Copper

April 10, 2025

2 min

Copper

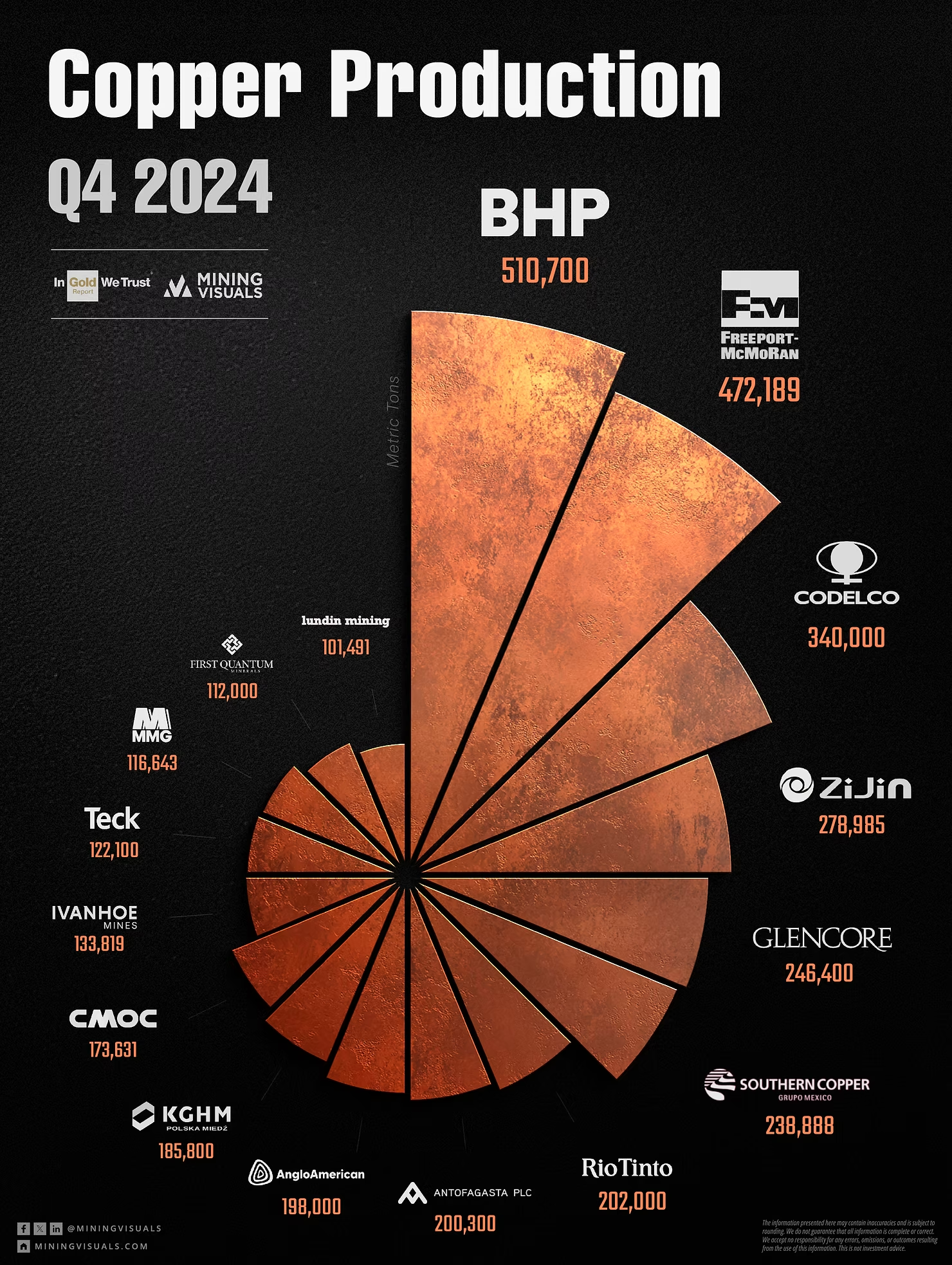

The latest Q4 numbers are in. In this graphic and article, we take a look at the companies that produced the most copper in the final quarter of 2024 — and how their performance stacked up against the same period last year.

BHP Takes the Lead

BHP topped the list with 510,700 tonnes of copper produced in Q4, marking a 16.8% increase compared to the same quarter in 2023. The boost came largely from its flagship Escondida mine in Chile, where higher ore grades drove production growth as richer zones were accessed according to plan.

Freeport-McMoRan secured the second spot with 472,189 tonnes of copper produced in Q4 2024 — a slight decline of 4.9% compared to the same period last year.

Codelco ranked third for the quarter, delivering 340,000 tonnes. This marked a 5.0% decrease year-over-year.

Strongest Year-over-Year Increases

- Ivanhoe Mines recorded a 45.1% increase, producing 133,819 tonnes. The jump was driven by the ramp-up of its Phase 3 concentrator at the Kamoa-Kakula complex in the DRC, which reached (and even exceeded) design capacity during the quarter.

- MMG reported 116,643 tonnes, up 43.6% YoY. This was supported by new output from the Khoemacau mine, acquired earlier in 2024, and a strong quarter at Las Bambas, which benefited from access to the Chalcobamba pit and stable operations.

- Rio Tinto produced 202,000 tonnes, a 26.3% increase compared to Q4 2023. Gains came from the continued ramp-up of the Oyu Tolgoi underground mine in Mongolia, alongside improved grades at Escondida.

Declines to Note

- First Quantum Minerals saw production fall 30.1% YoY to 112,000 tonnes, largely due to the suspension of its Cobre Panama mine, which contributed zero output this quarter versus 63,000 tonnes in Q4 last year.

- Anglo American reported a 13.9% decline, producing 198,000 tonnes. The drop stemmed from planned changes in Chile, including the closure of a smaller plant at Los Bronces and lower expected grades at Collahuasi.

Source: Company Reports

Disclaimer: The production figures and analysis presented in this article are based on publicly available company reports and data pertaining to the fourth quarter (Q4) of 2024, with comparisons made to Q4 2023. Explanations for production changes are derived from company statements and operational reviews available as of April 2025. While efforts have been made to ensure accuracy, this information is for informational purposes only and does not constitute investment advice. Readers should conduct their own research and consult with a qualified financial advisor before making 1 investment decisions. Data is subject to revision by the reporting companies.

Explore More

View All

Ranked: The World's Largest Copper Mines (2025)

Ranked: The World's Largest Copper Mines (2025)

Copper has spent 2026 setting records, touching an intraday COMEX high of $6.71 per pound on May 13 amid AI-driven demand and supply shocks, against a backdrop where the ICSG now forecasts a 150,000-tonne deficit for 2026. In a market this tight, where the deficit thesis turns on lost tonnes, the question of where the world's copper actually comes from carries unusual weight.

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper has spent most of 2026 doing something it had not done in a quarter century: setting fresh records every few weeks. The COMEX contract printed an intraday all-time high of $6.71 per pound on May 13, and the May monthly close looks set to land at the top of the historical chart. In London, copper traded above $14,000 per tonne in mid-May, touching $14,196.50, within reach of the LME's January 29 record of $14,527.50.

The Cost of Mining Copper: A 2024–2025 Update

The Cost of Mining Copper: A 2024–2025 Update

Copper futures touched an all-time high above $6.58 per pound on May 12, 2026, capping a 40.86% gain over the prior twelve months as supply tightness collided with structural demand from grid build-out, electric vehicles, and AI data centers. Earlier in the year, the LME benchmark rallied 22% to a record $13,387 per tonne on January 6, 2026. Behind the price action lies a less-discussed story: what it actually costs the world's largest miners to pull a pound of copper out of the ground.

Copper Production Q4 2025

Copper Production Q4 2025

As power-hungry AI data centers drive a projected 2-million-ton surge in global copper demand by 2030, market attention remains fixated on the supply side. Fourth-quarter 2025 metrics provide a definitive look at how the world's top miners closed out the year. While overall volumes remain heavily concentrated among a few historic industry giants, the true Q4 narratives emerged further down the list, as mid-tier producers leveraged flagship asset expansions to hit multi-year highs and offset the sector's ongoing struggle with declining ore grades.