Copper

September 18, 2024

2 min

Copper

Codelco, one of the world’s largest copper producers, is facing increasing costs as it battles several operational challenges. Chief among them are declining ore grades, aging infrastructure, and rising expenses related to labor, materials, and energy. As the global copper market remains competitive, these factors are placing significant strain on the company’s profitability and production efficiency.

One of the primary challenges is the decreasing quality of copper ore, particularly in some of Codelco’s oldest and largest mines, such as Chuquicamata and El Teniente. As ore grades decline, more material must be processed to extract the same volume of copper, significantly driving up operational costs. The lower-quality ore also requires more energy and water for processing, which further inflates expenses. In addition, the extraction of lower-grade ore produces more waste, complicating environmental management and increasing sustainability-related costs.

Alongside these issues, Codelco has seen rising third-party service costs and higher treatment and refining charges (TC-RC), contributing to the upward trend in operational expenses. Maintenance and labor costs are also increasing, making it harder for the company to maintain profitability.

To address these challenges, Codelco has embarked on ambitious modernization projects across its operations, particularly at Chuquicamata and El Teniente. These projects aim to access deeper, higher-grade ore bodies and extend the life of the mines. However, these initiatives require significant capital expenditures and have faced delays and disruptions, adding to the company’s cost pressures.

Codelco is also investing in automation, technology upgrades, and sustainability initiatives to improve efficiency and reduce long-term expenses. Automation is expected to enhance productivity, while technology upgrades should make mining processes more cost-effective. However, the full benefits of these efforts may take time to materialize, and in the short term, Codelco continues to struggle with rising costs and fluctuating production levels.

In summary, Codelco’s profitability and production are under pressure due to a combination of declining ore grades, aging mines, and rising operational expenses. While the company is taking steps to address these challenges through modernization and innovation, the road ahead remains complex and costly. For now, Codelco remains at the forefront of the global copper industry, but sustaining its position will require overcoming significant obstacles.

Source: Cochilco, YEARBOOK: COPPER AND OTHER MINERAL STATISTICS

The information presented here may contain inaccuracies and is subject to rounding. We do not guarantee that all information is complete or correct. We accept no responsibility for any errors, omissions, or outcomes resulting from the use of this information. This is not investment advice.

Explore More

View All

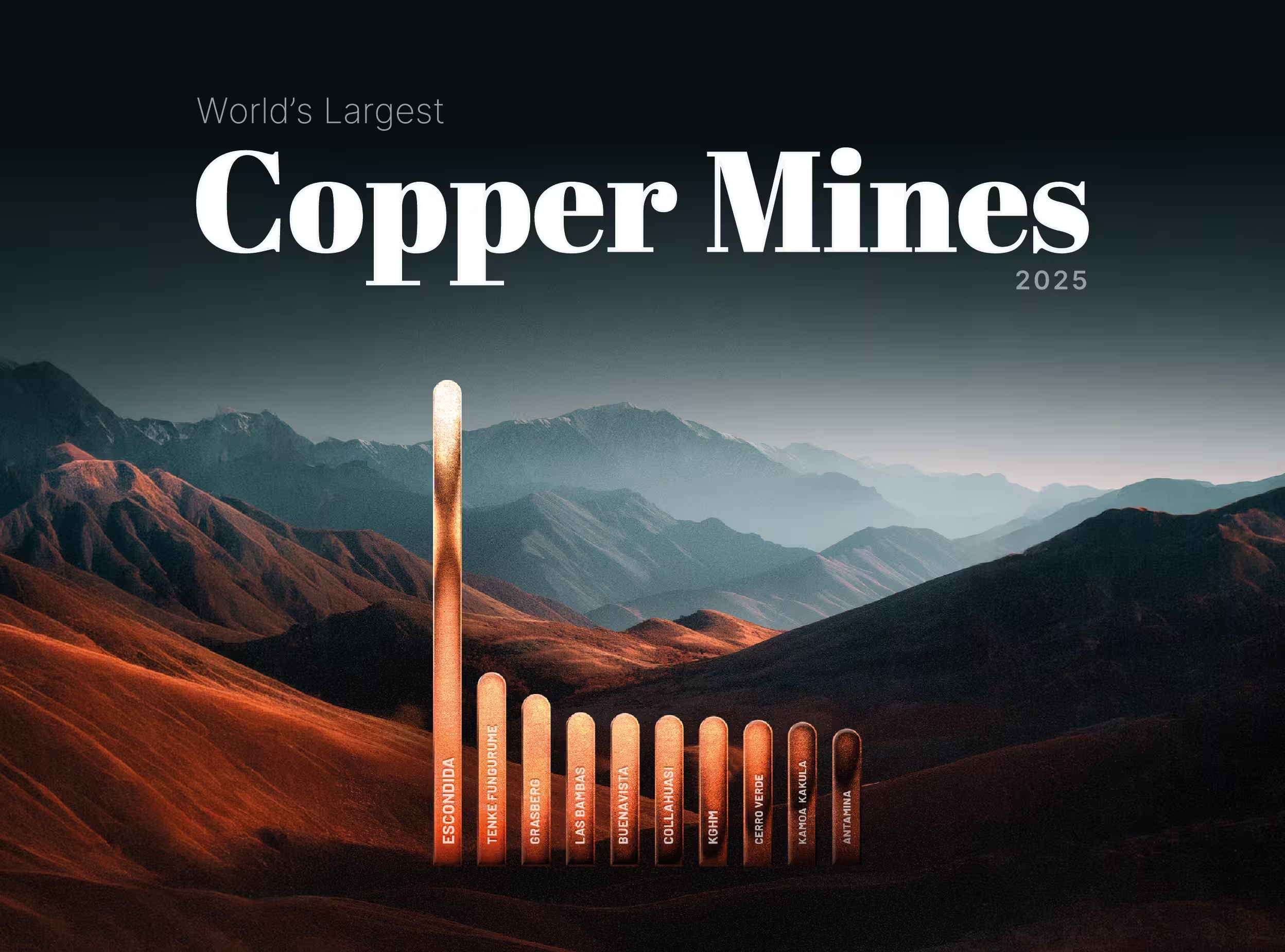

Ranked: The World's Largest Copper Mines (2025)

Ranked: The World's Largest Copper Mines (2025)

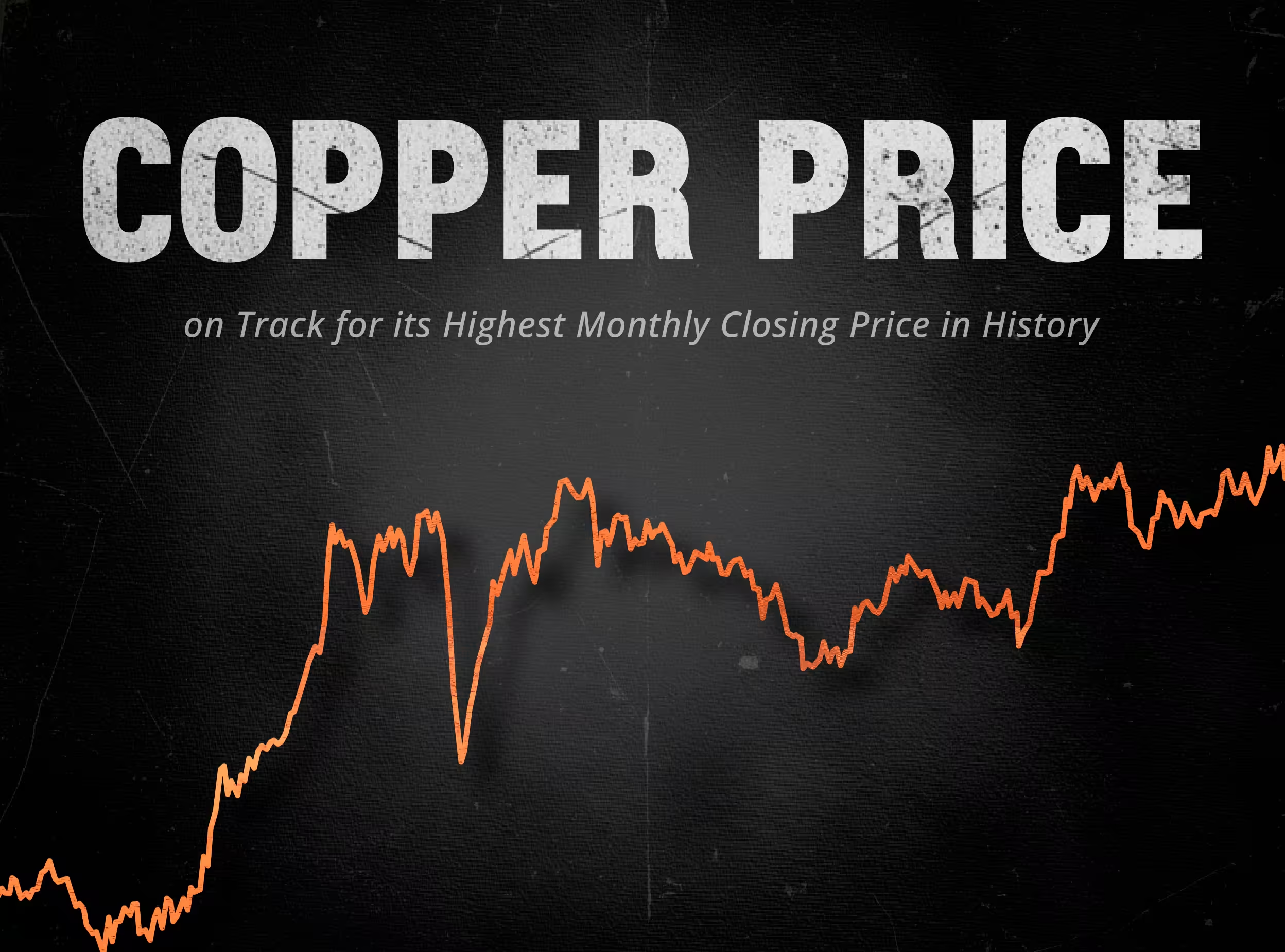

Copper has spent 2026 setting records, touching an intraday COMEX high of $6.71 per pound on May 13 amid AI-driven demand and supply shocks, against a backdrop where the ICSG now forecasts a 150,000-tonne deficit for 2026. In a market this tight, where the deficit thesis turns on lost tonnes, the question of where the world's copper actually comes from carries unusual weight.

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper has spent most of 2026 doing something it had not done in a quarter century: setting fresh records every few weeks. The COMEX contract printed an intraday all-time high of $6.71 per pound on May 13, and the May monthly close looks set to land at the top of the historical chart. In London, copper traded above $14,000 per tonne in mid-May, touching $14,196.50, within reach of the LME's January 29 record of $14,527.50.

The Cost of Mining Copper: A 2024–2025 Update

The Cost of Mining Copper: A 2024–2025 Update

Copper futures touched an all-time high above $6.58 per pound on May 12, 2026, capping a 40.86% gain over the prior twelve months as supply tightness collided with structural demand from grid build-out, electric vehicles, and AI data centers. Earlier in the year, the LME benchmark rallied 22% to a record $13,387 per tonne on January 6, 2026. Behind the price action lies a less-discussed story: what it actually costs the world's largest miners to pull a pound of copper out of the ground.

Copper Production Q4 2025

Copper Production Q4 2025

As power-hungry AI data centers drive a projected 2-million-ton surge in global copper demand by 2030, market attention remains fixated on the supply side. Fourth-quarter 2025 metrics provide a definitive look at how the world's top miners closed out the year. While overall volumes remain heavily concentrated among a few historic industry giants, the true Q4 narratives emerged further down the list, as mid-tier producers leveraged flagship asset expansions to hit multi-year highs and offset the sector's ongoing struggle with declining ore grades.