Commodities

April 4, 2025

1 min

Commodities

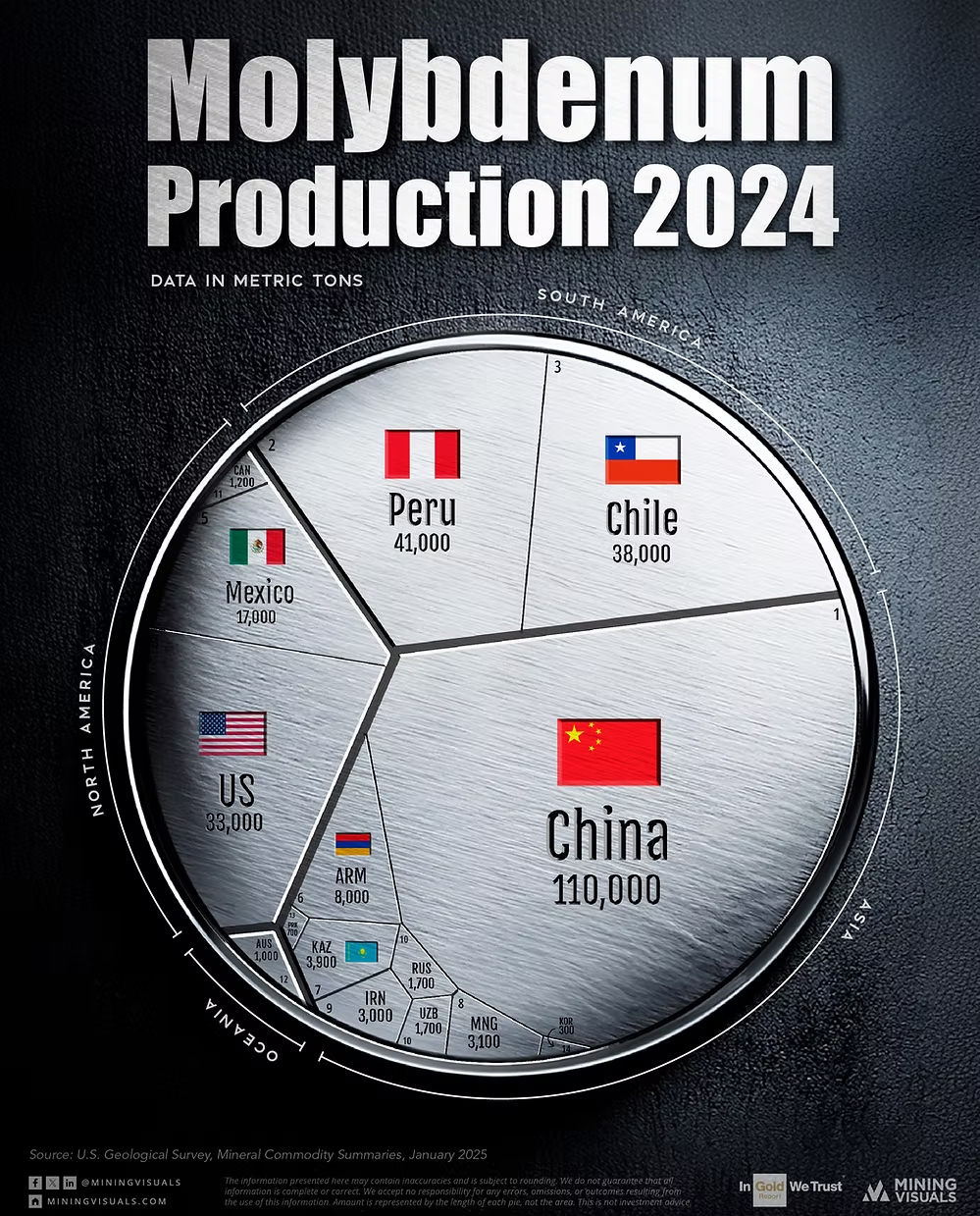

Molybdenum may not be a household name, but this versatile metal plays a crucial role in the modern economy. Its ability to enhance steel's strength, toughness, and resistance to heat and corrosion makes it indispensable in demanding applications, from high-strength alloys used in construction, aerospace, and automotive parts to catalysts essential for petroleum refining.

Recent data provides a snapshot of global molybdenum mine production estimates for 2024. The landscape continues to be dominated by China, estimated to produce around 110,000 metric tons (MT). Following China, a second tier of major producers includes Peru (approx. 41,000 MT), Chile (approx. 38,000 MT), the United States (approx. 33,000 MT), and Mexico (approx. 17,000 MT). Together, these five nations account for a significant majority of the world's primary molybdenum supply.

Other notable contributors illustrated include Armenia, Canada, Kazakhstan, Mongolia, Iran, Russia, and Uzbekistan, each playing a part in the global market. According to the USGS, overall global molybdenum production saw an estimated increase of 6% in 2024 compared to the previous year.

This concentration of production highlights the geological distribution of molybdenum resources. As industries continue to demand high-performance materials, particularly specialized steel alloys for infrastructure, energy, and transportation, molybdenum remains a strategically important metal underpinning key sectors of the global economy.

Source: U.S. Geological Survey, Mineral Commodity Summaries, January 2025

Disclaimer: Production figures for 2024 are estimates based primarily on U.S. Geological Survey (USGS) data and are for informational purposes only. Accuracy and completeness are not guaranteed; figures are subject to revision. Information on molybdenum's uses is provided for general context. This content does not constitute financial or investment advice. Conduct your own research before making decisions.

Explore More

View All

Mapped: Zinc's Use Across Five Industries and the 2030 Demand Outlook

Mapped: Zinc's Use Across Five Industries and the 2030 Demand Outlook

We've covered zinc's role in energy, health, and sustainability before, alongside the supply base concentrated in a handful of mega-mines and the production map that has shifted toward Asia since the mid-1990s. The story of 2025 is what changed on the demand side. In November, the U.S. Geological Survey retained zinc on its final 2025 List of Critical Minerals.

Lithium Use Cases: Batteries Now Consume 88% of Global Supply

Lithium Use Cases: Batteries Now Consume 88% of Global Supply

In February 2026, the U.S. Geological Survey put a fresh number on a transformation that has been building for a decade: batteries now account for 88% of global lithium end-use, up from 87% a year earlier. The metal that once quietly toughened ceramics and thickened industrial greases has been almost entirely repurposed by the battery economy. As covered in our reporting on the shift from surplus to deficit, the supply side of this story is tightening.

Sort First, Grind Later: The sensor technology reshaping polymetallic processing

Sort First, Grind Later: The sensor technology reshaping polymetallic processing

Sensor-based sorting lets miners reject barren rock before it's ever crushed, saving energy, water, and tailings volume at industrial scale. Polymetallic deposits, the orebodies that carry multiple economically valuable metals in a single rock, present a distinctive processing challenge: the valuable minerals are locked together with each other and with vast volumes of barren rock, demanding both heavy grinding and complex multi-stage separation.

CATL's 6-Minute Charge Closes the Gap with Gas — Without Cobalt or Nickel

CATL's 6-Minute Charge Closes the Gap with Gas — Without Cobalt or Nickel

On April 21, 2026, at its "Beyond the Pole" Tech Day in Beijing, CATL unveiled the third generation of its Shenxing battery, claiming a 10%-to-98% charge in 6 minutes 27 seconds. The launch came six weeks after BYD unveiled its second-generation Blade Battery with a 10%-to-97% charge in around 9 minutes.