Lithium

February 19, 2026

3 min

Lithium

Key takeaways

Key Takeaways

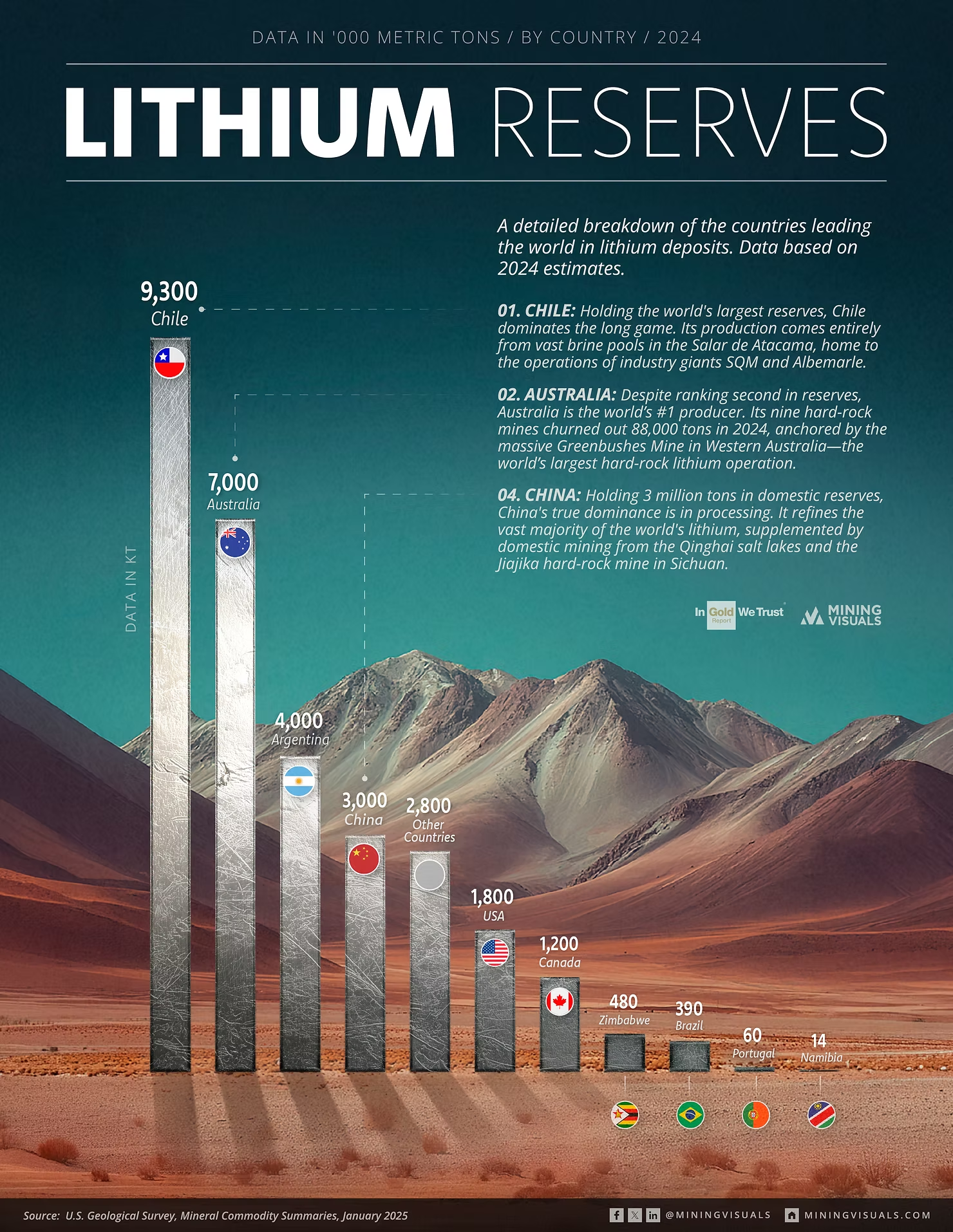

- Chile Holds the Most Lithium: With 9.3 million tons, Chile dominates global reserves through its vast brine pools, though new government policies are reshaping how foreign companies invest there.

- China Dominates Refining, Not Mining: China ranks 4th in reserves but controls 65–70% of global processing, meaning most lithium must still pass through China before becoming a battery.

- The U.S. is Ramping Up: The United States (1.2M tons) is finally moving from exploration to extraction, with major projects like Thacker Pass aiming to reduce reliance on foreign supply chains.

The "Lithium Winter" appears to be breaking.

On February 11, 2026, industry bellwether Albemarle Corporation (NYSE: ALB) signaled that the brutal price correction of 2023–2024 has finally stabilized. After a 90% price collapse forced a global recalibration of supply chains, the market is emerging leaner and more strategic.

While the "white gold rush" of the early 2020s was defined by speculation, 2026 is defined by security of supply. As automakers and data center energy storage providers lock in long-term contracts, the focus has shifted from "who has potential" to "who has the rock."

The infographic above visualizes the playing field using the latest data from the U.S. Geological Survey (January 2025), ranking the nations holding the keys to the energy transition.

.avif)

The "Lithium Triangle" Explained

The data reveals a stark geological divide centered on South America. Chile (9.3 million tons) and Argentina (4.0 million tons) form two-thirds of the so-called "Lithium Triangle"—a high-altitude region in the Andes that also includes Bolivia.

This area is famous for its "salars," or salt flats. Unlike traditional mines where rock is crushed, lithium here is pumped from underground reservoirs as a salty brine and left to evaporate in the sun. It is generally cheaper to produce but takes much longer to bring to market.

Chile’s dominance is anchored in the Salar de Atacama, home to industry giants like SQM and Albemarle. However, the landscape is shifting under President Boric’s National Lithium Strategy, which mandates public-private partnerships. While this secures state revenue, it has slowed new exploration. Meanwhile, Australia (7.0 million tons) has taken a different path, focusing on "hard rock" mining. These traditional mines can be built faster than brine ponds, allowing Australia to remain the world's top producer despite having smaller reserves than Chile.

China: The Midstream Monopoly

Looking strictly at the reserve chart, China (3.0 million tons) appears to be a tier-2 player, trailing Argentina. This is a dangerous misconception.

While China controls only about 18% of global raw lithium mining, its dominance lies in what happens after the metal leaves the ground. China processes an estimated 65% of the world’s lithium and manufactures over 75% of global lithium-ion batteries.

This "midstream monopoly" means that even lithium mined in Australia or Africa often travels to China for refining before ending up in a European or American electric vehicle. For Western investors, this disconnect between reserves and refining is the primary driver behind the aggressive push for domestic processing capacity in the US and Canada.

The North American Pivot

The United States appears on the chart with 1.2 million tons of reserves, primarily locked in Nevada’s clay and brine deposits. While this number is small compared to Chile, it represents a massive strategic pivot.

Following the Inflation Reduction Act (IRA) and the 2024–2025 surge in Department of Energy loans, projects in the Thacker Pass and the Salton Sea are attempting to build a "mine-to-battery" supply chain that bypasses the Chinese refining circuit. Canada (1.8 million tons) is following suit, leveraging its hard-rock resources in Quebec and Ontario to feed the growing "Battery Belt" of factories emerging in the American Midwest.

Conclusion

The 2024/2025 data snapshot captures a market in transition. We have moved past the era of easy discovery into the era of strategic extraction.

While Chile and Australia hold the physical advantage today, the geopolitical value of these reserves depends entirely on the ability to refine them. As we move deeper into 2026, the real value for investors won't just be in who holds the reserves, but who can get them out of the ground and into a battery cell without navigating a single choke point.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice.

Sources:

Explore More

View All

Mapped: Zinc's Use Across Five Industries and the 2030 Demand Outlook

Mapped: Zinc's Use Across Five Industries and the 2030 Demand Outlook

We've covered zinc's role in energy, health, and sustainability before, alongside the supply base concentrated in a handful of mega-mines and the production map that has shifted toward Asia since the mid-1990s. The story of 2025 is what changed on the demand side. In November, the U.S. Geological Survey retained zinc on its final 2025 List of Critical Minerals.

Lithium Use Cases: Batteries Now Consume 88% of Global Supply

Lithium Use Cases: Batteries Now Consume 88% of Global Supply

In February 2026, the U.S. Geological Survey put a fresh number on a transformation that has been building for a decade: batteries now account for 88% of global lithium end-use, up from 87% a year earlier. The metal that once quietly toughened ceramics and thickened industrial greases has been almost entirely repurposed by the battery economy. As covered in our reporting on the shift from surplus to deficit, the supply side of this story is tightening.

Sort First, Grind Later: The sensor technology reshaping polymetallic processing

Sort First, Grind Later: The sensor technology reshaping polymetallic processing

Sensor-based sorting lets miners reject barren rock before it's ever crushed, saving energy, water, and tailings volume at industrial scale. Polymetallic deposits, the orebodies that carry multiple economically valuable metals in a single rock, present a distinctive processing challenge: the valuable minerals are locked together with each other and with vast volumes of barren rock, demanding both heavy grinding and complex multi-stage separation.

CATL's 6-Minute Charge Closes the Gap with Gas — Without Cobalt or Nickel

CATL's 6-Minute Charge Closes the Gap with Gas — Without Cobalt or Nickel

On April 21, 2026, at its "Beyond the Pole" Tech Day in Beijing, CATL unveiled the third generation of its Shenxing battery, claiming a 10%-to-98% charge in 6 minutes 27 seconds. The launch came six weeks after BYD unveiled its second-generation Blade Battery with a 10%-to-97% charge in around 9 minutes.