Lithium

March 23, 2026

2 min

Lithium

Key takeaways

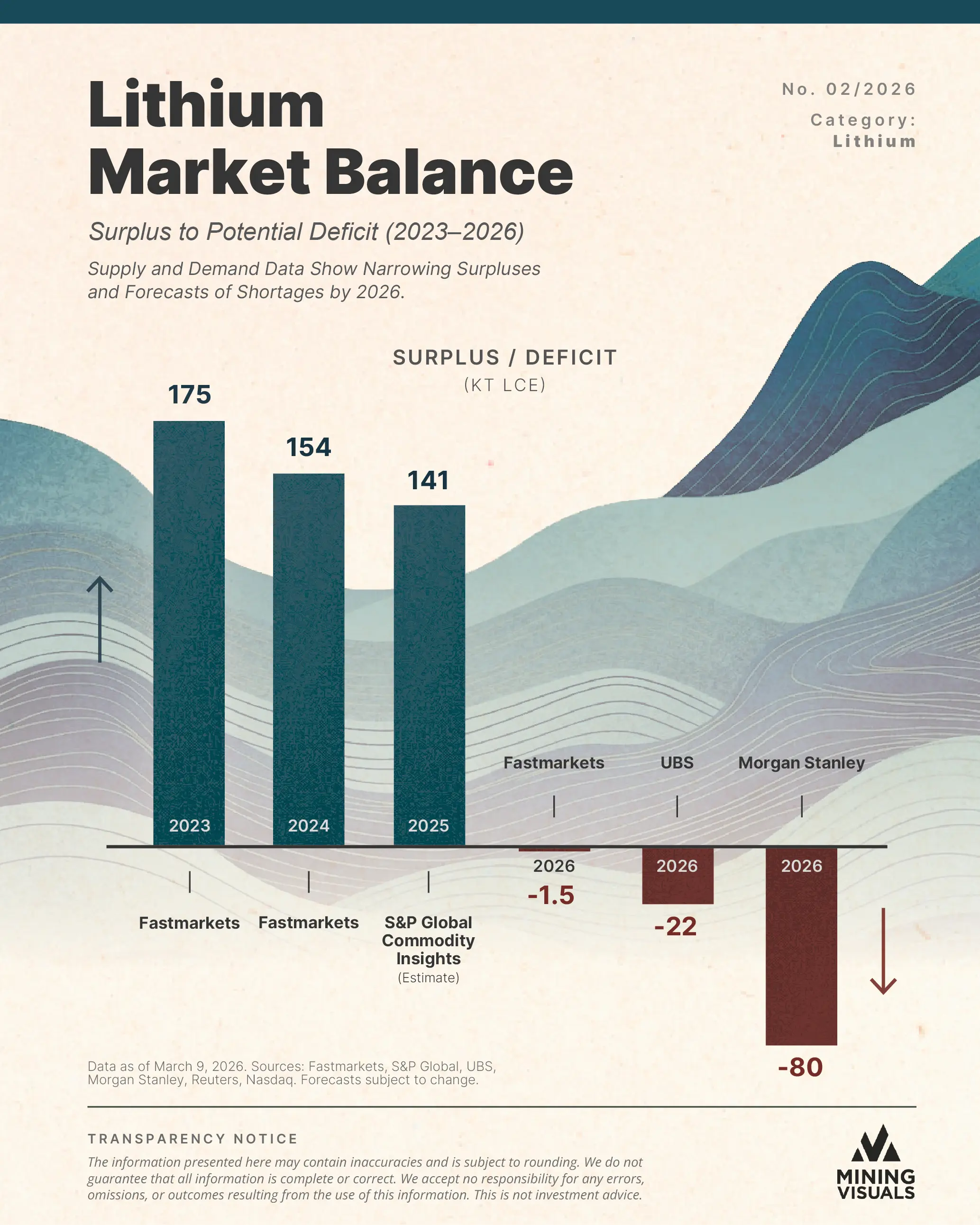

- Track the contraction: Monitor the rapidly shrinking lithium surplus, which has fallen from a peak of 175,000 tonnes in 2023 to an estimated 141,000 tonnes in 2025.

- Prepare for the 2026 shortfall: Acknowledge the consensus among major financial institutions that lithium will enter a structural deficit by 2026, with estimates projecting a shortage of up to 80,000 tonnes.

- Capitalize on the price floor: Note the ongoing market reaction, as Chinese spot prices have already rebounded 57% from their June 2025 lows in anticipation of tighter supply.

The global lithium market is undergoing a severe structural reversal. After a multi-year glut that crushed spot prices, the critical battery metal is careening toward a steep supply deficit by 2026. This shift isn't just a cyclical anomaly; it is a policy-driven correction. As Reuters recently reported in early 2026, an unprecedented energy storage boom is rapidly strengthening the demand outlook for the beaten-down metal. Major producers have slashed output, while global electric vehicle (EV) expansion and grid storage requirements continue to accelerate. For investors and industry professionals who previously navigated the structural transition of the silver market, the current lithium landscape presents a familiar, yet distinctly urgent, narrative. The era of the lithium glut is officially ending.

The Era of Oversupply

Between 2022 and 2024, the lithium market was defined by a massive wave of excess supply. A surge of new production, driven predominantly by operations in Australia and China, flooded the market exactly as short-term demand growth temporarily cooled.

The resulting imbalance was severe. According to Fastmarkets, the market surplus peaked at approximately 175,000 tonnes of Lithium Carbonate Equivalent (LCE) in 2023. By 2024, the surplus remained elevated at 154,000 tonnes. Predictably, this excess inventory crushed spot prices. After hitting record highs of roughly 150,000 yuan per tonne in late 2022, lithium carbonate prices in China plummeted by more than 80%, bottoming out at just $8,259 per tonne by June 2025.

The Catalysts for Reversal

This dramatic price collapse triggered a fierce and natural market correction. Mining economics dictated the response: as prices fell below the cost of production, major Chinese operations curtailed capacity, Australian spodumene miners reduced output, and global exploration budgets were heavily slashed.

While supply was aggressively reigned in, the underlying demand drivers only accelerated:

- Electric Vehicles (EVs): Maintaining their position as the primary demand driver (roughly 70% of total consumption), global EV sales are projected to surpass 25 million units by 2026.

- Energy Storage Systems: Utilities are massively expanding battery capacity to stabilize solar and wind grids. Grid storage is currently the fastest-growing segment, now accounting for 15% of total lithium demand.

- Heavy-Duty Transport: Electric trucks and buses, requiring significantly larger battery packs, are adding a steady 10% incremental demand to the market.

The 2026 Deficit Projections

The surplus contraction is already underway. S&P Global Commodity Insights forecasts the surplus will narrow to 141,000 tonnes LCE in 2025, driven by a 13.5% year-over-year increase in consumption.

However, the definitive pivot arrives in 2026. While major financial institutions vary on the exact magnitude, the consensus firmly points to a supply deficit:

The variance in these forecasts hinges on supply elasticity. Conservative estimates assume sidelined production will quickly restart as prices rise. Conversely, Morgan Stanley's aggressive 80,000-tonne deficit projection accounts for the reality that complex mine restarts often require two to five years to fully integrate back into the global supply chain.

Final Synthesis: Pricing in the Pivot

Markets are forward-looking mechanisms, and the shift from glut to deficit is already being priced in. Between June and November 2025, Chinese lithium carbonate spot prices recovered from $8,259 to $13,003 per tonne—a swift 57% rebound in just five months.

Much like the silver market's historical transitions, the fundamental drivers of the lithium deficit—global electrification, decarbonization mandates, and grid storage integration—are structural, not cyclical. The data indicates that the question is no longer if the lithium market will face a supply shortage, but rather how aggressively the supply chain will struggle to meet the compounding demand of the late 2020s.

Sources & References

- S&P Global Commodity Insights — "COMMODITIES 2026: Lithium carbonate surplus to narrow; energy storage to drive growth" (January 9, 2026).

- Reuters — "Energy storage boom strengthens demand outlook for beaten-down lithium" (January 4, 2026).

- Fastmarkets / CarbonCredits — "Lithium Prices Surge Amid Strong Demand Forecasts, Could Reach Up to $28,000/Ton by 2026" (January 2026).

- Nasdaq — "Lithium Market 2025 Year-End Review" (December 2025).

- Bloomberg — Lithium carbonate spot price data (China), June–November 2025.

Disclaimer: The information presented in this article is for informational purposes only and is based on publicly available reports and market data. Production and demand forecasts are estimates from the cited sources and may differ from actual outcomes. This is not investment advice. Content is intended for educational purposes under the MiningVisuals mandate. Would you like me to draft a companion social media thread (e.g., for X or LinkedIn) to help promote this article?

Explore More

View All

Apple Outweighs Every Listed Miner on Earth, and It Is Not Even the Biggest Company

Apple Outweighs Every Listed Miner on Earth, and It Is Not Even the Biggest Company

One consumer-electronics company is now worth more than every publicly traded mining company on Earth combined. The graphic above captures the June 5 snapshot, when the 317 publicly traded miners tracked by CompaniesMarketCap were worth about $3.48 trillion

Three Weeks Public, SpaceX Already Approaches the Value of Every Listed Miner on Earth

Three Weeks Public, SpaceX Already Approaches the Value of Every Listed Miner on Earth

For 24 years SpaceX stayed private. Then, on June 12, 2026, it began trading on the Nasdaq in the largest IPO in history, priced at a $1.77 trillion valuation. Barely three weeks later the rocket and satellite maker is worth even more. As of early July, SpaceX carried a market capitalization of about $2.1 trillion, the seventh-highest of any public company on Earth, and it joins the Nasdaq-100 on July 7

Mapped: Zinc's Use Across Five Industries and the 2030 Demand Outlook

Mapped: Zinc's Use Across Five Industries and the 2030 Demand Outlook

We've covered zinc's role in energy, health, and sustainability before, alongside the supply base concentrated in a handful of mega-mines and the production map that has shifted toward Asia since the mid-1990s. The story of 2025 is what changed on the demand side. In November, the U.S. Geological Survey retained zinc on its final 2025 List of Critical Minerals.

Lithium Use Cases: Batteries Now Consume 88% of Global Supply

Lithium Use Cases: Batteries Now Consume 88% of Global Supply

In February 2026, the U.S. Geological Survey put a fresh number on a transformation that has been building for a decade: batteries now account for 88% of global lithium end-use, up from 87% a year earlier. The metal that once quietly toughened ceramics and thickened industrial greases has been almost entirely repurposed by the battery economy. As covered in our reporting on the shift from surplus to deficit, the supply side of this story is tightening.