Copper

January 27, 2026

3 min

Copper

In the current industrial landscape, significant attention is paid to where resources are mined. However, a critical component of the supply chain lies in the processing stage, where raw ores are converted into usable materials.

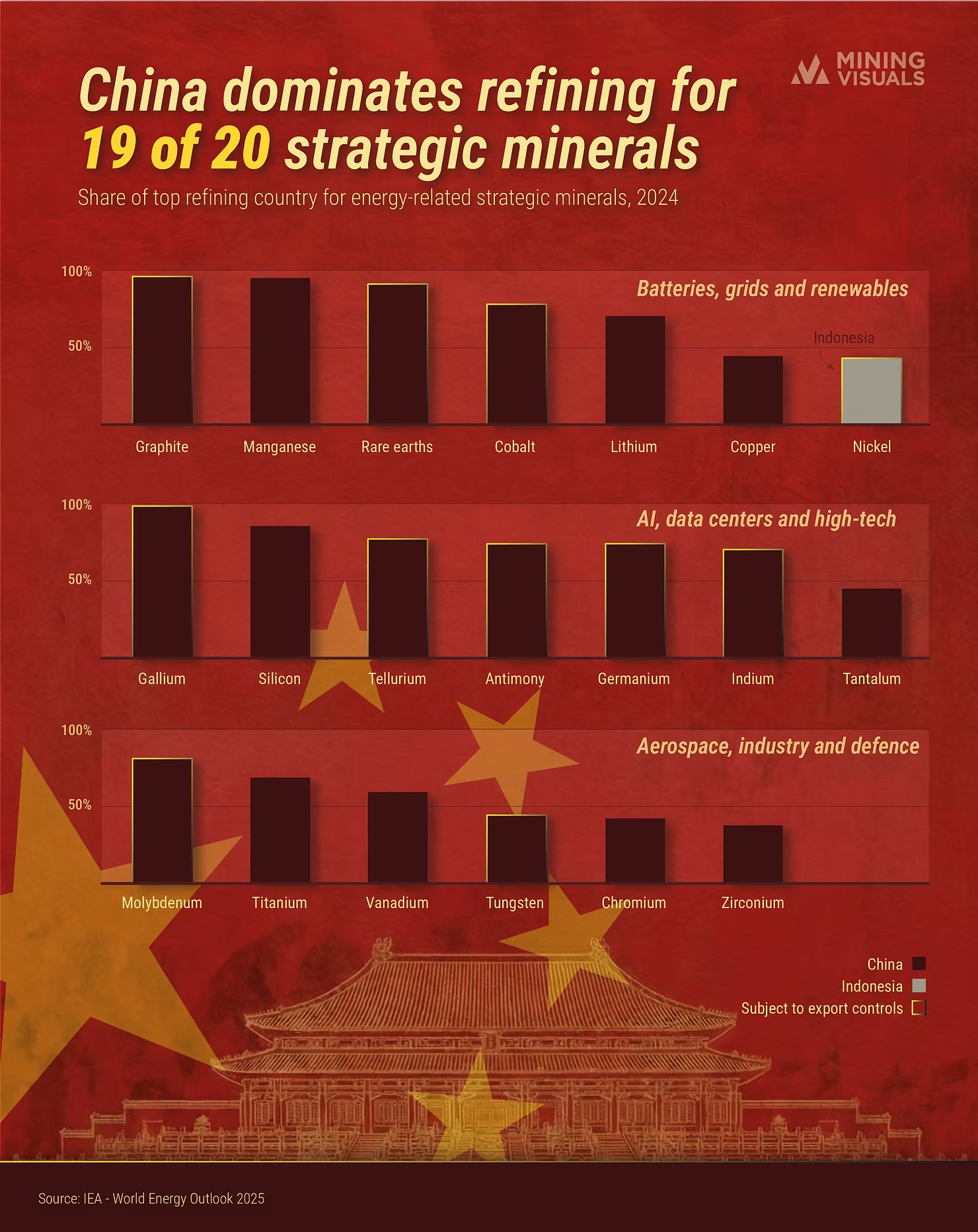

Data from 2024 indicates a high degree of concentration in this sector. According to the IEA's Global Critical Minerals Outlook 2025, China currently holds the leading refining share for 19 of the 20 strategic minerals essential to the global economy. This processing capacity places the country at the center of supply chains for technologies ranging from electric vehicle batteries to advanced semiconductors.

Concentration in Processing Capacity

While nations such as Australia, Chile, and the DRC are major producers of raw ores, the refining process, which is often energy-intensive and technically complex, is largely centralized.

This concentration is particularly notable in three key sectors:

Recent data suggests this trend is continuing. The IEA reports that the average market share of the top refining nations for key energy minerals increased from approximately 82% in 2020 to 86% in 2024.

The Nickel Market: Indonesia's Role

Nickel is the primary strategic mineral where China does not hold the top refining share.

Indonesia has emerged as the global leader in refined nickel production, a shift driven by a ban on raw ore exports that encouraged domestic processing. Following this policy, there was a substantial increase in foreign direct investment to build refining infrastructure. As of 2024, Indonesia controls approximately 60-70% of the world's refined nickel supply.

However, reports indicate that a majority of this refining capacity, up to 75%, is controlled by Chinese firms, integrating it into the broader Asian processing market.

Export Regulations and Market Impact

Recent policy changes have highlighted the sensitivity of these supply chains. Between 2023 and 2024, new export regulations were introduced for Gallium, Germanium, and Antimony.

These regulatory adjustments had a measurable impact on global markets. Following the implementation of these controls, prices for these metals saw significant increases in European and US markets, with Gallium rising by approximately 360% and Germanium by 400%. This volatility underscores the importance of stable supply chains for industries such as semiconductor manufacturing.

Future Outlook

The current distribution of refining capacity presents a complex challenge for global markets. Diversifying supply chains involves significant capital investment and long lead times, often 5 to 10 years for new refining projects. Additionally, existing market leaders have the ability to adjust output, which can influence global prices and impact the economic viability of new entrants.

For stakeholders, the data suggests that securing raw materials is only one part of the equation; access to processing and refining capacity is equally critical for long-term supply security.

Sources & Further Reading

- International Energy Agency (IEA) – Global Critical Minerals Outlook 2025

- Primary data on global refining shares and market concentration for strategic minerals.

- Mining Newswire – China Controls Graphite Supply Chain: A Concern for Energy Transition

- Analysis of graphite refining dominance and its specific impact on the battery sector.

- ING Think – Nickel: Still Capped by Surplus

- Detailed insights into Indonesia's nickel production volumes and market share.

- East Asia Forum – The Illusion of Control in Indonesia’s Nickel Revolution

- Context on Indonesia's export bans and the geopolitical strategy behind downstreaming.

- Swedish National China Centre – China’s Mineral Export Restrictions: Market Impacts

- Quantitative data on price spikes for Gallium and Germanium following the implementation of export controls.

Explore More

View All

Silver’s Elevation to Critical Mineral Status: A Strategic Turning Point for U.S. Supply Chains

Silver’s Elevation to Critical Mineral Status: A Strategic Turning Point for U.S. Supply Chains

The U.S. Department of the Interior’s addition of silver to the Final 2025 List of Critical Minerals in November 2025 marks a pivotal shift. No longer viewed primarily as a precious metal for jewelry and investment, silver is now recognized as vital to technology, the energy transition, and national security.

The EU’s Race for Critical Raw Materials: Navigating Supply Risks

The EU’s Race for Critical Raw Materials: Navigating Supply Risks

As the European Union moves toward its goal of net-zero emissions by 2050, the demand for critical raw materials, the building blocks of wind turbines, batteries, and solar panels—is skyrocketing.