper Will Shape Our Future. Analysis on the "Urban Mine," recycling energy intensity (85% savings), and the specific impact of data centers on future demand.

- S&P Global Market Intelligence / IEA: Industry benchmarks regarding the ~17-year average lead time from discovery to production for new mines.

- EY / Mining.com: Reports on operational headwinds, including water stress in major mining regions like Chile and Peru, and the increasing complexity of environmental permitting.

Explore More

View All

Ranked: The World's Largest Copper Mines (2025)

Ranked: The World's Largest Copper Mines (2025)

Copper has spent 2026 setting records, touching an intraday COMEX high of $6.71 per pound on May 13 amid AI-driven demand and supply shocks, against a backdrop where the ICSG now forecasts a 150,000-tonne deficit for 2026. In a market this tight, where the deficit thesis turns on lost tonnes, the question of where the world's copper actually comes from carries unusual weight.

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper has spent most of 2026 doing something it had not done in a quarter century: setting fresh records every few weeks. The COMEX contract printed an intraday all-time high of $6.71 per pound on May 13, and the May monthly close looks set to land at the top of the historical chart. In London, copper traded above $14,000 per tonne in mid-May, touching $14,196.50, within reach of the LME's January 29 record of $14,527.50.

The Cost of Mining Copper: A 2024–2025 Update

The Cost of Mining Copper: A 2024–2025 Update

Copper futures touched an all-time high above $6.58 per pound on May 12, 2026, capping a 40.86% gain over the prior twelve months as supply tightness collided with structural demand from grid build-out, electric vehicles, and AI data centers. Earlier in the year, the LME benchmark rallied 22% to a record $13,387 per tonne on January 6, 2026. Behind the price action lies a less-discussed story: what it actually costs the world's largest miners to pull a pound of copper out of the ground.

Copper Production Q4 2025

Copper Production Q4 2025

As power-hungry AI data centers drive a projected 2-million-ton surge in global copper demand by 2030, market attention remains fixated on the supply side. Fourth-quarter 2025 metrics provide a definitive look at how the world's top miners closed out the year. While overall volumes remain heavily concentrated among a few historic industry giants, the true Q4 narratives emerged further down the list, as mid-tier producers leveraged flagship asset expansions to hit multi-year highs and offset the sector's ongoing struggle with declining ore grades.