Copper

October 31, 2024

3 min

Copper

In this article, we take a closer look at BHP’s latest report, BHP Insights: How Copper Will Shape Our Future, which projects a 70% surge in copper demand by 2050—an increase of 22.1 Mt from 2021 levels. To put this in perspective, 22.1 Mt is equivalent to the output of more than 16 Escondida mines running at full capacity (Escondida being the largest copper mine in the world). This growth in demand is expected to be fueled by three main drivers: traditional economic expansion, the global energy transition, and rapid digitalization.

Introduction

Copper has been a crucial part of economic growth and technological development for decades. Now, as the world moves faster toward a more sustainable and electrified future, copper’s importance is set to rise. Urbanization, electric vehicles, renewable energy, and consumer goods are all driving this demand. For those in the mining and resource industries, staying on top of these trends is key to navigating what’s ahead.

Broad-Based Copper Demand

Unlike in the past, when tech adoption came in waves, the next 25 years will see a simultaneous surge in copper demand worldwide. Electrification, decarbonization, and digitization are happening everywhere at once, from electric cars and renewable energy systems to the expansion of data centers. Copper is at the heart of all this, and it’s clear that industries like construction, capital goods, and consumer products will need a lot more of it to keep up.

Key Sectors Driving Demand (BHP forecast)

Two sectors stand out as the biggest drivers of copper demand: transport and power infrastructure. These sectors are leading the charge in global electrification and renewable energy, and their need for copper is set to be huge.

That said, other sectors like construction, expected to see a 38.46% rise by 2050, capital goods with a 53.33% increase, and consumer goods with a 59.57% jump, will also drive up copper consumption. But let’s focus on the two most critical sectors that will shape copper’s future: transport and power infrastructure.

1. Transport: The Biggest Growth Sector

Copper demand in the transport sector is set to skyrocket, forecasted to increase by a staggering 223.53% by 2050. We’re talking about going from 3.4 million metric tons (Mt) in 2021 to 11 Mt in 2050. Electric vehicles (EVs), which require a lot more copper than traditional cars, are a big part of this. And it’s not just the cars—charging stations, electrified rail systems, and public transport expansions will also fuel the rise in demand. Copper’s conductivity, durability, and recyclability make it irreplaceable in these applications, even with ongoing attempts at substitution.

2. Power Infrastructure: The Backbone of the Energy Transition

Copper demand in power infrastructure is forecasted to rise by 69.09%, from 5.5 Mt in 2021 to 9.3 Mt by 2050. This sector’s growth is being driven by the expansion of renewable energy systems, which use far more copper than traditional energy grids. Whether it’s wind turbines, solar panels, or energy storage, copper is key for efficient transmission and storage.

Plus, copper’s relatively low carbon footprint—compared to alternatives like aluminum—makes it an even better choice as industries aim for decarbonization.

Conclusion

Copper’s role in the global economy is about to get even bigger as we shift to a more electrified, sustainable future. For professionals in the mining sector, this presents a huge opportunity to not only meet growing demand but also push for innovation and sustainability. Copper is undeniably at the center of what’s next for technology and infrastructure, and it’s here to stay.

Sponsored by:

Arras Minerals is a mining exploration company focused on copper and gold projects in northeast Kazakhstan, with key assets including Elemes, Tay, and Beskauga. The company also partners with Teck Resources on a 1,900 sq km exploration area funded by Teck. Arras aims to expand exploration in Kazakhstan's prolific mineral belts, leveraging untapped potential through drilling and geological surveys to define resources and grow its portfolio.

Learn more about Arras Minerals at https://www.arrasminerals.com/

Source: BHP, read the full report at https://www.bhp.com/news/bhp-insights/2024/09/how-copper-will-shape-our-future

The information presented here may contain inaccuracies and is subject to rounding. We do not guarantee that all information is complete or correct. We accept no responsibility for any errors, omissions, or outcomes resulting from the use of this information. This is not investment advice.

Explore More

View All

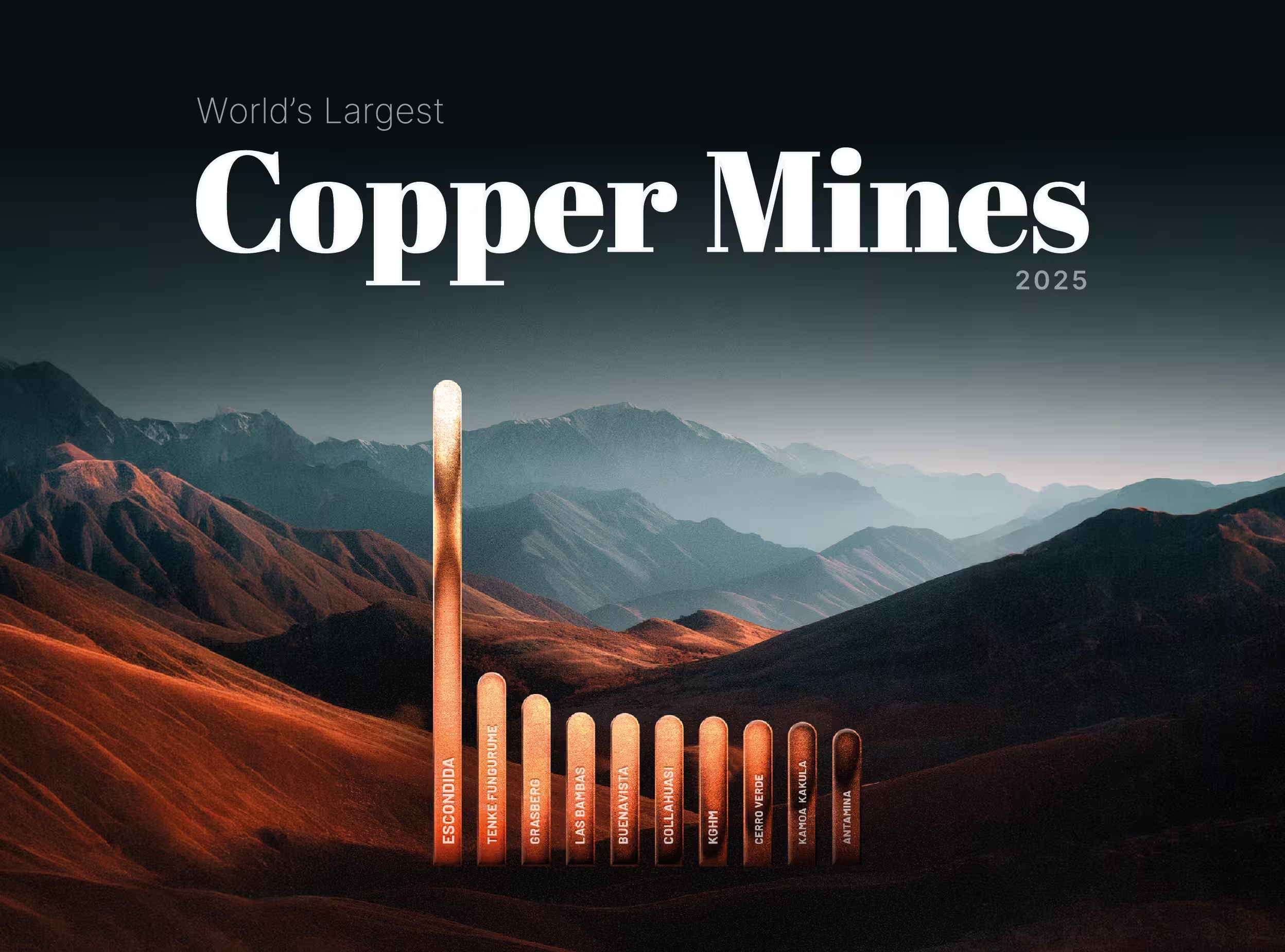

Ranked: The World's Largest Copper Mines (2025)

Ranked: The World's Largest Copper Mines (2025)

Copper has spent 2026 setting records, touching an intraday COMEX high of $6.71 per pound on May 13 amid AI-driven demand and supply shocks, against a backdrop where the ICSG now forecasts a 150,000-tonne deficit for 2026. In a market this tight, where the deficit thesis turns on lost tonnes, the question of where the world's copper actually comes from carries unusual weight.

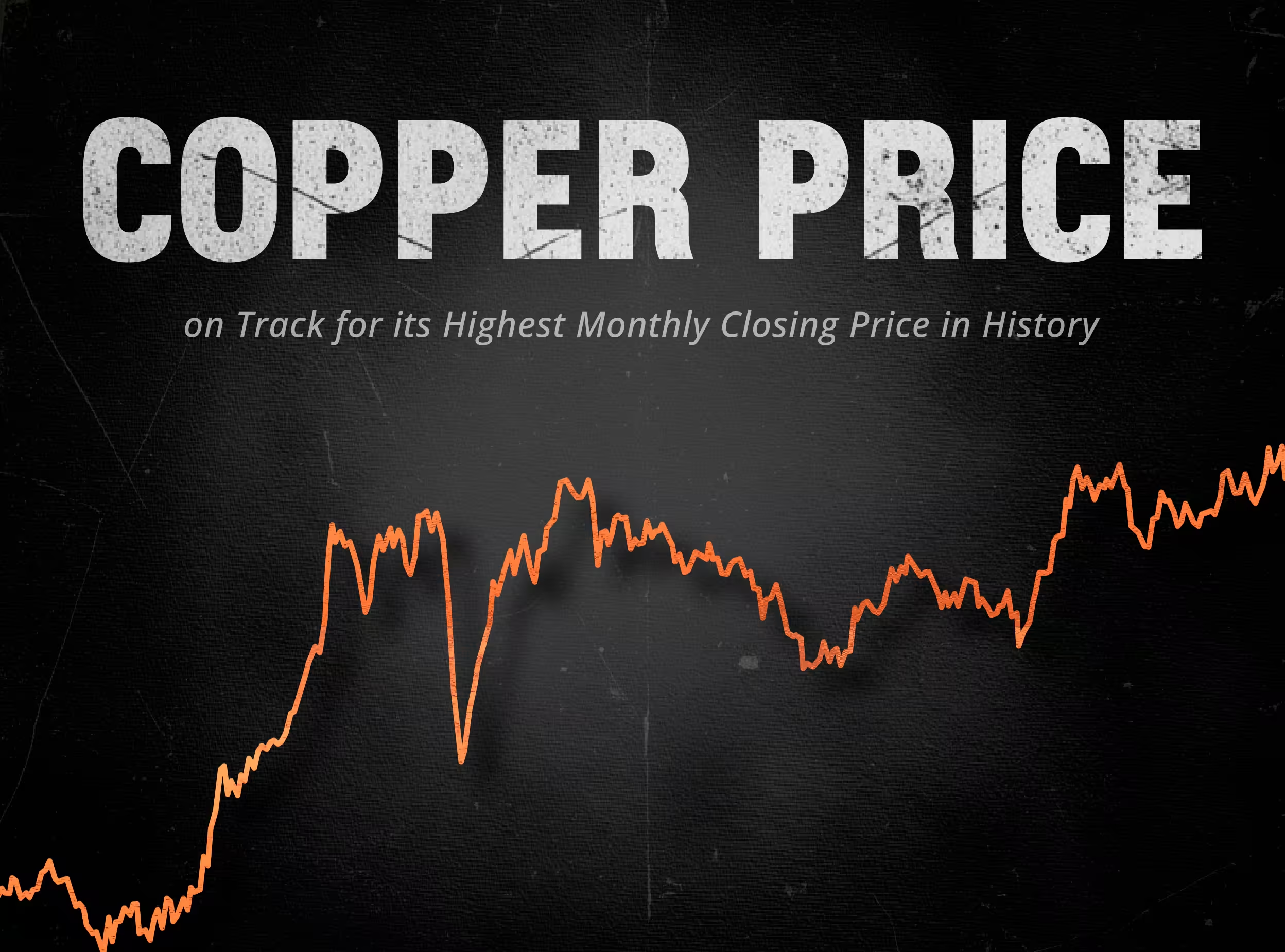

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper has spent most of 2026 doing something it had not done in a quarter century: setting fresh records every few weeks. The COMEX contract printed an intraday all-time high of $6.71 per pound on May 13, and the May monthly close looks set to land at the top of the historical chart. In London, copper traded above $14,000 per tonne in mid-May, touching $14,196.50, within reach of the LME's January 29 record of $14,527.50.

The Cost of Mining Copper: A 2024–2025 Update

The Cost of Mining Copper: A 2024–2025 Update

Copper futures touched an all-time high above $6.58 per pound on May 12, 2026, capping a 40.86% gain over the prior twelve months as supply tightness collided with structural demand from grid build-out, electric vehicles, and AI data centers. Earlier in the year, the LME benchmark rallied 22% to a record $13,387 per tonne on January 6, 2026. Behind the price action lies a less-discussed story: what it actually costs the world's largest miners to pull a pound of copper out of the ground.

Copper Production Q4 2025

Copper Production Q4 2025

As power-hungry AI data centers drive a projected 2-million-ton surge in global copper demand by 2030, market attention remains fixated on the supply side. Fourth-quarter 2025 metrics provide a definitive look at how the world's top miners closed out the year. While overall volumes remain heavily concentrated among a few historic industry giants, the true Q4 narratives emerged further down the list, as mid-tier producers leveraged flagship asset expansions to hit multi-year highs and offset the sector's ongoing struggle with declining ore grades.