Copper

Ranked: The World's Largest Copper Mines (2025)

Ten mines, six countries: 4.9M tonnes and a fifth of global copper supply

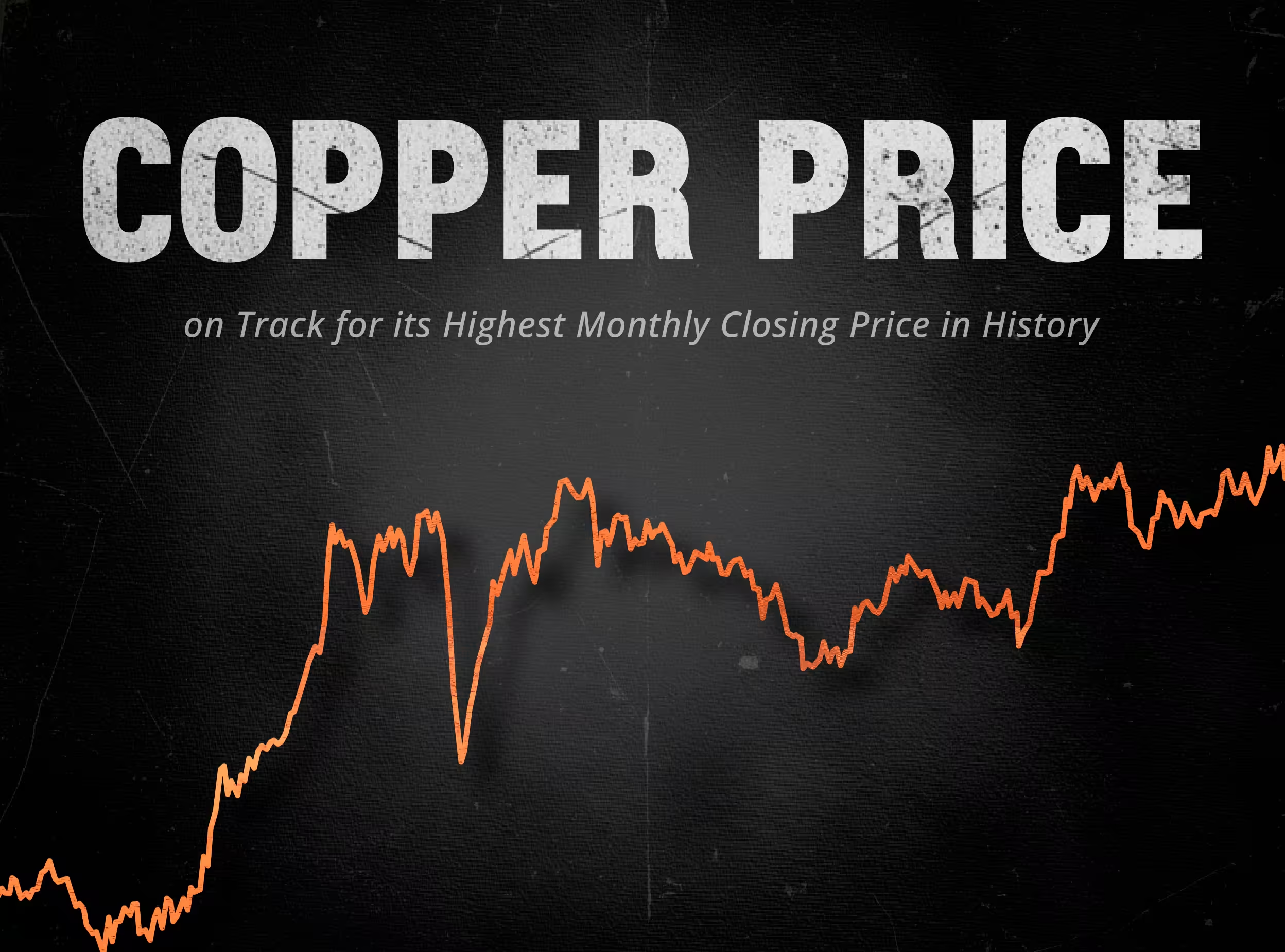

Copper has spent 2026 setting records, touching an intraday COMEX high of $6.71 per pound on May 13 amid AI-driven demand, against a backdrop where the ICSG now forecasts a 150,000-tonne deficit for 2026. In a market this tight, where the deficit thesis turns on whether supply can keep pace, the question of where the world's copper actually comes from carries unusual weight. MINING.COM's latest ranking provides the answer: the ten biggest mines on the planet produced 4.9 million tonnes in 2025, more than a fifth of total global mined production. The infographic above shows the figures; the sections below explain what the ranking reveals about how concentrated, and how structured, global copper supply has become.

The single most striking feature of the ranking is not the order but the gap at the top. Escondida in Chile produced 1,347.6 kt in 2025, while the source places second-ranked Tenke Fungurume at roughly 519 kt. That is a lead of more than two and a half times over the next-largest mine, and Escondida accounts for over a quarter of the top 10's combined output, a larger share than any other single asset on the list.

The ranking's most counterintuitive detail is an absence. Per the same source, after recently being surpassed by BHP as the world's number one copper producer on an attributable basis, Chile's state-owned Codelco does not have any operation that qualifies for the top 10. That can look like a contradiction until the two measures are separated. A mine ranking counts the total output of a single physical site regardless of who owns it. A company ranking counts a producer's attributable share across its whole portfolio. Codelco's production is spread across multiple operations rather than concentrated in one record-setting pit, so it ranks highly as a company while placing no single mine in this list.

This publication has tracked the company-basis view separately, where BHP led Q4 2025 production at 490.5 kt. The same logic applies at the top: the 1,347.6 kt credited to Escondida is the whole mine's output, whereas BHP's own attributable share was about 1.13 million MT in 2025, the rest belonging to its joint-venture partners.

The geography behind the list is narrow. By the source's own figures, Chile contributes the largest single mine (Escondida) and Collahuasi; Peru appears three times, through Las Bambas, Cerro Verde and Antamina; and the Democratic Republic of Congo accounts for two entries, Tenke Fungurume and Kamoa-Kakula. Indonesia (Grasberg), Mexico (Buenavista) and Poland (KGHM) round out the rest. In other words, the top 10 mines are spread across just six countries, with the Andes and Central Africa supplying the bulk. That concentration is the structural backdrop to the supply concerns documented in our coverage of the 2026 deficit: a short list of mines in a short list of jurisdictions carries an outsized share of world output.

Most of these mines are joint ventures, not single-owner assets. Escondida lists four owners (BHP, Rio Tinto, Mitsubishi and JX Advanced Metals); Antamina is shared among BHP, Glencore, Teck and Mitsubishi; Collahuasi, Grasberg, Las Bambas, Cerro Verde and Kamoa-Kakula are likewise held by multi-party groups, frequently pairing Western majors, Chinese producers and state entities.

The KGHM entry, 100% owned by Poland's Polska Miedz, is the one fully single-owner line on the list, but it is worth clarifying what that entry represents. Unlike Escondida or Grasberg, which are individual mines, KGHM's Polish copper output is drawn from three underground mines, Lubin, Rudna and Polkowice-Sieroszowice, feeding the company's concentrator and smelter network. The ranking treats KGHM's wholly-owned Polish operation as a single line, which is a useful reminder that "mine" in these tables can mean either a single deposit or a company's integrated mining complex. For investors, the broader pattern still holds: exposure to the world's biggest copper sources almost always means exposure shared across several listed companies and governments, or, in KGHM's case, to a single company operating a cluster of mines rather than one pit.

Taken together, the ranking tells a story the production figures alone do not. Global copper supply at the top is concentrated in a handful of mines producing 4.9 million tonnes, more than a fifth of world output, dominated by a single outsized asset in Escondida, drawn from just six countries, and owned largely through multi-party joint ventures rather than by any one company. Set against record prices and a forecast 2026 deficit, the ranking shows just how few assets, in how few places, the supply side is built on.

MiningVisuals Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Always conduct your own research.

Sources: MINING.COM, World's 10 biggest copper mines 2026; KGHM Polska Miedz; Investing News Network; MiningVisuals: Copper on Track for Its Highest Monthly Close; MiningVisuals: Copper Market Balance; MiningVisuals: The World's Top 16 Copper Producers Q4 2025.

Copper has spent most of 2026 doing something it had not done in a quarter century: setting fresh records every few weeks. The COMEX contract printed an intraday all-time high of $6.71 per pound on May 13, and the May monthly close looks set to land at the top of the historical chart. In London, copper traded above $14,000 per tonne in mid-May, touching $14,196.50, within reach of the LME's January 29 record of $14,527.50.

Copper futures touched an all-time high above $6.58 per pound on May 12, 2026, capping a 40.86% gain over the prior twelve months as supply tightness collided with structural demand from grid build-out, electric vehicles, and AI data centers. Earlier in the year, the LME benchmark rallied 22% to a record $13,387 per tonne on January 6, 2026. Behind the price action lies a less-discussed story: what it actually costs the world's largest miners to pull a pound of copper out of the ground.

As power-hungry AI data centers drive a projected 2-million-ton surge in global copper demand by 2030, market attention remains fixated on the supply side. Fourth-quarter 2025 metrics provide a definitive look at how the world's top miners closed out the year. While overall volumes remain heavily concentrated among a few historic industry giants, the true Q4 narratives emerged further down the list, as mid-tier producers leveraged flagship asset expansions to hit multi-year highs and offset the sector's ongoing struggle with declining ore grades.

For years, analysts modeling the global copper market were comforted by a reliable buffer of surplus supply. But as our latest data visualization reveals, that cushion has violently evaporated. The International Copper Study Group (ICSG) has officially abandoned its projected surplus for 2025 to officially forecast a 150,000-metric-ton deficit for 2026—the market's first structural shortage since 2009. Wall Street is bracing for an even harsher reality.