Critical Minerals

January 14, 2026

3 min

Critical Minerals

In the opening weeks of 2026, the Arctic has once again become a center of a high-stakes geopolitical tug-of-war. President Trump’s renewed push for U.S. control or "strategic acquisition" of Greenland has reignited international tensions, framing the island not merely as a territorial ambition, but as a mandatory hedge against resource scarcity.

Greenland, in some ways, represents the "Final Frontier" of critical minerals—a necessary, if daunting, counterweight to a global supply chain currently anchored in Beijing.

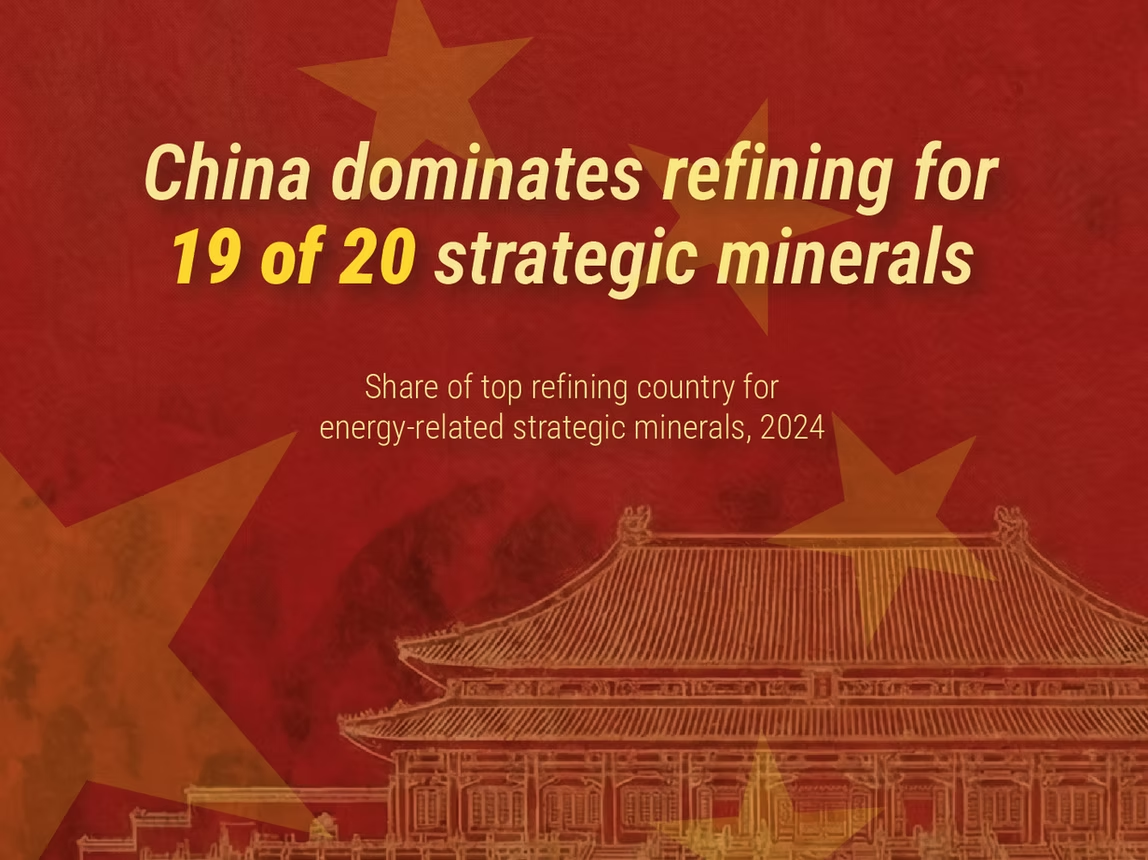

China’s Decades-Long Head Start

To understand why Greenland has become a 2026 flashpoint, one must look at the structural dominance of the People’s Republic of China. China’s lead in critical minerals—particularly Rare Earth Elements (REEs)—is the result of a deliberate, 40-year industrial strategy. As early as 1992, Deng Xiaoping famously remarked, “The Middle East has oil; China has rare earth elements.”

Today, that vision is a reality that the West is struggling to dismantle:

- Extraction: China mines approximately 60% of global REEs.

- Refining: Beijing controls over 85-90% of the world’s refining capacity.

- Downstream: China dominates nearly 90% of high-strength permanent magnet manufacturing, the core component for EV motors and defense systems.

Western reluctance to invest—stymied by high ESG hurdles and the "China Price" for processed oxides—has created a single-point-of-failure in the global supply chain. Greenland is increasingly viewed as an important part to break this monopoly.

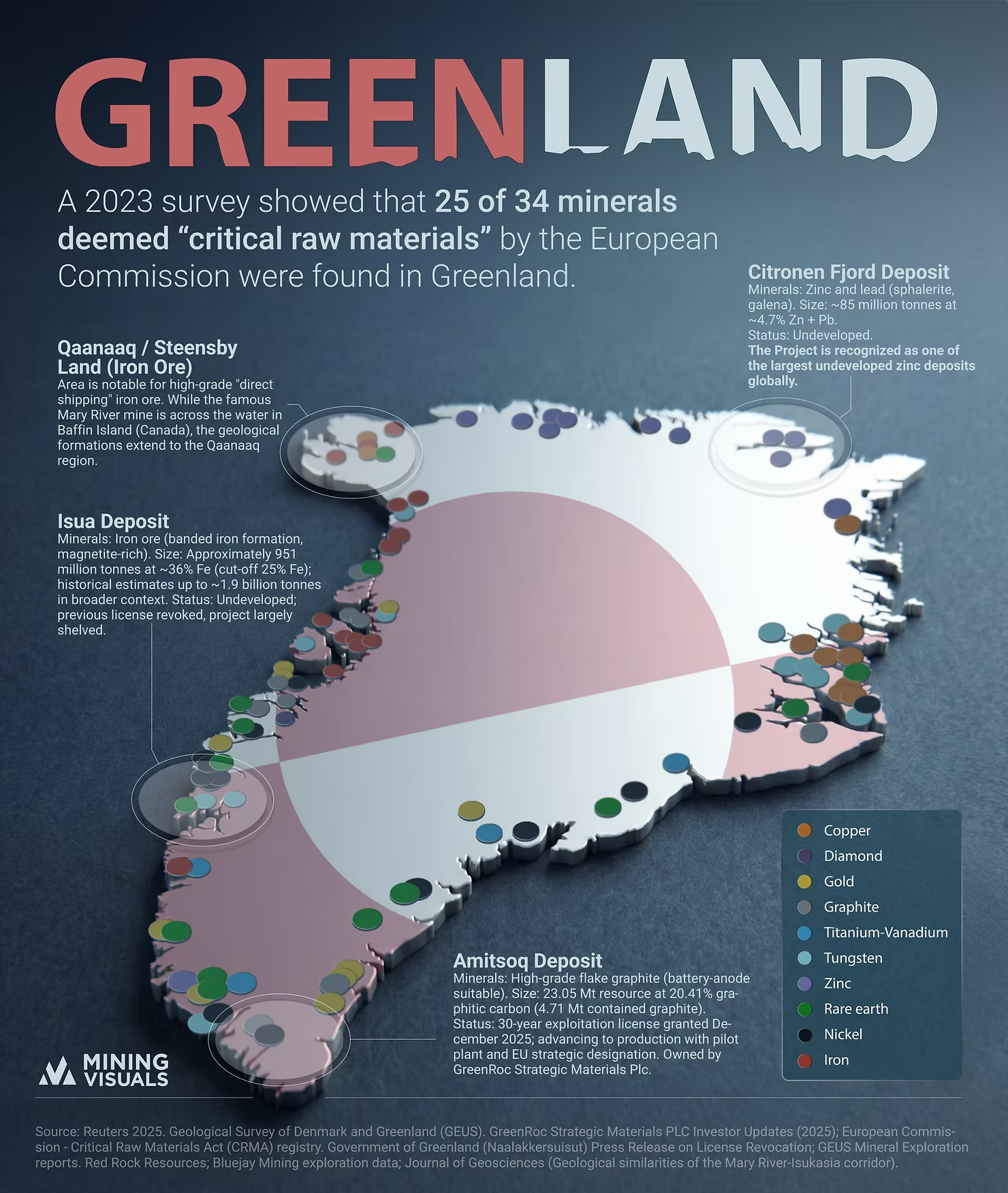

Greenland’s Geological Profile: 2026 Assessments

Greenland hosts 25 out of the 34 minerals deemed critical by the European Commission. The island's geology has concentrated deposits that are increasingly accessible as the ice sheet recedes.

The scale of the "untapped" potential is significant:

- Energy: The USGS estimates offshore oil and gas deposits at 31 to 42 billion barrels of oil equivalent.

- Rare Earths: Deposits such as Kvanefjeld and Tanbreez are among the world's largest multi-element resources, particularly rich in heavy REEs like dysprosium and terbium, which are essential for high-temperature magnets.

Key Resource Breakdown

The "Unsinkable Aircraft Carrier" and the Polar Silk Road

The strategic value of Greenland extends far beyond the mine pit, as the island sits at the heart of the GIUK (Greenland-Iceland-UK) Gap. This maritime bottleneck is essential for monitoring naval movements and securing the Pituffik Space Base, which remains the cornerstone of U.S. missile defense and space domain awareness. This "Great Power Competition" has manifested in the "Polar Silk Road," a Chinese strategy focused on securing long-term offtake agreements by offering to fund the very infrastructure—airports, ports, and power plants—that Western miners struggle to finance through traditional equity markets.

To counter this, the Trump administration’s 2026 rhetoric is increasingly backed by the threat of blocking Chinese Foreign Direct Investment (FDI) in favor of U.S.-led "Strategic Mineral Partnerships." This tension is further amplified by the accelerating viability of the Northern Sea Route, which promises to reduce transit times between Asian manufacturing hubs and European markets by 40%, effectively turning Greenland into a strategic tollgate for 21st-century commerce.

The Investment Reality: CAPEX, Risk, and Generational Returns

For the mining professional, Greenland remains a high-beta play where world-class resource density is offset by systemic logistical and political hurdles. The reality of Arctic mining involves higher-than-average OPEX due to extreme climate conditions and a complete absence of interconnected power grids. The 2026 outlook suggests a polarized future for investors. In a "Bull Case" scenario, massive sovereign de-risking—led by the U.S. and the EU’s Critical Minerals Act—could provide the low-interest debt required to build the ports and processing plants that currently stall project development.

Conversely, a "Bear Case" scenario involves a prolonged "frozen" regulatory environment if the friction between the Trump administration, Copenhagen, and the autonomous government in Nuuk intensifies.

As the world transitions toward a mineral-intensive economy, Greenland has ceased to be a peripheral concern; it is now a frontline where the future of resource security and Western industrial autonomy is fought.

Sources:

- https://www.iea.org/reports/global-critical-minerals-outlook-2025

- https://www.thearcticinstitute.org/dimensions-oil-gas-development-greenland/

- https://www.usgs.gov/centers/national-minerals-information-center/mineral-commodity-summaries

- https://www.atlanticcouncil.org/dispatches/trumps-quest-for-greenland-could-be-natos-darkest-hour/

- https://www.europarl.europa.eu/RegData/etudes/BRIE/2025/769527/EPRS_BRI(2025)769527_EN.pdf

- https://www.epc.eu/publication/its-a-bargain-the-case-of-greenland/

- https://govmin.gl/publications/greenland-mineral-resources-strategy-2025-2029/

- https://criticalmineralsinstitute.com/

- https://www.thearcticinstitute.org/dimensions-oil-gas-development-greenland/

- https://www.usgs.gov/centers/national-minerals-information-center/mineral-commodity-summaries

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. The content regarding geopolitical developments and resource markets contains forward-looking statements and scenarios that are subject to rapid change. Readers should conduct their own due diligence before making any investment decisions.

Explore More

View All

Silver’s Elevation to Critical Mineral Status: A Strategic Turning Point for U.S. Supply Chains

Silver’s Elevation to Critical Mineral Status: A Strategic Turning Point for U.S. Supply Chains

The U.S. Department of the Interior’s addition of silver to the Final 2025 List of Critical Minerals in November 2025 marks a pivotal shift. No longer viewed primarily as a precious metal for jewelry and investment, silver is now recognized as vital to technology, the energy transition, and national security.

The EU’s Race for Critical Raw Materials: Navigating Supply Risks

The EU’s Race for Critical Raw Materials: Navigating Supply Risks

As the European Union moves toward its goal of net-zero emissions by 2050, the demand for critical raw materials, the building blocks of wind turbines, batteries, and solar panels—is skyrocketing.