Precious Metals

January 21, 2026

3 min

Precious Metals

The third quarter of 2025 served as a definitive stress test for the silver sector. While the average realized silver price reached $40.81 per ounce, the narrative on the ground was one of complex operational discipline. Official company filings reveal a landscape where mid-tier miners are aggressively rewriting the supply table through massive M&A and expansions, while industry giants navigate the technical transitions of maturing mines.

1. The Consolidation Payoff

The most dramatic shifts in production this quarter were inorganic. Consolidation has moved from a corporate trend to the primary engine for supply growth.

- First Majestic’s Record Integration (3.9 Moz): First Majestic delivered its most productive quarter in company history. The 96% year-over-year surge in silver output was primarily driven by the full integration of the Cerro Los Gatos mine, which now serves as the high-grade anchor for the portfolio.

- Pan American Silver (5.5 Moz): Following its strategic moves, Pan American benefited from the full integration of the Juanicipio asset, which continues to drive volumes upward. This helps offset maturing production at other legacy sites and solidifies their position in the top tier.

2. The Ramp-Up Success Stories

Organic growth was led by massive projects in North America reaching critical steady-state.

- Coeur Mining (4.8 Moz): Coeur reported a 57% increase in silver production, marking a successful turning point at its Rochester mine in Nevada. After technical modifications to the crushing circuit earlier in the year, the operation achieved its targeted throughput levels just in time for the price rally.

- Hecla Mining (4.6 Moz): Hecla’s record-breaking financial results were supported by a strong quarter at Greens Creek and the ongoing ramp-up of Keno Hill, which delivered its second consecutive quarter of positive free cash flow.

3. Managing Operational Transitions

At the top of the table, the industry's giants are navigating a delicate balance between asset maturity and maintenance.

- Fresnillo Plc (11.7 Moz): As the global primary leader, Fresnillo’s output remained steady. The company managed the planned cessation of mining at the San Julián Disseminated Ore Body by optimizing throughput and grades at Saucito and Herradura.

- KGHM Polska Miedz (10.8 Moz): The Polish giant remains the bedrock of byproduct supply. Despite planned maintenance at the Głogów II smelter impacting refined output, silver recovery from copper concentrates remained high, illustrating the reliability of its large-scale assets.

- Buenaventura (4.0 Moz): The quarter saw silver production slightly exceed projections at Yumpag due to higher ore grades. The company has successfully implemented the Over-Drift-Fill (ODF) mining method, which provides high ore recovery with enhanced selectivity, reducing surface impact while maintaining steady volumes during mine transitions.

Summary: Growth Moves to the Mid-Tier

Q3 2025 demonstrated that while established giants provide a vital supply floor, the sector's growth is being driven by the mid-tier. Through aggressive consolidation and successful project ramp-ups, companies like First Majestic and Coeur Mining are effectively replacing ounces lost to the natural depletion of legacy assets.

Sources & References

This article is based on official Q3 2025 quarterly reports, production updates, and earnings releases from the respective companies, as published on their investor relations websites and filed with relevant regulatory bodies (e.g., SEDAR+, EDGAR, JSE, ASX, HKEX) in October and November 2025:

- Fresnillo Plc – Q3 2025 Production Report

- KGHM Polska Miedz SA – Results Highlights for the Third Quarter of 2025

- Newmont Corporation – Q3 2025 Results and 2025 Guidance Update

- Southern Copper Corp – Third Quarter 2024 Earnings Release

- Glencore PLC – Third Quarter 2025 Production Report

- Pan American Silver Corp – Q3 2025 Unaudited Results

- Coeur Mining Inc – Third Quarter 2025 Results

- Hecla Mining Co – Third Quarter 2025 Results

- Buenaventura (SAA) – Third Quarter and Nine-month 2025 Results

- First Majestic Silver Corp – Financial Results for Q3 2025 and Operational Highlights

- Additional supporting data drawn from company presentations, webcasts, and press releases issued during the October–November 2025 reporting season.

Disclaimer: The information presented in this article is for informational purposes only and is based on publicly available company reports and disclosures as of December 2025. Production figures represent attributable gold ounces unless otherwise stated. Minor differences in reported numbers may arise from rounding, final audit adjustments, or differences between preliminary and final reports.

Explore More

View All

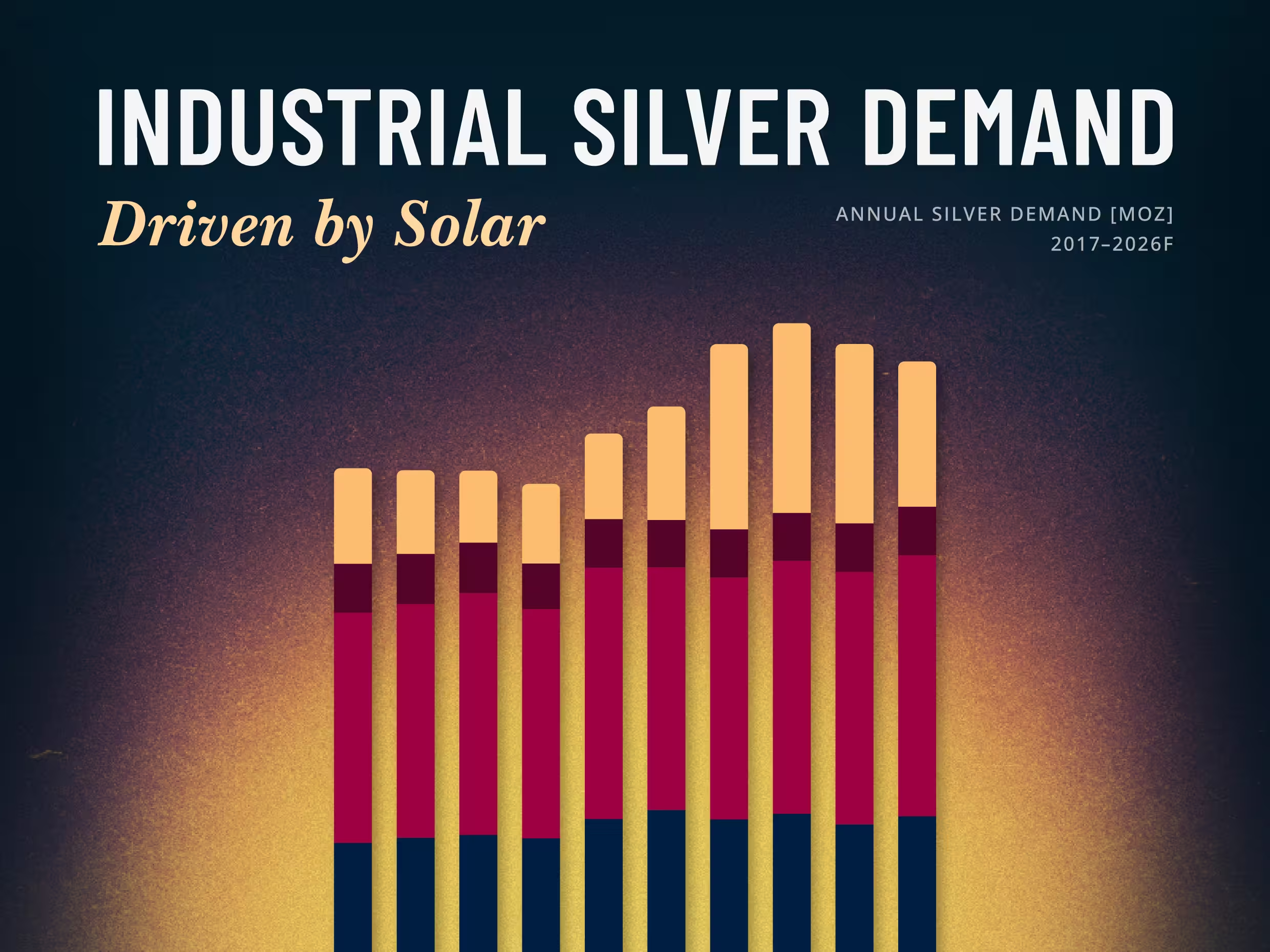

Solar Is Silver's Largest Industrial Market, and Not Easily Replaced

Solar Is Silver's Largest Industrial Market, and Not Easily Replaced

When LONGi Green Energy, the world's largest solar module maker, told investors on January 5, 2026 that it would begin mass-producing base-metal solar cells in the second quarter, it put a number on a pressure the whole industry feels. Solar is the largest single application within silver's industrial demand, and as the metal ran to a record above $121 an ounce in January, rising silver costs pushed manufacturers to accelerate efforts to reduce the metal per cell.

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

In early 2026, the artificial intelligence narrative shifted abruptly from software capabilities to physical hardware constraints. With tech giants committing hundreds of billions to new infrastructure—pushing global hyperscaler capital expenditures past $600 billion this year—the industry has collided with a new primary bottleneck: a severe power and thermal crunch.

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Somewhere inside a pressurized-water reactor, an alloy that is four-fifths silver is absorbing neutrons to keep the core in check, a job most silver investors have never heard of. It is a useful reminder that the metal people picture as coins and jewelry mostly works elsewhere, across industry.

Ranked: The Countries That Produced the Most Silver in 2025

Ranked: The Countries That Produced the Most Silver in 2025

Mexico remained the world's top silver-producing country in 2025, mining 172.9 million ounces (Moz), roughly a fifth of global supply, according to the World Silver Survey 2026, produced for the Silver Institute by Metals Focus. But Mexico's lead narrowed: its output fell 5% for a third straight year, while second-place Peru climbed 7%. Global mine production rose 3% to 846.6 Moz, even as the ranking's top tier told a story of one leader sliding and its closest rival closing in.