Precious Metals

October 27, 2025

3 min

Precious Metals

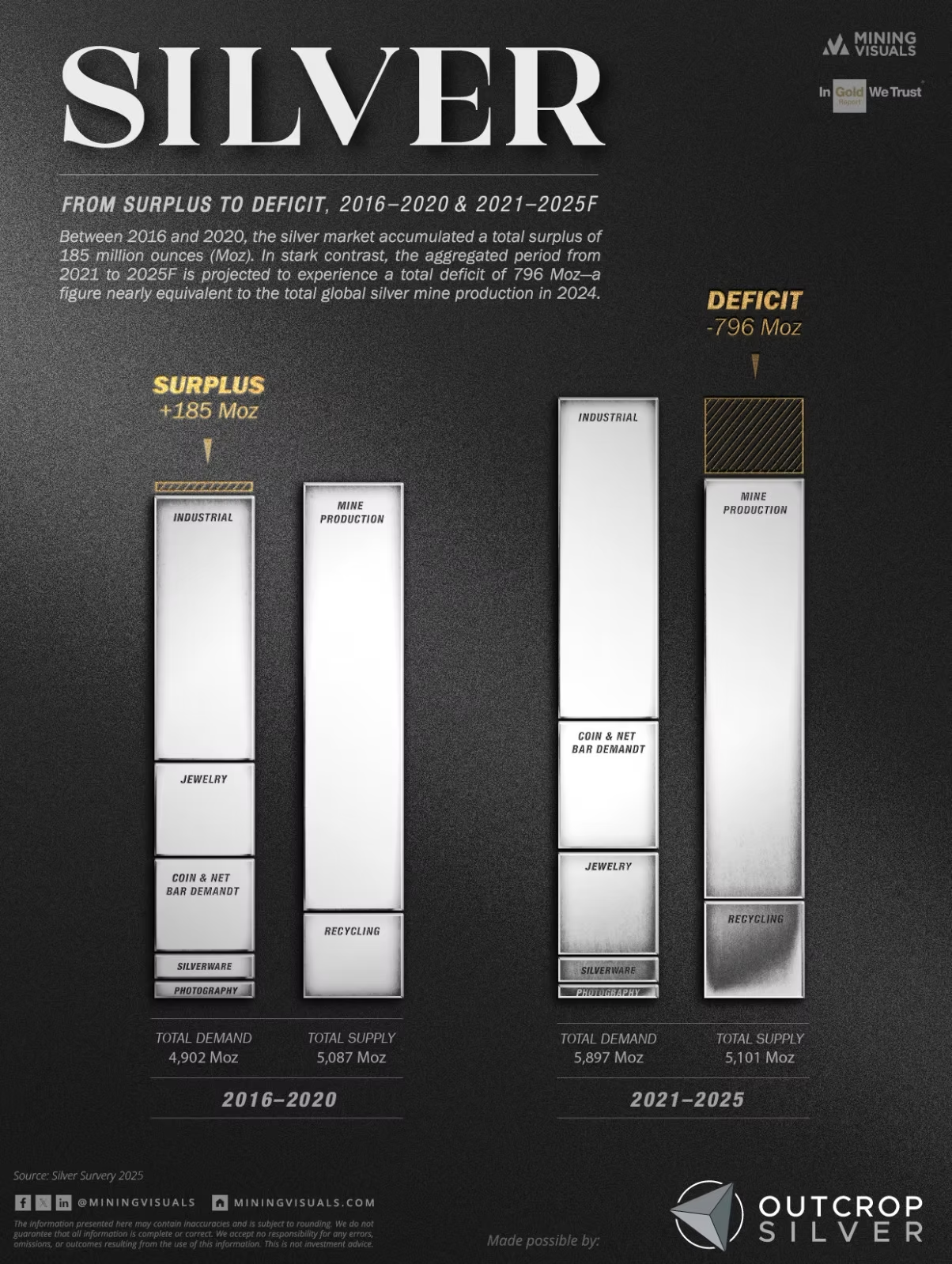

Silver's industrial utility is finally colliding with its physical scarcity. While silver prices have recently surged, hitting a new all-time high, that excitement is merely a reflection of a fundamental market shift. This analysis, based on data from the World Silver Survey 2025 (The Silver Institute), examines how the global silver market has fundamentally inverted, moving from a period of comfortable surplus to one defined by chronic structural deficits.

During 2016–2020, the silver market was generally well-supplied, exhibiting a cumulative market surplus. This period was characterized by total supply exceeding total demand, ensuring readily available metal. Demand was diversified, with industrial applications forming the largest component, supported by steady jewelry and investment purchases.

The current period (2021–2025F) is marking a complete reversal, with an anticipated cumulative market deficit of -796 million ounces (Moz). This imbalance results from a deep structural divergence, where accelerating industrial demand is running up against an inelastic supply base.

The Demand Imperative: Technology & Electrification

The primary driver of the structural shift is a surge in industrial consumption, which now accounts for approximately 60% of total global usage. This is focused on applications where silver is essential due to its unmatched electrical and thermal properties:

- Green Energy: Demand from Photovoltaics (PV) is the fastest-growing industrial segment. Silver is a mandatory input for every solar cell, where it is applied as a conductive paste to the front and back surfaces to form thin wires (or busbars) that capture and channel the electricity generated by the silicon wafers.

- Mobility & Data: Strong consumption is also noted from the automotive sector, where Electric Vehicles (EVs) require significantly more silver per unit than conventional cars, alongside growing demand from 5G network construction and data center build-out (Source: CME Group).

The Supply Constraint: An Inelastic Response

While demand accelerates, total supply—from both mine production and recycling—is expected to remain largely flat. This is due to two key structural challenges:

- Byproduct Dependency: Approximately 70% to 75% of mined silver is a byproduct of mining other metals, such as copper, lead, and zinc (Source: Investec, 2025). Consequently, higher silver prices alone cannot trigger a rapid increase in supply, as production is dictated by the economics and capital cycles of these primary base metals.

- Declining Ore Grades: Primary silver miners face the challenge of declining average ore grades at mature mines, requiring greater capital and effort to maintain existing production levels (Source: Discovery Alert).

Market Implication

This persistent supply shortfall—equivalent to nearly an entire year of global mine output—is forcing the market to address the deficit by drawing from above-ground physical inventories held in exchange and dealer warehouses.

Sponsored by:

Outcrop Silver is a leading explorer and developer focused on advancing its flagship Santa Ana high-grade silver project in Colombia. Leveraging a disciplined and seasoned team of professionals with decades of experience in the region. Outcrop Silver is dedicated to expanding current mineral resources through strategic exploration initiatives.

At the core of our operations is a commitment to responsible mining practices and community engagement, underscoring our approach to sustainable development. Our expertise in navigating complex geological and market conditions enables us to consistently identify and capitalize on opportunities to enhance shareholder value.

With a deep understanding of the Colombian mining landscape and a track record of successful exploration, Outcrop Silver is poised to transform the Santa Ana project into a significant silver producer, contributing positively to the local economy and setting new standards in the mining industry.

Learn more about Outcrop Silver at https://outcropsilver.com/

Source Disclaimer

The data presented in this article and the accompanying infographic is sourced from the "World Silver Survey 2025," published by the Silver Institute. This report is a comprehensive analysis of the global silver market. For a full breakdown, methodology, and detailed analysis, please refer to the complete report, available at: https://silverinstitute.org/wp-content/uploads/2025/04/World_Silver_Survey-2025.pdf

Explore More

View All

Ghana's Gold Mining Landscape: A Story Written in Ancient Rock

Ghana's Gold Mining Landscape: A Story Written in Ancient Rock

Ghana is one of the world's most significant gold-producing countries, and in 2025 it remained the largest in Africa, with national output reaching about 6 million ounces. But the numbers are only the surface. Ghana's gold reaches back more than two billion years into the rock beneath it, shaped by ancient mountain-building forces and worked by human hands for well over a century.

Solar Is Silver's Largest Industrial Market, and Not Easily Replaced

Solar Is Silver's Largest Industrial Market, and Not Easily Replaced

When LONGi Green Energy, the world's largest solar module maker, told investors on January 5, 2026 that it would begin mass-producing base-metal solar cells in the second quarter, it put a number on a pressure the whole industry feels. Solar is the largest single application within silver's industrial demand, and as the metal ran to a record above $121 an ounce in January, rising silver costs pushed manufacturers to accelerate efforts to reduce the metal per cell.

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

In early 2026, the artificial intelligence narrative shifted abruptly from software capabilities to physical hardware constraints. With tech giants committing hundreds of billions to new infrastructure—pushing global hyperscaler capital expenditures past $600 billion this year—the industry has collided with a new primary bottleneck: a severe power and thermal crunch.

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Somewhere inside a pressurized-water reactor, an alloy that is four-fifths silver is absorbing neutrons to keep the core in check, a job most silver investors have never heard of. It is a useful reminder that the metal people picture as coins and jewelry mostly works elsewhere, across industry.