Precious Metals

January 10, 2025

2 min

Precious Metals

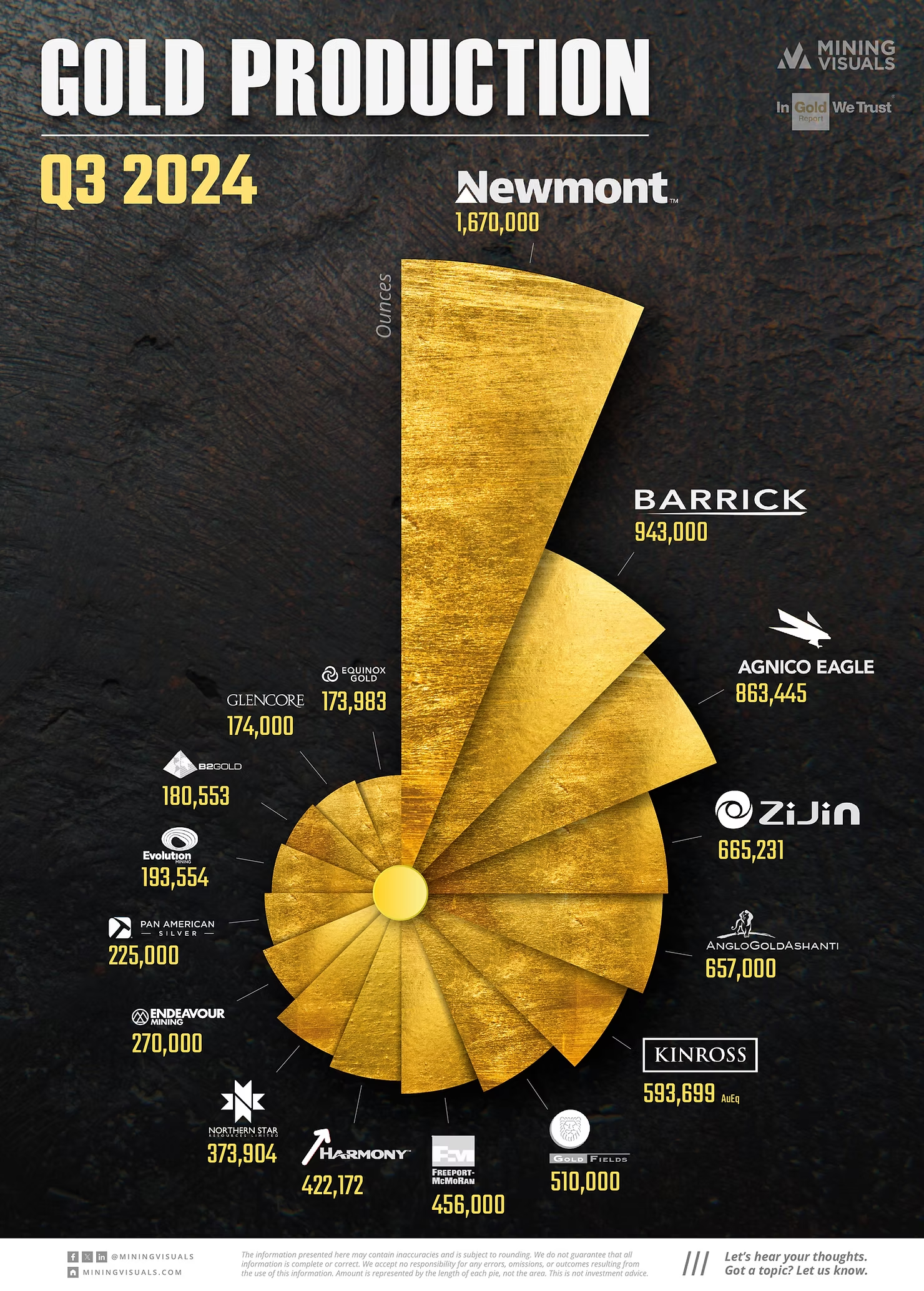

In this graphic and article, we examine gold production by the world's largest producers in Q3 2024, comparing it to the same period in 2023. Explore the shifts in production levels and the factors behind these changes.

Top Producers and Performance

- Newmont Corporation retained its top spot with 1,670,000 ounces, a significant 29.46% increase from Q3 2023. This growth came from higher output at the Cerro Negro mine in Argentina and the integration of Newcrest's assets, including the Lihir project.

- Barrick Gold Corp produced 943,000 ounces, down 9.24% due to lower output at its Nevada operations (Carlin and Cortez mines). However, Barrick expects a stronger Q4 to meet its full-year target.

- Agnico Eagle Mines Ltd showed a modest 1.53% growth, producing 863,445 ounces, maintaining steady output.

Growth Leaders

- Evolution Mining Ltd saw a 22.27% increase, reaching 193,554 ounces due to operational improvements at Red Lake in Ontario and higher-grade ore processing.

- Equinox Gold Corp posted 16.70% growth with 173,983 ounces, driven by the ramp-up of the Greenstone Mine.

- Zijin Mining Group continued its upward trend, increasing output by 6.24% to 665,231 ounces.

Declines Among Major Players

- Freeport-McMoRan Inc had the steepest decline, with a 14.29% drop to 456,000 ounces due to lower ore grades.

- B2Gold Corp's production fell by 25.65% to 180,553 ounces, mainly due to delays in accessing high-grade ore, equipment issues, and adverse weather at its Fekola Mine.

- AngloGold Ashanti PLC and Gold Fields Ltd reported moderate declines of 2.81% and 5.90%, respectively.

Steady Performers

- Kinross Gold Corp (593,699 ounces, +1.41%) and Northern Star Resources Ltd (373,904 ounces, +1.33%) maintained consistent production with stable operations.

Source: Company reports

Explore More

View All

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

In early 2026, the artificial intelligence narrative shifted abruptly from software capabilities to physical hardware constraints. With tech giants committing hundreds of billions to new infrastructure—pushing global hyperscaler capital expenditures past $600 billion this year—the industry has collided with a new primary bottleneck: a severe power and thermal crunch.

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Somewhere inside a pressurized-water reactor, an alloy that is four-fifths silver is absorbing neutrons to keep the core in check, a job most silver investors have never heard of. It is a useful reminder that the metal people picture as coins and jewelry mostly works elsewhere, across industry.

Ranked: The Countries That Produced the Most Silver in 2025

Ranked: The Countries That Produced the Most Silver in 2025

Mexico remained the world's top silver-producing country in 2025, mining 172.9 million ounces (Moz), roughly a fifth of global supply, according to the World Silver Survey 2026, produced for the Silver Institute by Metals Focus. But Mexico's lead narrowed: its output fell 5% for a third straight year, while second-place Peru climbed 7%. Global mine production rose 3% to 846.6 Moz, even as the ranking's top tier told a story of one leader sliding and its closest rival closing in.

Electric Vehicles Are Set to Become the Auto Industry's Biggest Silver Consumer by 2027

Electric Vehicles Are Set to Become the Auto Industry's Biggest Silver Consumer by 2027

Most of silver's 2026 story has been told from the supply side: a sixth straight year of structural deficit and a record price near $121 in January. Less examined is where the next leg of industrial demand actually comes from. With solar, silver's largest industrial use, now facing thrifting and substitution, the Silver Institute points to a quieter end-use picking up the slack: the automotive sector. A December 2025 study from Oxford Economics and the Silver Institute quantifies that shift, and the engine behind it is the electric vehicle.