Tin

December 9, 2025

4 min

Tin

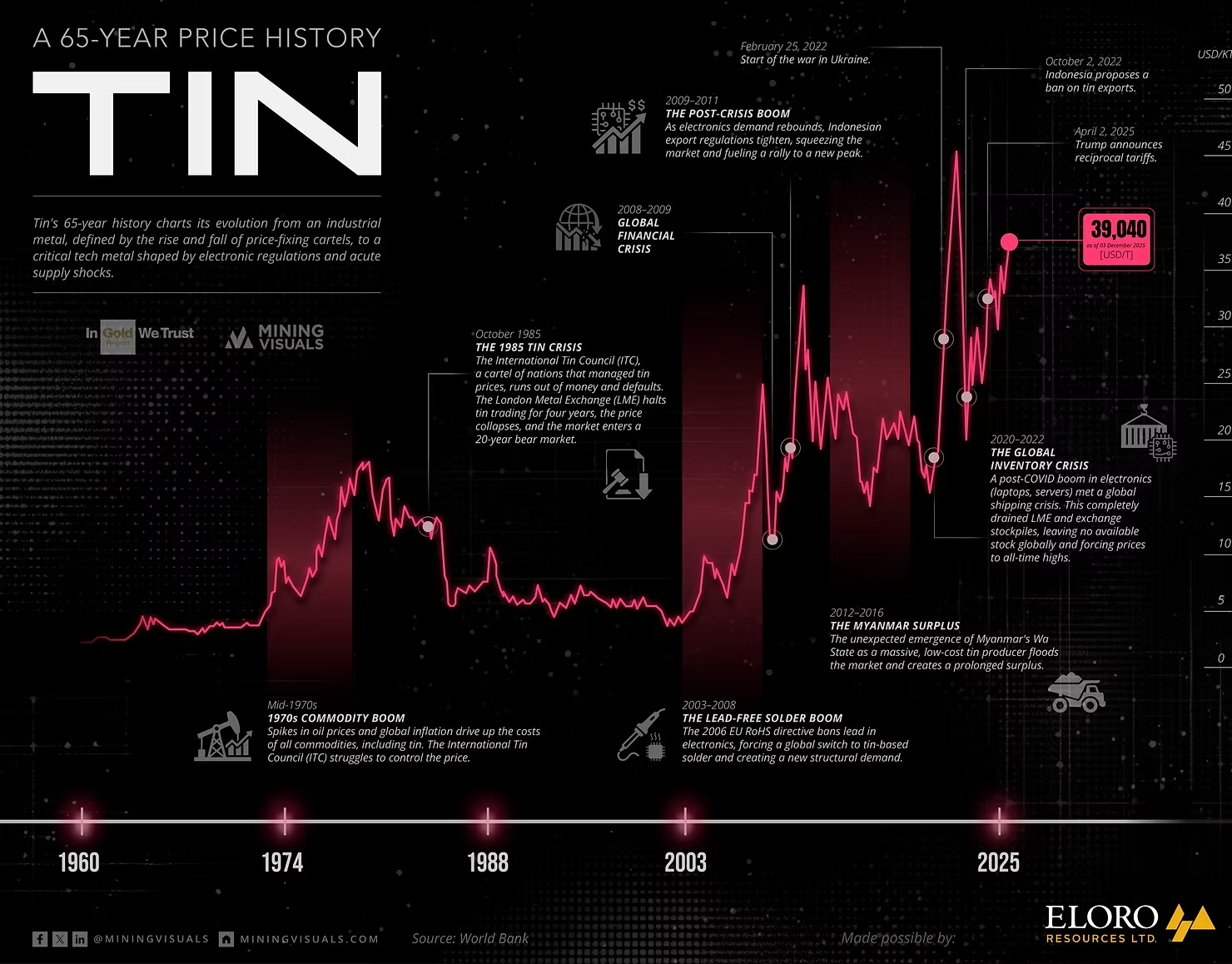

The 65-year price history of tin is a clear illustration of its dramatic evolution, from a price-fixed industrial commodity to a critical, strategic component at the heart of the global electronics industry.

As the chart shows, tin's journey is a volatile story, shaped not by a single factor, but by a complex interplay of speculative crises, cartel collapses, technological regulation, and acute, recurring supply shocks. Here is a deeper look at the events that defined tin's journey from 1960 to the present.

Part I: The Age of Cartels and Crises (1960–2002)

The first half of the chart is defined by the efforts of producers to manage—and ultimately fail to control—the metal's price through collective action.

- Mid-1970s: The 1970s Commodity Boom: The price first spiked significantly during the widespread commodity boom of the 1970s, driven by rising oil prices and global inflation. The market structure, however, was defined by The International Tin Council (ITC). This association of major producing and consuming nations was established to stabilize the market by managing a buffer stock, buying when prices were low and selling when they were high.

- 1985, The Tin Crisis: The ITC's attempt to control the price was a massive failure. Over several years, the ITC's managers bought up massive quantities of tin to keep the floor price high. By October 1985, they ran out of money and defaulted on their debts, leaving a large, unsellable buffer stock. The London Metal Exchange (LME) suspended tin trading until 1989 (a period of almost four years), and the price collapsed. This event marked the end of the market's artificially supported structure, fundamentally changing how the metal traded.

Part II: The Electronics Era (2003–Present)

After a period of relative stagnation following the ITC collapse, the market was permanently transformed by the rise of the global electronics industry and new environmental legislation.

2003–2008: The Lead-Free Solder Boom

The first major rally of the 21st century was not driven by a typical demand cycle but by a permanent, structural change in the market. The catalyst was the European Union's 2006 Restriction of Hazardous Substances (RoHS) directive.

- This legislation banned the use of several hazardous materials in electronics, most notably lead (Pb). The global industry, which had relied on tin-lead solder (typically 63% tin) for decades, was forced to switch to lead-free solder, which is often 95–99% tin.

The RoHS directive, aimed at preventing toxic e-waste and protecting human health, forced a global scramble for a replacement. The solution was lead-free solder, and its primary component is tin. This 'legislative boom' created a massive new demand floor for the metal, permanently and intrinsically linking the price of tin to the future growth of the entire electronics industry.

- This shift was monumental, creating a new demand floor for the metal and intrinsically linking the price of tin to the future growth of the entire electronics industry.

2008–2011: Crisis, Collapse, and Rebound

- 2008–2009 Global Financial Crisis: The market's upward climb was abruptly halted. As global economies seized up, demand for consumer electronics and automobiles evaporated, causing a sharp price decline.

- 2009–2011 Post-Crisis Boom: The recovery was dramatic, fueled by massive government stimulus and resurgent electronics demand. However, a new factor emerged: supply-side anxiety. Indonesian export regulations began to tighten, providing the first major signal that the tin supply chain was fragile and sending prices to a new peak.

2012–2016: The Myanmar Surplus

The market's supply fears were unexpectedly and completely reversed by the emergence of a massive, low-cost tin source: Myanmar's Wa State. This "Myanmar Surplus" rapidly flooded the market, overwhelming demand, breaking the post-2011 rally, and pushing the market into a prolonged multi-year bear market.

2020–2022: The "Perfect Storm" and All-Time Highs

The period from 2020 onward represents the most volatile in tin's history, a phenomenon labeled The Global Inventory Crisis on the chart.

- The "Work From Home" boom created increased demand for electronics (laptops, servers).

- Simultaneously, global shipping chains fractured and smelters were shut down by lockdowns, creating an acute supply crunch.

- The resulting imbalance sent prices parabolic, culminating in the all-time high of $50,000/tonne seen on February 25, 2022, coinciding with the start of the war in Ukraine.

2022–2025: The New Geopolitical Volatility

The subsequent crash in 2022 was triggered by aggressive central bank interest rate hikes and the cooling of the post-COVID electronics boom. However, the market is now defined by acute geopolitical supply risk:

- October 2, 2022: Indonesia proposes a ban on tin exports. This threat of resource nationalism highlighted the market's supply-side fragility and helped establish a new price floor.

- April 2, 2025: Tit-for-tat reciprocal tariffs were announced, injecting massive uncertainty and inflationary pressure into global electronics supply chains, leading to the latest spike.

The story of tin is no longer just about industrial demand; it's about the intersection of technology, green energy (solar panels and EV batteries), and artificial intelligence, all balanced on a newly fragile supply chain.

Sponsored by:

Eloro Resources Ltd. is a mineral exploration company advancing a world-class silver and tin project in Bolivia’s historic Potosí Department. Its flagship asset, the Iska Iska Project, ranks among the top five undeveloped global resources in terms of scale for both tin and silver.

This significant grassroots discovery remains open in multiple directions, offering substantial potential for continued expansion and resource enhancement. Iska Iska benefits from strong infrastructure access and a deeply rooted presence in Bolivia, supported by an experienced management team and meaningful community engagement.

Eloro’s strategy is focused on resource growth, strategic partnerships, and establishing a leading position within the global mining sector.

Learn more at elororesources.com.

Sources

- Price Data: World Bank

- Market Analysis & Events: International Tin Association (ITA): Reports on market trends, including the impact of the RoHS directive, demand from solar PV, and future applications in green tech and AI.

- Reuters: News and analysis covering specific supply-side events, including Indonesian export policies and the 2023 mining ban in Myanmar's Wa State.

- European Commission: Information on the 2006 Restriction of Hazardous Substances (RoHS) directive, which mandated the shift to lead-free (tin-based) solder in electronics.

- Fastmarkets: Analysis on commodity demand, including the role of tin in electronics, AI data centers, and renewable energy technologies. Various Industry Reports (Industry): Analysis from mining and tech publications on the structural demand for tin in electronics, solder, and new applications like EV batteries and AI hardware.

Explore More

View All

Apple Outweighs Every Listed Miner on Earth, and It Is Not Even the Biggest Company

Apple Outweighs Every Listed Miner on Earth, and It Is Not Even the Biggest Company

One consumer-electronics company is now worth more than every publicly traded mining company on Earth combined. The graphic above captures the June 5 snapshot, when the 317 publicly traded miners tracked by CompaniesMarketCap were worth about $3.48 trillion

Three Weeks Public, SpaceX Already Approaches the Value of Every Listed Miner on Earth

Three Weeks Public, SpaceX Already Approaches the Value of Every Listed Miner on Earth

For 24 years SpaceX stayed private. Then, on June 12, 2026, it began trading on the Nasdaq in the largest IPO in history, priced at a $1.77 trillion valuation. Barely three weeks later the rocket and satellite maker is worth even more. As of early July, SpaceX carried a market capitalization of about $2.1 trillion, the seventh-highest of any public company on Earth, and it joins the Nasdaq-100 on July 7

Mapped: Zinc's Use Across Five Industries and the 2030 Demand Outlook

Mapped: Zinc's Use Across Five Industries and the 2030 Demand Outlook

We've covered zinc's role in energy, health, and sustainability before, alongside the supply base concentrated in a handful of mega-mines and the production map that has shifted toward Asia since the mid-1990s. The story of 2025 is what changed on the demand side. In November, the U.S. Geological Survey retained zinc on its final 2025 List of Critical Minerals.

Lithium Use Cases: Batteries Now Consume 88% of Global Supply

Lithium Use Cases: Batteries Now Consume 88% of Global Supply

In February 2026, the U.S. Geological Survey put a fresh number on a transformation that has been building for a decade: batteries now account for 88% of global lithium end-use, up from 87% a year earlier. The metal that once quietly toughened ceramics and thickened industrial greases has been almost entirely repurposed by the battery economy. As covered in our reporting on the shift from surplus to deficit, the supply side of this story is tightening.