Precious Metals

October 29, 2024

2 min

Precious Metals

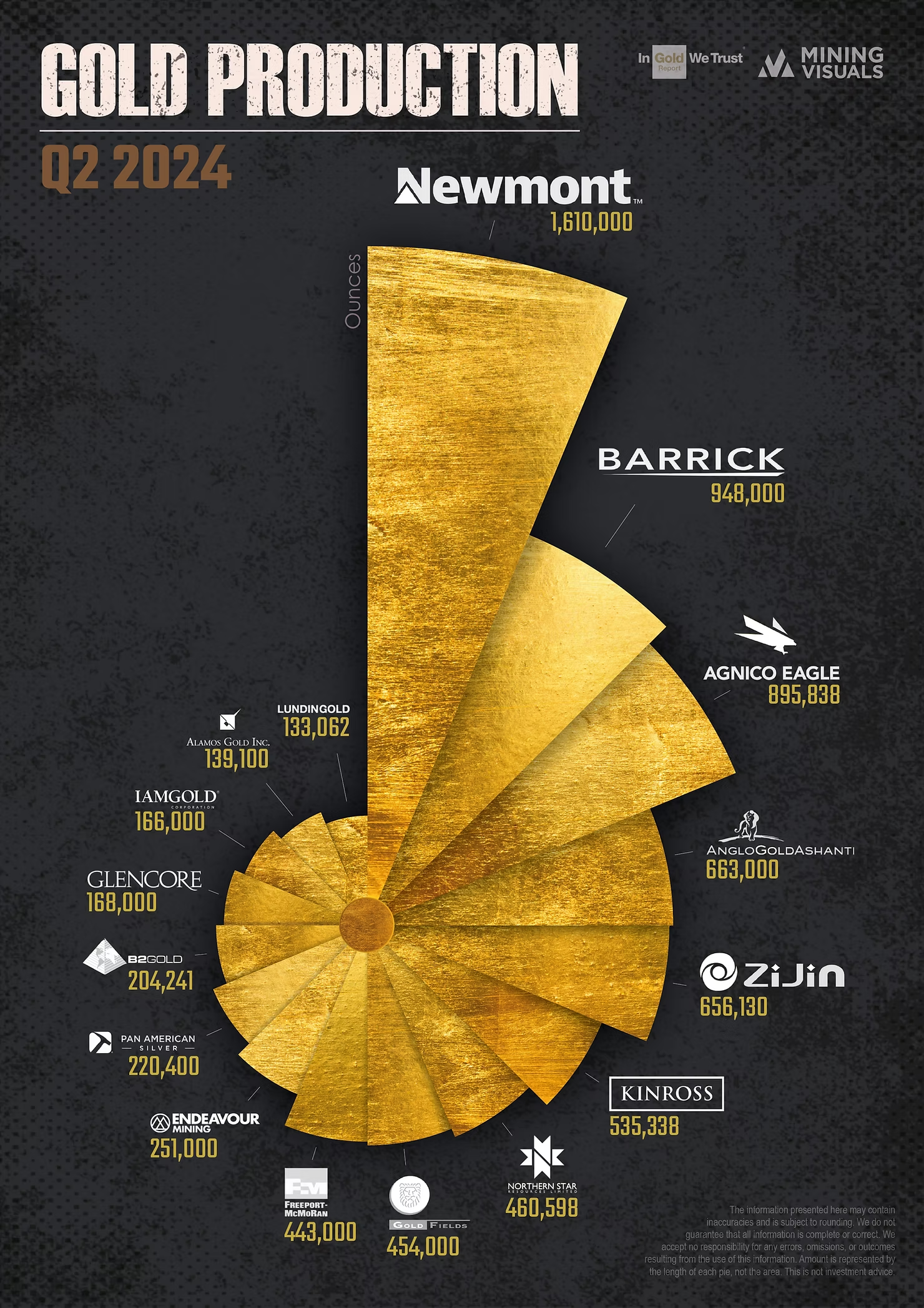

The second quarter of 2024 has shown dynamic shifts in gold production among major mining companies compared to the same period in 2023. Below is a closer look at how some of the leading gold producers performed, highlighting the top increases and decreases in production year-over-year.

Leaders in Production Growth

- Newmont Corporation reported a notable 29.84% increase in gold production, reaching 1,610,000 ounces in Q2 2024 compared to 1,240,000 ounces in Q2 2023.

- Iamgold Corp demonstrated the most impressive growth, with a 55.14% increase in production. The company produced 166,000 ounces in Q2 2024, up from 107,000 ounces in Q2 2023.

- Zijin Mining Group also saw a strong rise, increasing its production by 16.61% year-over-year. The company produced 656,130 ounces in Q2 2024 compared to 562,690 ounces in the same quarter last year, reinforcing its growth trajectory in the global market.

- Northern Star Resources production grew by 7.51% compared to Q2 2023.

Companies Facing Production Declines

- Gold Fields Ltd faced a significant production drop of 21.32%, with production falling to 454,000 ounces in Q2 2024 from 577,000 ounces in Q2 2023.

- Glencore PLC saw a 7.69% reduction in output, producing 168,000 ounces in Q2 2024 versus 182,000 ounces in Q2 2023.

- Barrick Gold Corp produced 948,000 ounces in Q2 2024, a 6.05% drop from the previous year’s 1,009,000 ounces.

- Endeavour Mining PLC also reported a decline of 6.34%, with production dropping from 268,000 ounces in Q2 2023 to 251,000 ounces in Q2 2024.

- B2Gold Corp - production decreased by 16.96%, dropping from 245,961 ounces to 204,241 ounces.

Companies with Stable Production or Marginal Changes

In contrast to the larger fluctuations seen across the industry, several companies maintained relatively stable gold production in Q2 2024, with only minor changes from the previous year. The companies with the smallest changes were:

- Agnico Eagle Mines Ltd (Ontario) – A modest increase of 2.59%, from 873,204 ounces to 895,838 ounces.

- Alamos Gold Inc – Production rose by 2.28%, moving from 136,000 ounces to 139,100 ounces.

- Lundin Gold Inc – Production grew by 2.57%, from 129,731 ounces to 133,062 ounces.

- Pan American Silver - Production declined by 1.28%, with production at 220,400 ounces, slightly down from 223,258 ounces in Q2 2023.

- Kinross Gold Corp experienced a slight decrease of 3.55%, from 555,036 ounces in Q2 2023 to 535,338 ounces in Q2 2024.

The information presented here may contain inaccuracies and is subject to rounding. We do not guarantee that all information is complete or correct. We accept no responsibility for any errors, omissions, or outcomes resulting from the use of this information. This is not investment advice.

Explore More

View All

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

In early 2026, the artificial intelligence narrative shifted abruptly from software capabilities to physical hardware constraints. With tech giants committing hundreds of billions to new infrastructure—pushing global hyperscaler capital expenditures past $600 billion this year—the industry has collided with a new primary bottleneck: a severe power and thermal crunch.

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Somewhere inside a pressurized-water reactor, an alloy that is four-fifths silver is absorbing neutrons to keep the core in check, a job most silver investors have never heard of. It is a useful reminder that the metal people picture as coins and jewelry mostly works elsewhere, across industry.

Ranked: The Countries That Produced the Most Silver in 2025

Ranked: The Countries That Produced the Most Silver in 2025

Mexico remained the world's top silver-producing country in 2025, mining 172.9 million ounces (Moz), roughly a fifth of global supply, according to the World Silver Survey 2026, produced for the Silver Institute by Metals Focus. But Mexico's lead narrowed: its output fell 5% for a third straight year, while second-place Peru climbed 7%. Global mine production rose 3% to 846.6 Moz, even as the ranking's top tier told a story of one leader sliding and its closest rival closing in.

Electric Vehicles Are Set to Become the Auto Industry's Biggest Silver Consumer by 2027

Electric Vehicles Are Set to Become the Auto Industry's Biggest Silver Consumer by 2027

Most of silver's 2026 story has been told from the supply side: a sixth straight year of structural deficit and a record price near $121 in January. Less examined is where the next leg of industrial demand actually comes from. With solar, silver's largest industrial use, now facing thrifting and substitution, the Silver Institute points to a quieter end-use picking up the slack: the automotive sector. A December 2025 study from Oxford Economics and the Silver Institute quantifies that shift, and the engine behind it is the electric vehicle.