Precious Metals

March 5, 2026

3 min

Precious Metals

Key takeaways

Key Takeaways

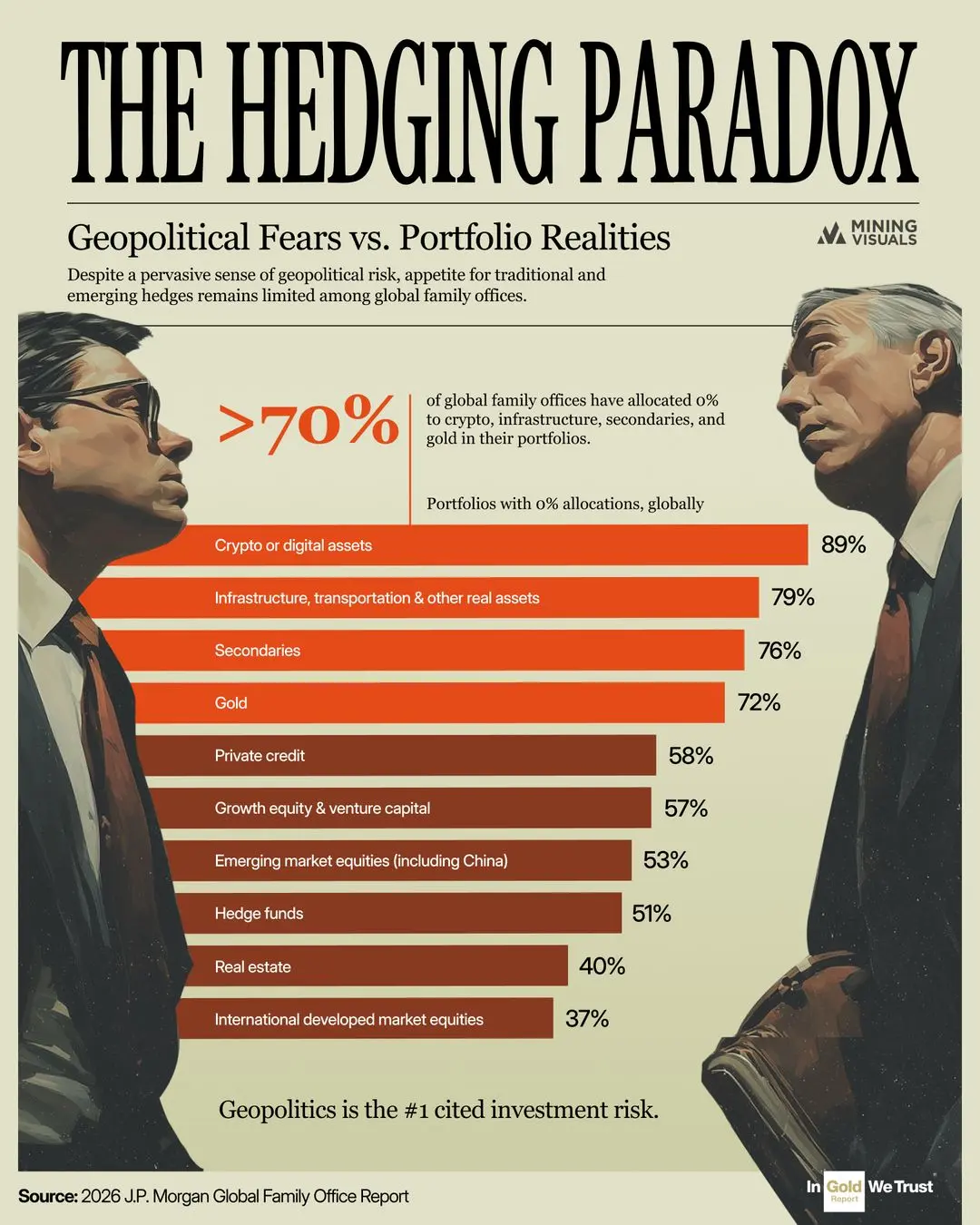

- Geopolitics is the Top Risk, but Hedges are Ignored: One in five global family offices identify geopolitics as their number one investment risk. However, despite these fears, 72% of these offices have zero exposure to traditional safe havens like gold.

- AI Ambitions Lack an Infrastructure Foundation: While 65% of family offices plan to prioritize artificial intelligence investments, 79% have zero allocation to the physical infrastructure required to power it.

- Crypto Remains Sidelined Despite Hype: Despite the headlines surrounding digital assets, a massive 89% of family offices remain on the sidelines and have no exposure to cryptocurrencies in their portfolios.

The geopolitical temperature is boiling. Between shifting global alliances, fractured supply chains, and persistent structural inflation, macro uncertainty is the defining feature of 2026. According to the newly released J.P. Morgan Private Bank 2026 Global Family Office Report—which gathered insights from 333 family offices—geopolitics is overwhelmingly cited as the number one risk to portfolio performance.

Yet, a glaring contradiction has emerged. While we have already established the profound structural deficits and safe-haven demand driving the recent silver breakout, the world's wealthiest families are surprisingly under-allocated in traditional and alternative hedges. Instead of flocking to hard assets, a staggering majority are sitting on the sidelines, completely ignoring gold, infrastructure, and digital assets. This disconnect between stated fears and actual capital deployment is what we call "The Hedging Paradox."

The #1 Risk Nobody is Hedging

According to the 2026 J.P. Morgan Global Family Office Report, which surveyed 333 single family offices overseeing an average of $1.16 billion in assets, geopolitics and trade policy dominate the macro risk landscape. For international offices, the anxiety is even more pronounced, with 74% ranking geopolitics among their top five concerns.

However, when looking under the hood of these billion-dollar portfolios, defensive posturing is remarkably absent. Traditional safe havens like gold are entirely absent from 72% of family office portfolios. Even among those who do invest, the average global allocation to gold is a microscopic 0.9%.

The AI Disconnect: Software over Hardware

The promise of artificial intelligence is a dominant investment theme, with 65% of family offices globally prioritizing AI. Yet, the capital is flowing almost exclusively into the application and software layers, ignoring the massive physical footprint required to sustain the technology.

An astonishing 79% of family offices have zero allocation to infrastructure, transportation, and other real assets. This represents a critical blind spot. Infrastructure is the physical backbone of the AI revolution, providing the immense power generation, connectivity, and logistics required for data centers. By completely avoiding real assets, these portfolios are exposed to the upside of AI software, but remain highly vulnerable to the inflation and physical supply constraints of the hardware reality.

Institutional Convergence and the Crypto Snub

Family offices are increasingly managing their capital like major institutional investors, heavily favoring growth-oriented risk assets. On average, public equities (38.4%) and private investments (30.8%) account for over two-thirds of portfolio allocations.

When these ultra-wealthy investors do seek alternatives, they lean heavily toward drawdown private equity funds and real estate. Meanwhile, emerging hedges are left in the dust. A massive 89% of family offices have no exposure to crypto or digital assets. This signals that despite mainstream hype, the smartest money in the room is still not convinced that cryptocurrencies belong in a generational wealth-preservation strategy.

The data reveals a fascinating behavioral gap in the ultra-wealthy demographic. Family offices correctly identify the shifting, fragmented global order and volatile inflation as their primary threats. Yet, their portfolios reflect an era of seamless globalization that has arguably already ended. As the geopolitical landscape continues to fracture, this "Hedging Paradox" suggests that when family offices finally decide to align their portfolios with their stated fears, the ensuing capital rotation into gold, infrastructure, and real assets could be significant.

Disclaimer & Sources

Disclaimer: The content provided on MiningVisuals is for educational and informational purposes only and does not constitute financial or investment advice. Always conduct your own due diligence and consult with a licensed financial advisor before making any investment decisions. Past performance is not indicative of future results.

Sources: J.P. Morgan Private Bank 2026 Global Family Office Report, Visual Capitalist.

Explore More

View All

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

In early 2026, the artificial intelligence narrative shifted abruptly from software capabilities to physical hardware constraints. With tech giants committing hundreds of billions to new infrastructure—pushing global hyperscaler capital expenditures past $600 billion this year—the industry has collided with a new primary bottleneck: a severe power and thermal crunch.

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Somewhere inside a pressurized-water reactor, an alloy that is four-fifths silver is absorbing neutrons to keep the core in check, a job most silver investors have never heard of. It is a useful reminder that the metal people picture as coins and jewelry mostly works elsewhere, across industry.

Ranked: The Countries That Produced the Most Silver in 2025

Ranked: The Countries That Produced the Most Silver in 2025

Mexico remained the world's top silver-producing country in 2025, mining 172.9 million ounces (Moz), roughly a fifth of global supply, according to the World Silver Survey 2026, produced for the Silver Institute by Metals Focus. But Mexico's lead narrowed: its output fell 5% for a third straight year, while second-place Peru climbed 7%. Global mine production rose 3% to 846.6 Moz, even as the ranking's top tier told a story of one leader sliding and its closest rival closing in.

Electric Vehicles Are Set to Become the Auto Industry's Biggest Silver Consumer by 2027

Electric Vehicles Are Set to Become the Auto Industry's Biggest Silver Consumer by 2027

Most of silver's 2026 story has been told from the supply side: a sixth straight year of structural deficit and a record price near $121 in January. Less examined is where the next leg of industrial demand actually comes from. With solar, silver's largest industrial use, now facing thrifting and substitution, the Silver Institute points to a quieter end-use picking up the slack: the automotive sector. A December 2025 study from Oxford Economics and the Silver Institute quantifies that shift, and the engine behind it is the electric vehicle.