Copper

December 16, 2024

2 min

Copper

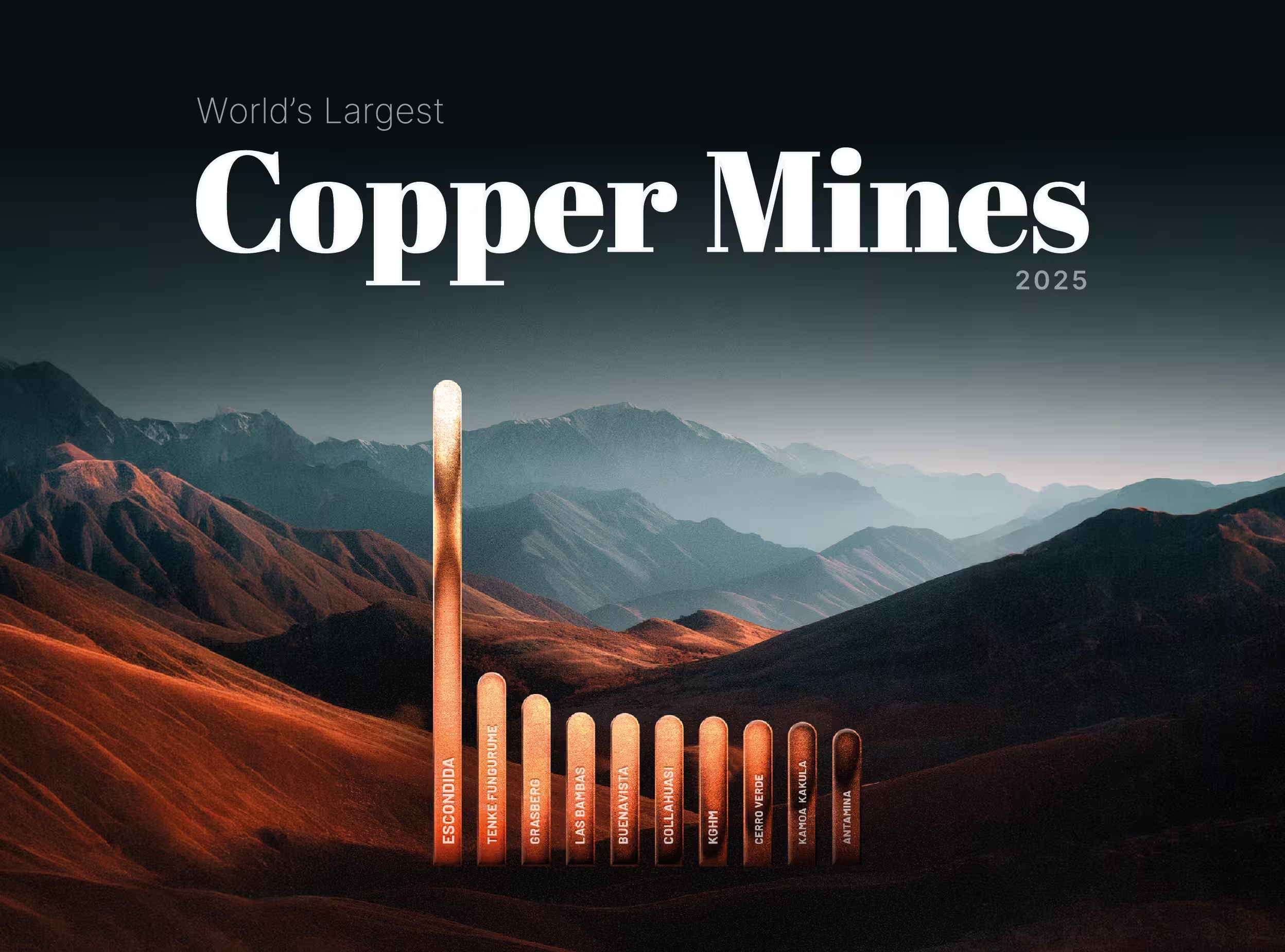

In 2024, the world’s largest copper mines by annual production capacity are spread across various continents, with Latin America leading the charge. At the top is Escondida in Chile, the largest copper mine globally, with a production capacity of 1.35 million metric tons per year. Owned by BHP and Rio Tinto, Escondida is crucial to both Chile's economy and the global copper supply.

Grasberg, located in Papua Province, Indonesia, is the second-largest copper mine with an annual capacity of 770 kt. It’s also one of the world’s richest gold mines, significantly contributing to Indonesia's economy. Co-owned by PT Freeport Indonesia and the government, it plays a key role in the global copper and gold markets.

Collahuasi, located in northern Chile, has an annual copper production capacity of 640 kt and operates at high altitudes in the Atacama Desert. Co-owned by Anglo American and Glencore, it is a major contributor to Chile's economy. The mine is known for its advanced technology and commitment to sustainability and local communities.

In North America, Morenci in Arizona leads with an annual capacity of 570 kt. It is operated by Freeport-McMoRan in partnership with Sumitomo Corporation. Close behind is Mexico's Buenavista del Cobre, with a capacity of 535 k. It is owned by Grupo México and includes open-pit operations and significant leaching facilities.

Antamina (450 kt) and Cerro Verde II (500 kt) are two of Peru's largest copper mines. Antamina is co-owned by BHP, Glencore, and other partners. Cerro Verde II, operated by Freeport-McMoRan and partners. Russia's Polar Division (450 kt), owned by Norilsk Nickel, is a key supplier of copper and nickel. In Africa, the Kamoa-Kakula mine in the Democratic Republic of Congo (420 kt), owned by Ivanhoe Mines, Zijin Mining, and the DRC government, is rapidly expanding.

Other notable mines include Chile’s El Teniente (402 kt), Chuquicamata, and Los Pelambres, Peru’s Las Bambas and Toromocho, and Zambia’s Kansanshi. Central America’s Cobre Panama and the U.S.’s Bingham Canyon are also critical contributors.

Together, these mines represent the global copper mining industry's top annual production capacities, vital for supporting the increasing demand for copper in construction, electronics, and renewable energy technologies. Latin America, led by Chile, remains the dominant force in the sector.

Source: The World Copper Factbook 2024

Explore More

View All

Ranked: The World's Largest Copper Mines (2025)

Ranked: The World's Largest Copper Mines (2025)

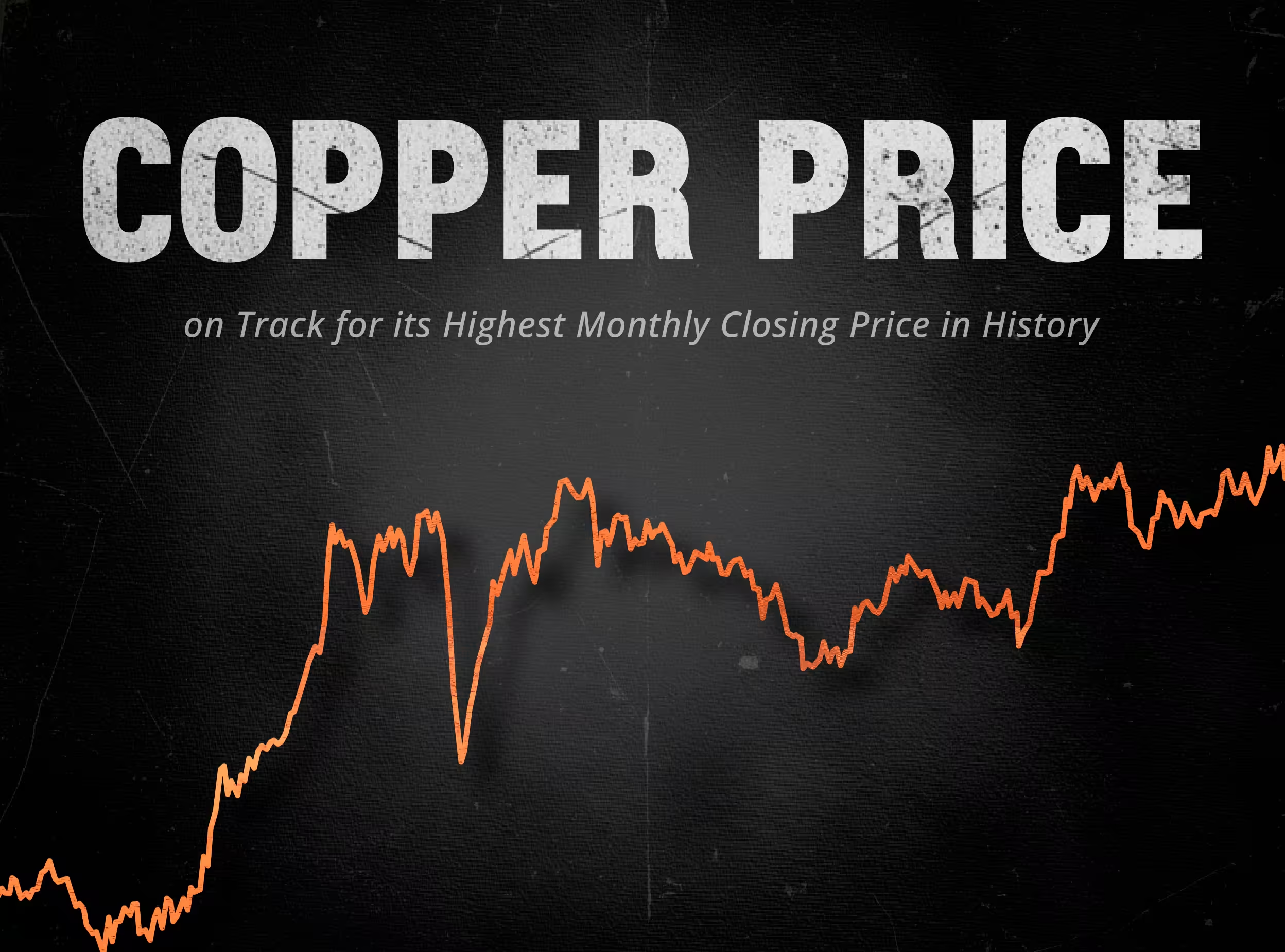

Copper has spent 2026 setting records, touching an intraday COMEX high of $6.71 per pound on May 13 amid AI-driven demand and supply shocks, against a backdrop where the ICSG now forecasts a 150,000-tonne deficit for 2026. In a market this tight, where the deficit thesis turns on lost tonnes, the question of where the world's copper actually comes from carries unusual weight.

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper has spent most of 2026 doing something it had not done in a quarter century: setting fresh records every few weeks. The COMEX contract printed an intraday all-time high of $6.71 per pound on May 13, and the May monthly close looks set to land at the top of the historical chart. In London, copper traded above $14,000 per tonne in mid-May, touching $14,196.50, within reach of the LME's January 29 record of $14,527.50.

The Cost of Mining Copper: A 2024–2025 Update

The Cost of Mining Copper: A 2024–2025 Update

Copper futures touched an all-time high above $6.58 per pound on May 12, 2026, capping a 40.86% gain over the prior twelve months as supply tightness collided with structural demand from grid build-out, electric vehicles, and AI data centers. Earlier in the year, the LME benchmark rallied 22% to a record $13,387 per tonne on January 6, 2026. Behind the price action lies a less-discussed story: what it actually costs the world's largest miners to pull a pound of copper out of the ground.

Copper Production Q4 2025

Copper Production Q4 2025

As power-hungry AI data centers drive a projected 2-million-ton surge in global copper demand by 2030, market attention remains fixated on the supply side. Fourth-quarter 2025 metrics provide a definitive look at how the world's top miners closed out the year. While overall volumes remain heavily concentrated among a few historic industry giants, the true Q4 narratives emerged further down the list, as mid-tier producers leveraged flagship asset expansions to hit multi-year highs and offset the sector's ongoing struggle with declining ore grades.