Copper

November 26, 2025

2 min

Copper

If you are tracking the commodities market, the latest note from UBS—the world’s largest global wealth manager—signals a "perfect storm" for copper, as reported by Reuters. This forecast carries significant weight; when UBS shifts its "House View," it often signals where institutional capital will flow next.

The bank has aggressively raised its price forecasts, citing a collision between tightening global supply and fueled demand from the green energy transition.

📈 The Trajectory: Reaching New Highs

UBS’s updated projections paint a bullish picture for the next year. The bank has raised its March 2026 forecast by $750 to $11,500 per metric ton, and pushed its targets for June and September 2026 up by $1,000 each.

Most notably, UBS introduced a new target for December 2026, predicting prices will climb significantly:

New Target: UBS predicts copper prices will hit $13,000 per ton by December 2026.

As illustrated in the forecast above, this upward momentum is fueled by long-term demand from electrification. UBS expects global copper demand to grow by 2.8% annually through 2026, driven by:

- Electric Vehicles (EVs)

- Power-grid investments

- The booming data center sector

📉 The Widening Deficit: Where is the Supply?

While demand creates the pull, the supply side is providing the push. UBS warns that the gap between how much copper the world needs and how much is available is widening significantly.

The bank has drastically increased its market deficit forecasts. Falling inventories and persistent supply risks are expected to keep market conditions extremely tight.

What is driving this scarcity? UBS points to "persistent mine disruptions" as a key factor. Specific challenges cited include:

- Indonesia: Production halts at Freeport-McMoRan’s Grasberg mine following a fatal incident.

- Chile: A slower-than-expected output recovery.

- Peru: Recurring protests affecting operations.

Consequently, UBS has trimmed its refined copper production growth estimates to just 1.2% for 2025.

Explore More

View All

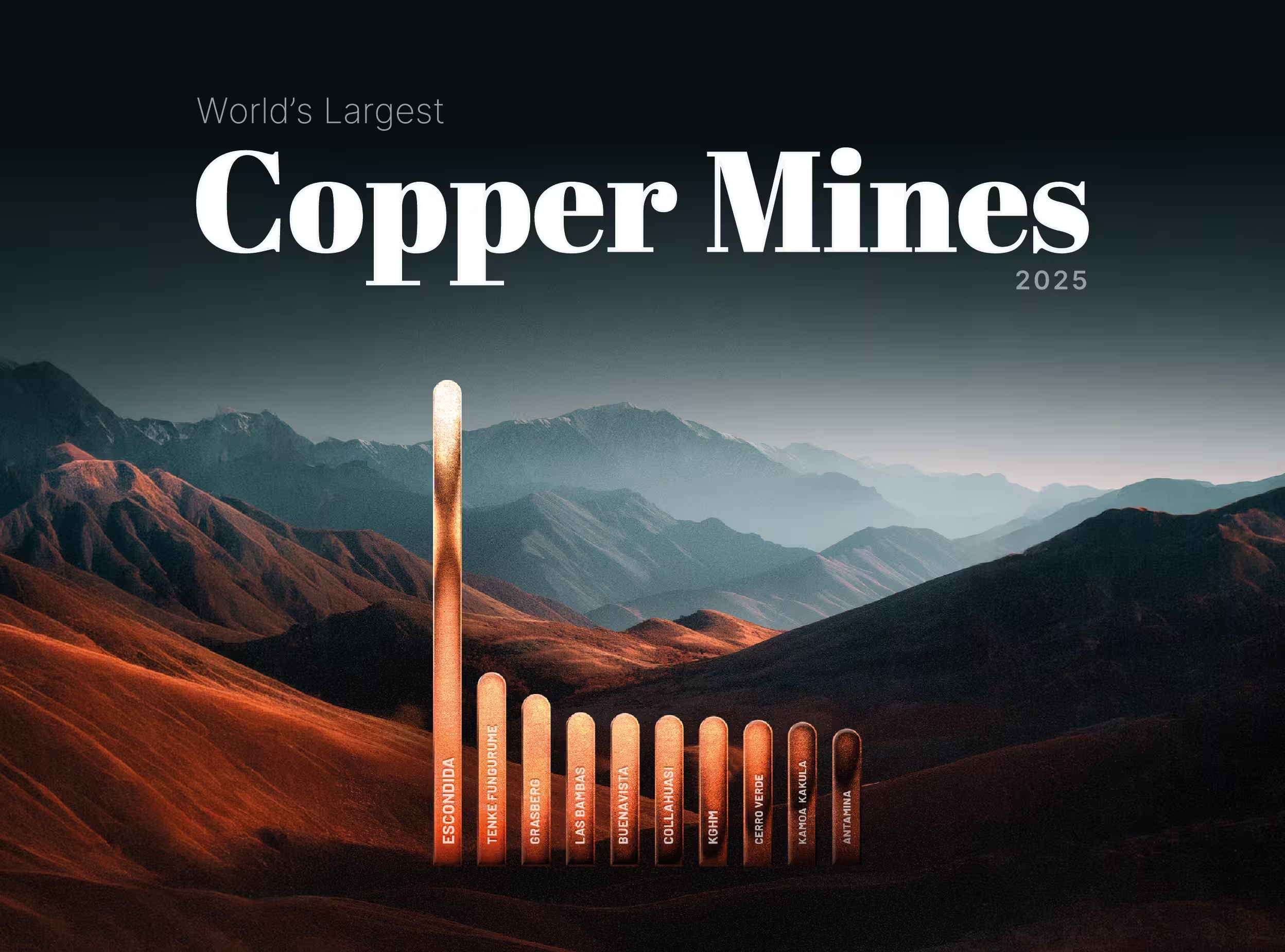

Ranked: The World's Largest Copper Mines (2025)

Ranked: The World's Largest Copper Mines (2025)

Copper has spent 2026 setting records, touching an intraday COMEX high of $6.71 per pound on May 13 amid AI-driven demand and supply shocks, against a backdrop where the ICSG now forecasts a 150,000-tonne deficit for 2026. In a market this tight, where the deficit thesis turns on lost tonnes, the question of where the world's copper actually comes from carries unusual weight.

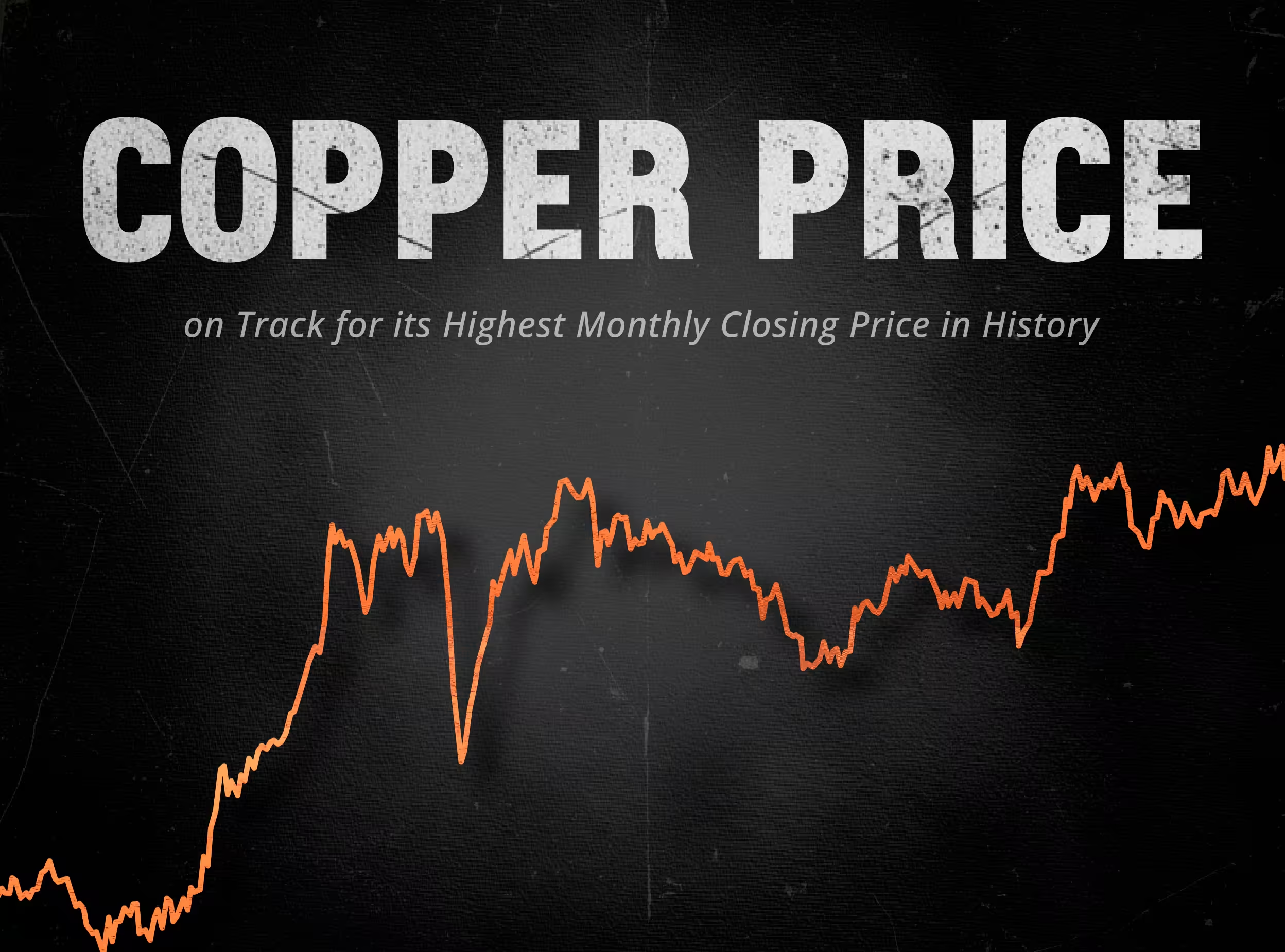

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper has spent most of 2026 doing something it had not done in a quarter century: setting fresh records every few weeks. The COMEX contract printed an intraday all-time high of $6.71 per pound on May 13, and the May monthly close looks set to land at the top of the historical chart. In London, copper traded above $14,000 per tonne in mid-May, touching $14,196.50, within reach of the LME's January 29 record of $14,527.50.

The Cost of Mining Copper: A 2024–2025 Update

The Cost of Mining Copper: A 2024–2025 Update

Copper futures touched an all-time high above $6.58 per pound on May 12, 2026, capping a 40.86% gain over the prior twelve months as supply tightness collided with structural demand from grid build-out, electric vehicles, and AI data centers. Earlier in the year, the LME benchmark rallied 22% to a record $13,387 per tonne on January 6, 2026. Behind the price action lies a less-discussed story: what it actually costs the world's largest miners to pull a pound of copper out of the ground.

Copper Production Q4 2025

Copper Production Q4 2025

As power-hungry AI data centers drive a projected 2-million-ton surge in global copper demand by 2030, market attention remains fixated on the supply side. Fourth-quarter 2025 metrics provide a definitive look at how the world's top miners closed out the year. While overall volumes remain heavily concentrated among a few historic industry giants, the true Q4 narratives emerged further down the list, as mid-tier producers leveraged flagship asset expansions to hit multi-year highs and offset the sector's ongoing struggle with declining ore grades.