Copper

May 5, 2026

2 min

Copper

Key takeaways

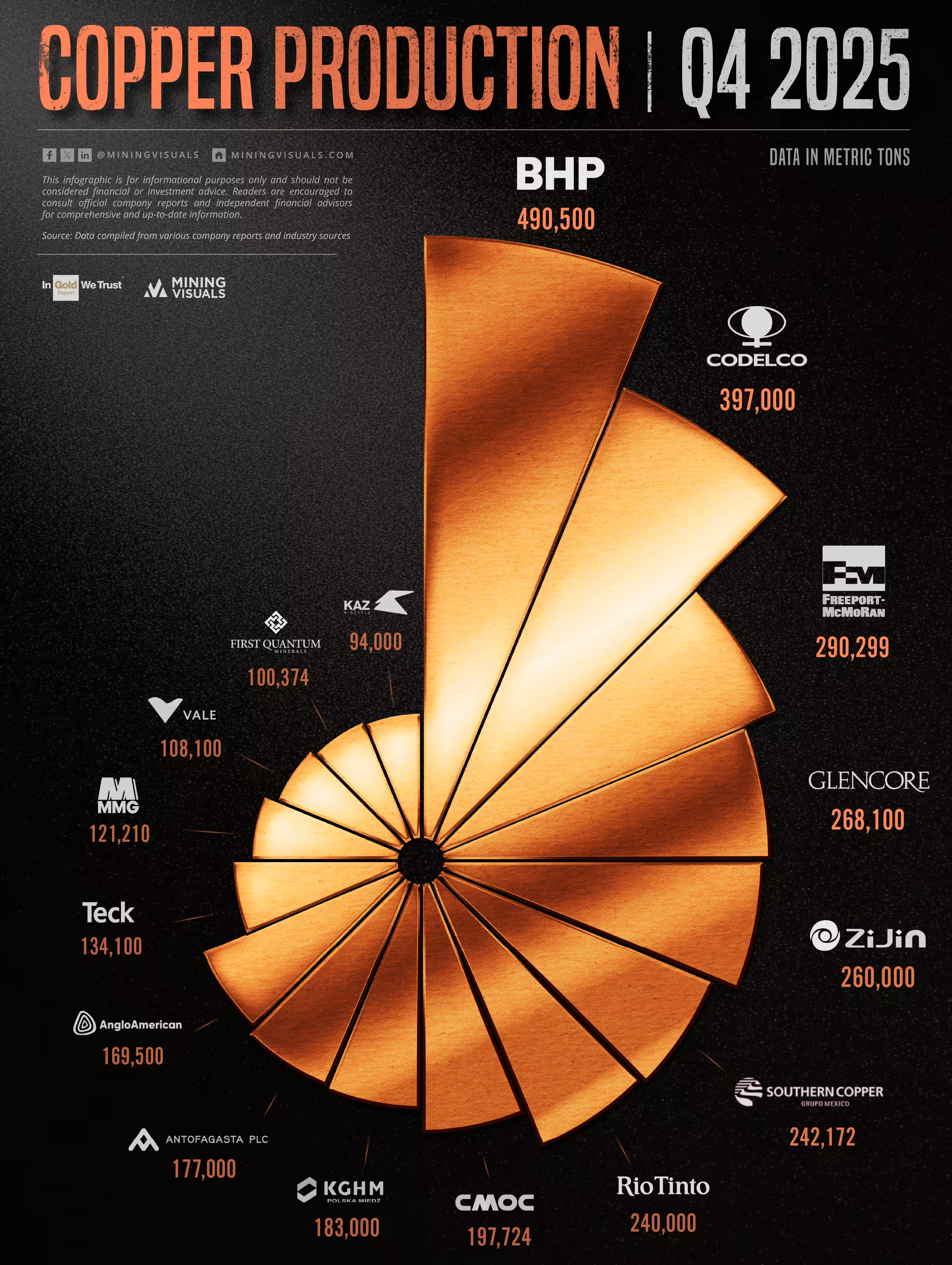

- BHP Maintains the Crown: BHP Group led global production by a wide margin, delivering 490.5 kilotonnes (kt) in Q4 2025, outpacing second-place Codelco by nearly 100 kt.

- Expansions Drive Mid-Tier Growth: Companies like MMG and Vale reported substantial output surges, driven by historic operational breakthroughs at Las Bambas and all-time-high production at the Salobo complex, respectively.

- Grade Declines Cap Output: Several majors, including Anglo American (-14% YoY) and KAZ Minerals, reported production dips as they processed lower-grade ores, highlighting the ongoing geological challenges in mature copper districts.

As power-hungry AI data centers drive a projected 2-million-ton surge in global copper demand by 2030, market attention remains fixated on the supply side. Fourth-quarter 2025 metrics provide a definitive look at how the world's top miners closed out the year. While overall volumes remain heavily concentrated among a few historic industry giants, the true Q4 narratives emerged further down the list, as mid-tier producers leveraged flagship asset expansions to hit multi-year highs and offset the sector's ongoing struggle with declining ore grades.

The Heavyweights: BHP, Codelco, and Freeport-McMoRan

The top of the production hierarchy remains securely defended by three industry giants. BHP firmly held the number one position, reporting total copper production of 490.5 kt for the quarter.

Chile’s state-owned Codelco followed in second place. By reconciling their finalized 2025 full-year volume (1,334 kt) against their nine-month cumulative reporting, Codelco’s Q4 output stood at a robust 397 kt, rounding out a year that saw a slight 6-kilotonne increase over 2024. Freeport-McMoRan secured the third spot, reporting consolidated quarterly production of 640 million recoverable pounds (approximately 290 kt).

Directly behind the top three, Glencore (268.1 kt) and Zijin Mining (260 kt) maintained highly consistent output, with Zijin perfectly matching its Q3 production pace to cross the 1.09 million tonne mark for the full year.

Mid-Tier Movers: Ramp-Ups and Record Highs

The middle of the pack showcased some of the strongest growth narratives of the quarter. Rio Tinto produced 240 kt in Q4, representing a significant 17.6% quarter-over-quarter increase. This late-year surge was largely attributed to the Kennecott mine returning from scheduled maintenance and improved feed grades from the underground ramp-up at Oyu Tolgoi.

Teck Resources delivered 134.1 kt (up 10% YoY), fueled heavily by the ongoing ramp-up at its Quebrada Blanca (QB) mine in Chile, which achieved its strongest quarterly performance of the year. Similarly, Vale hit a multi-year high, producing 108.1 kt of copper. This marked the Brazilian miner's highest quarterly output since 2018, pushed upward by all-time-high production at the Salobo complex.

Perhaps the most notable growth came from MMG Limited. The company reported 121.2 kt for the quarter, capping off a year where total annual copper production surged 27% to 506.9 kt. This milestone was underpinned by a historic operational breakthrough at the Las Bambas mine in Peru. CMOC also concluded a record year (741,100 tonnes total), deriving a Q4 production volume nearing 200,000 tonnes (197,724 tonnes).

Navigating Headwinds: Geological and Operational Hurdles

Not all producers saw upward trajectories in the final months of 2025. Anglo American reported 169.5 kt of copper for Q4, a 14% year-over-year decrease largely tied to lower ore grades at the Quellaveco and Collahuasi mines.

Lower grades also impacted First Quantum Minerals, which produced 100.4 kt (a 4% quarter-over-quarter drop) due to lower throughput at the Sentinel mine, though this was partially offset by the successful commercial declaration of the Kansanshi S3 expansion.

Final Synthesis: The Supply Balancing Act

The Q4 2025 production data illustrates a polarized mining environment. While aggregate output from the top 16 producers remains robust, the growth is heavily reliant on a handful of successful expansions (like Teck's QB and MMG's Las Bambas) offsetting the natural grade declines experienced by established operations (such as those managed by Anglo American and KAZ Minerals). As miners transition into 2026, the data indicates that sustaining output will increasingly depend on unlocking underground expansions and optimizing recovery rates across maturing assets.

MiningVisuals Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Always conduct your own research. Sources: Visual Capitalist - Top Copper Producers 2000-2024, BHP Group, Codelco, Freeport-McMoRan, Glencore, Zijin Mining, Southern Copper, Rio Tinto, CMOC, Anglo American, KGHM Group, Antofagasta PLC, MMG Limited, Vale, First Quantum Minerals, Teck Resources, KAZ Minerals, Lundin Mining, Ivanhoe Mines.

Explore More

View All

Ranked: The World's Largest Copper Mines (2025)

Ranked: The World's Largest Copper Mines (2025)

Copper has spent 2026 setting records, touching an intraday COMEX high of $6.71 per pound on May 13 amid AI-driven demand and supply shocks, against a backdrop where the ICSG now forecasts a 150,000-tonne deficit for 2026. In a market this tight, where the deficit thesis turns on lost tonnes, the question of where the world's copper actually comes from carries unusual weight.

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper has spent most of 2026 doing something it had not done in a quarter century: setting fresh records every few weeks. The COMEX contract printed an intraday all-time high of $6.71 per pound on May 13, and the May monthly close looks set to land at the top of the historical chart. In London, copper traded above $14,000 per tonne in mid-May, touching $14,196.50, within reach of the LME's January 29 record of $14,527.50.

The Cost of Mining Copper: A 2024–2025 Update

The Cost of Mining Copper: A 2024–2025 Update

Copper futures touched an all-time high above $6.58 per pound on May 12, 2026, capping a 40.86% gain over the prior twelve months as supply tightness collided with structural demand from grid build-out, electric vehicles, and AI data centers. Earlier in the year, the LME benchmark rallied 22% to a record $13,387 per tonne on January 6, 2026. Behind the price action lies a less-discussed story: what it actually costs the world's largest miners to pull a pound of copper out of the ground.

Copper Market Balance: A Look at 2026 Deficit Forecasts

Copper Market Balance: A Look at 2026 Deficit Forecasts

For years, analysts modeling the global copper market were comforted by a reliable buffer of surplus supply. But as our latest data visualization reveals, that cushion has violently evaporated. The International Copper Study Group (ICSG) has officially abandoned its projected surplus for 2025 to officially forecast a 150,000-metric-ton deficit for 2026—the market's first structural shortage since 2009. Wall Street is bracing for an even harsher reality.