Copper

January 8, 2026

3 min

Copper

Copper’s Complex Quarter: Resilience Amid Disruption (Q3 2025)

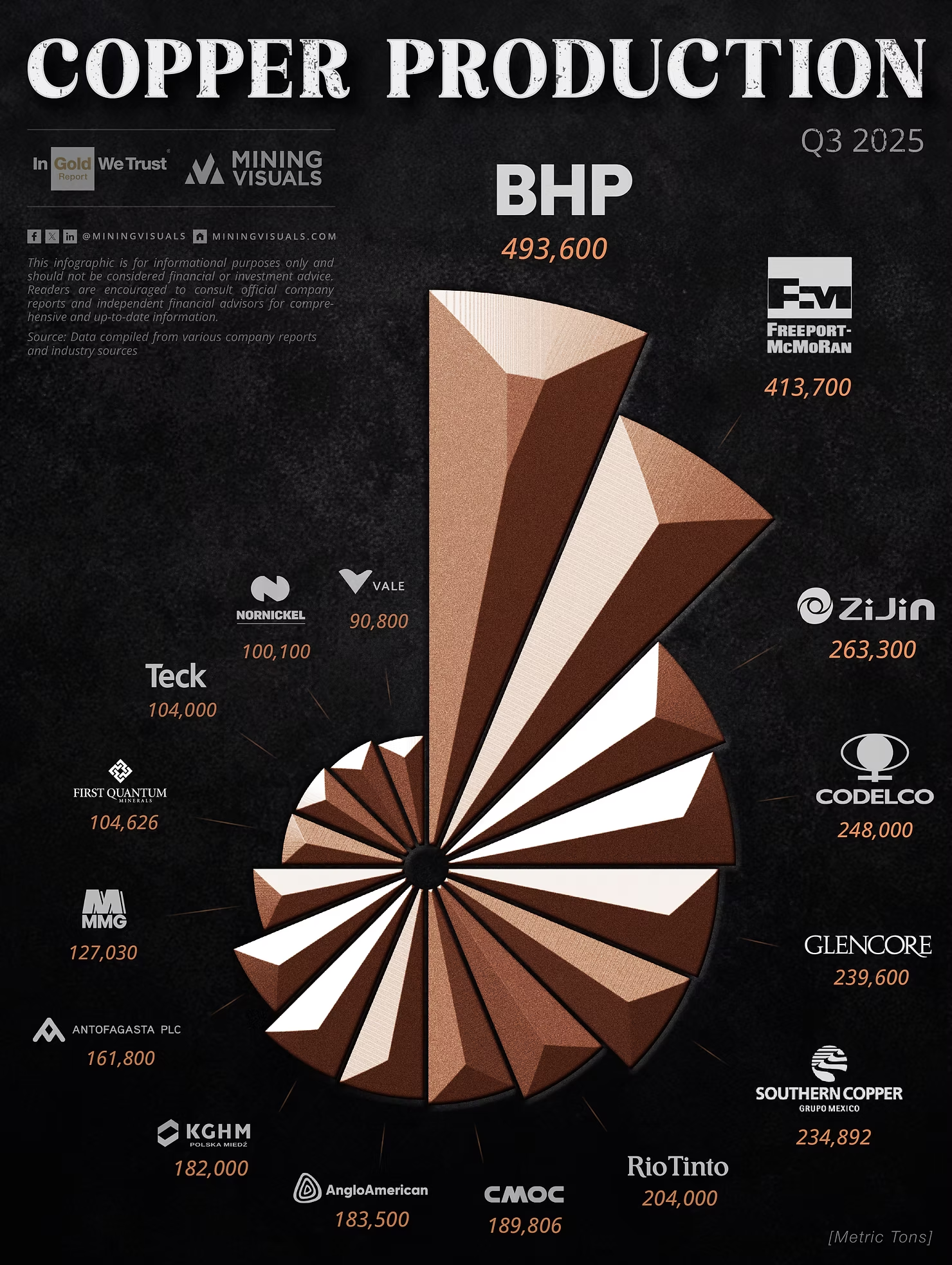

Q3 2025 proved challenging for the global copper industry. Strong demand from electrification and infrastructure met sharp supply-side disruptions. Output from the top 20 miners hit ~3.46 million tonnes, down ~4% quarter-over-quarter, per SMM data.

Operational Setbacks Hit Giants

Freeport-McMoRan suffered a major blow at its Grasberg mine in Indonesia. On September 8, a massive mud rush flooded underground levels with ~800,000 tonnes of material, tragically killing seven workers and halting operations [Reuters, Freeport Update]. Q3 production reached 912 million pounds (~413,700 tonnes), with higher copper and gold prices cushioning financial impacts.

In Chile, Codelco dealt with tragedy too. A July 31 seismic event triggered a rockburst at El Teniente, claiming six lives and forcing a safety-driven shutdown [Reuters, Mining Technology]. Output fell sharply, though year-to-date volumes rose modestly via ramp-ups at Ministro Hales and Rajo Inca.

Bright Spots: Glencore and Zijin Shine

Glencore delivered a strong rebound, with own-sourced copper up 36% QoQ to higher grades at African assets like KCC in the DRC [Glencore Q3 Report]. It strategically prioritized copper amid cobalt export quotas.

Zijin Mining solidified its rise, posting ~830,000 tonnes in nine-month output (up 5% YoY) [Zijin Report]. Phase II at Julong in Tibet nears year-end commissioning, boosting future capacity.

Steady Progress and Outlook

Rio Tinto advanced mined copper YoY via the Oyu Tolgoi underground ramp-up in Mongolia, on track for >50% annual growth [Rio Tinto Q3 Results].

Disruptions from Grasberg and El Teniente flipped 2025 forecasts from surplus to deficit (estimates 55,500–400,000 tonnes) [Goldman Sachs, Benchmark]. As safety and environmental standards tighten, brownfield expansions will shape the energy transition ahead.

Stay tuned. We will be sharing our Q4 update in the coming months.

Sources for Q3 2025 Copper Production Table

Production figures are cross-verified from official company reports (as of December 30, 2025):

- BHP: Operational Review

- Freeport-McMoRan: Q3 2025 Results

- Zijin Mining: Q3 Report

- Codelco: 9M 2025 Results

- Glencore: Q3 Production Report

- Southern Copper: Q3 Earnings

- Rio Tinto: Q3 Production Results

- Anglo American: Q3 Production Report

- KGHM: Q3 Report

- Antofagasta: Q3 Production Report

- MMG: Q3 Production Report

- First Quantum: Q3 Results

- Teck Resources: Q3 Results

- Nornickel: 9M Production Results

- Vale: Q3 Production Report

- Lundin Mining: Q3 Results

- Ivanhoe Mines: Q3 Production Update

Disclaimer

The information in this article is provided for informational purposes only and does not constitute investment advice, financial recommendation, or an offer to buy or sell securities. Copper production data and market commentary are based on publicly available information from the companies and third-party sources believed to be reliable, but no representation or warranty is made as to the accuracy, completeness, or timeliness of the data.

Forward-looking statements regarding future production, prices, costs, project developments, or market conditions involve known and unknown risks and uncertainties, including but not limited to operational disruptions, geopolitical events, regulatory changes, commodity price volatility, and weather-related impacts. Actual results may differ materially from those expressed or implied in this article.

Explore More

View All

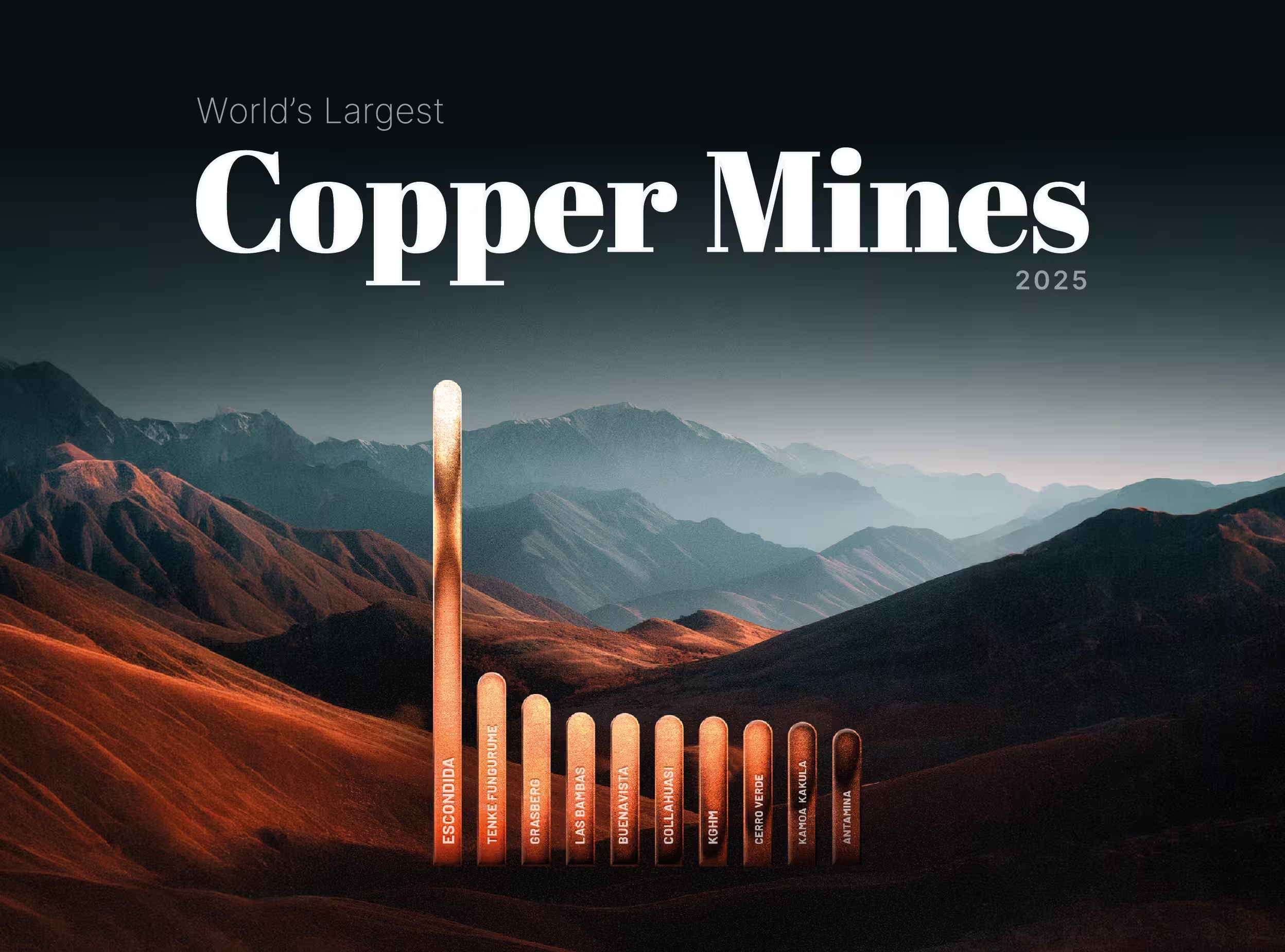

Ranked: The World's Largest Copper Mines (2025)

Ranked: The World's Largest Copper Mines (2025)

Copper has spent 2026 setting records, touching an intraday COMEX high of $6.71 per pound on May 13 amid AI-driven demand and supply shocks, against a backdrop where the ICSG now forecasts a 150,000-tonne deficit for 2026. In a market this tight, where the deficit thesis turns on lost tonnes, the question of where the world's copper actually comes from carries unusual weight.

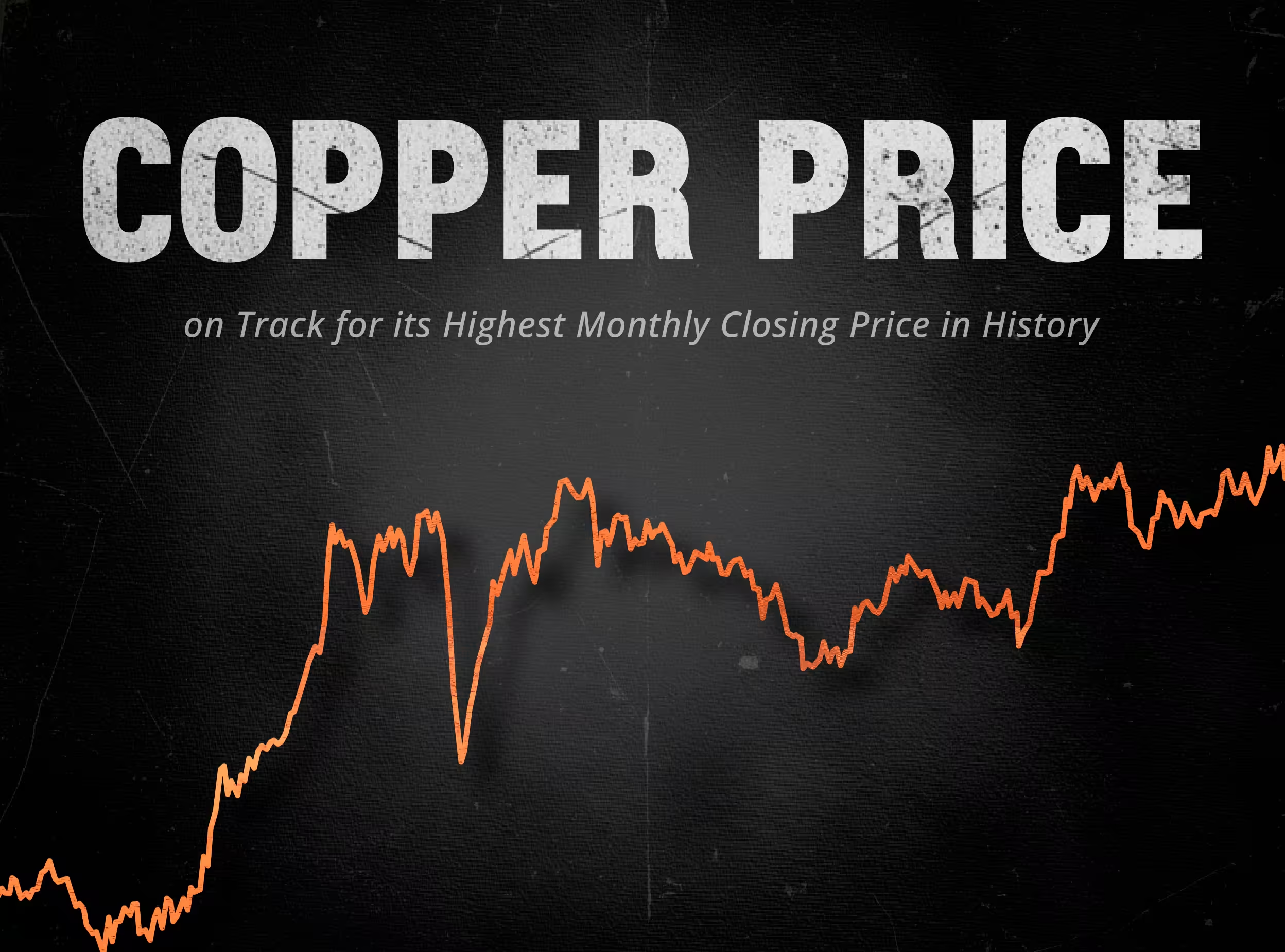

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper has spent most of 2026 doing something it had not done in a quarter century: setting fresh records every few weeks. The COMEX contract printed an intraday all-time high of $6.71 per pound on May 13, and the May monthly close looks set to land at the top of the historical chart. In London, copper traded above $14,000 per tonne in mid-May, touching $14,196.50, within reach of the LME's January 29 record of $14,527.50.

The Cost of Mining Copper: A 2024–2025 Update

The Cost of Mining Copper: A 2024–2025 Update

Copper futures touched an all-time high above $6.58 per pound on May 12, 2026, capping a 40.86% gain over the prior twelve months as supply tightness collided with structural demand from grid build-out, electric vehicles, and AI data centers. Earlier in the year, the LME benchmark rallied 22% to a record $13,387 per tonne on January 6, 2026. Behind the price action lies a less-discussed story: what it actually costs the world's largest miners to pull a pound of copper out of the ground.

Copper Production Q4 2025

Copper Production Q4 2025

As power-hungry AI data centers drive a projected 2-million-ton surge in global copper demand by 2030, market attention remains fixated on the supply side. Fourth-quarter 2025 metrics provide a definitive look at how the world's top miners closed out the year. While overall volumes remain heavily concentrated among a few historic industry giants, the true Q4 narratives emerged further down the list, as mid-tier producers leveraged flagship asset expansions to hit multi-year highs and offset the sector's ongoing struggle with declining ore grades.