Copper

November 5, 2025

2 min

Copper

Copper is an essential metal for modern civilization. While often working behind the scenes, it is a fundamental component in everything from household wiring to advanced electronics. An analysis of its production over the last century reveals a compelling story. As the global population has grown, so has the demand for copper.

More recently, however, its production trajectory has accelerated, reflecting a growing global need for connectivity, advanced technology, and new forms of energy. As the book "RED METAL, BLUE PLANET" illustrates, key moments in recent history have highlighted this growing demand.

The Industrial Baseline: A Parallel Growth

For much of the 20th century, copper's story was closely linked with basic industrial development. As global populations expanded and societies built out their infrastructure, the demand for copper increased at a similar, steady pace. This period showed a parallel growth between population and copper use. Homes needed wiring and pipes, cars required electrical systems, and factories used copper components.

The Digital Accelerator: More Copper Per Person

A notable shift began in the mid-1960s, and then accelerated in the mid-1990s. The "Digital Revolution," with the widespread adoption of personal computers, the internet, and early mobile phones, created new and significant demands for copper.

This wasn't just about more people; it was about more copper per person. Each new electronic device and the data infrastructure to support it added to the global copper requirement. This trend was amplified by the "Rise of a New Consumer" in 1999. China's rapid industrialization and urbanization, in particular, drove substantial new demand for construction materials, electronics, and infrastructure, creating a strong "super-cycle" for copper that pushed production levels higher.

Supply Challenges

Unlike in the past—such as the 1990s “supply flood” from Chile—today’s supply growth faces tougher conditions. New high-grade deposits are harder to find, ore grades are declining, and mine development takes longer due to regulatory hurdles.

This growing imbalance highlights the need for greater efficiency, recycling, and continued investment in mining innovation.

Source: Data source: USGS - Mineral Commodity Summaries (2024); USGS - Historical Statistics for Mineral and Material Commodities (2023)

Explore More

View All

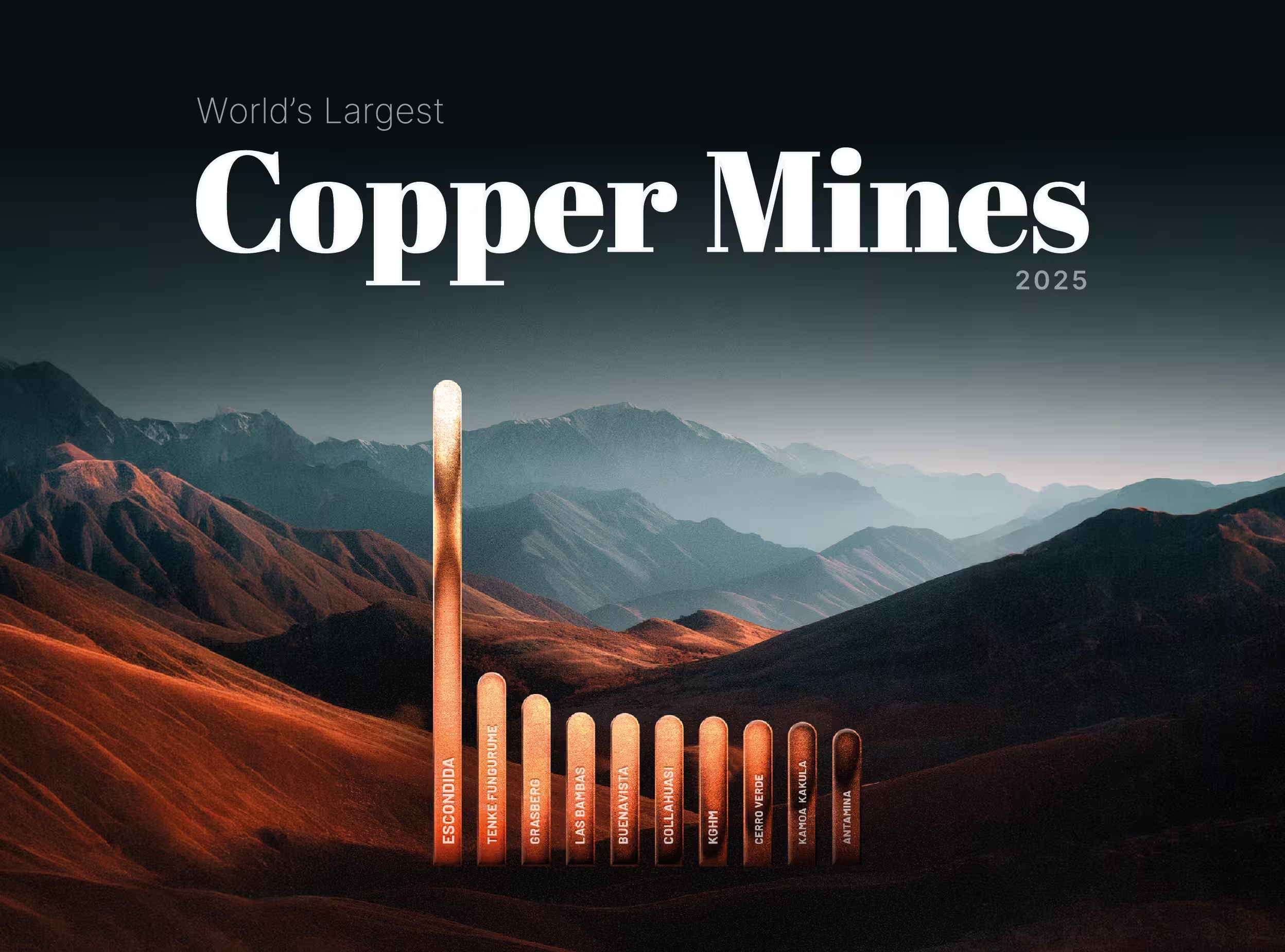

Ranked: The World's Largest Copper Mines (2025)

Ranked: The World's Largest Copper Mines (2025)

Copper has spent 2026 setting records, touching an intraday COMEX high of $6.71 per pound on May 13 amid AI-driven demand and supply shocks, against a backdrop where the ICSG now forecasts a 150,000-tonne deficit for 2026. In a market this tight, where the deficit thesis turns on lost tonnes, the question of where the world's copper actually comes from carries unusual weight.

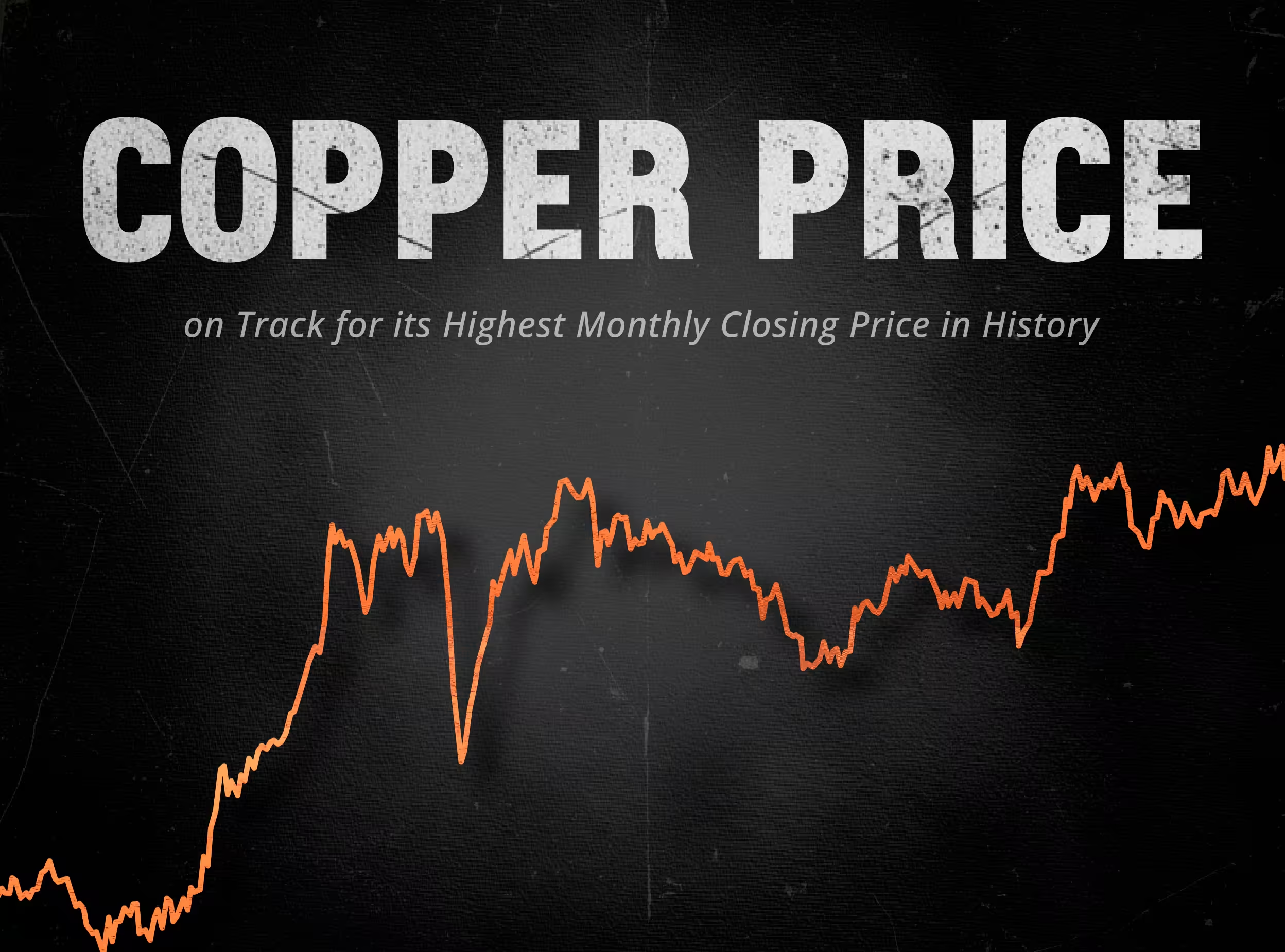

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper has spent most of 2026 doing something it had not done in a quarter century: setting fresh records every few weeks. The COMEX contract printed an intraday all-time high of $6.71 per pound on May 13, and the May monthly close looks set to land at the top of the historical chart. In London, copper traded above $14,000 per tonne in mid-May, touching $14,196.50, within reach of the LME's January 29 record of $14,527.50.

The Cost of Mining Copper: A 2024–2025 Update

The Cost of Mining Copper: A 2024–2025 Update

Copper futures touched an all-time high above $6.58 per pound on May 12, 2026, capping a 40.86% gain over the prior twelve months as supply tightness collided with structural demand from grid build-out, electric vehicles, and AI data centers. Earlier in the year, the LME benchmark rallied 22% to a record $13,387 per tonne on January 6, 2026. Behind the price action lies a less-discussed story: what it actually costs the world's largest miners to pull a pound of copper out of the ground.

Copper Production Q4 2025

Copper Production Q4 2025

As power-hungry AI data centers drive a projected 2-million-ton surge in global copper demand by 2030, market attention remains fixated on the supply side. Fourth-quarter 2025 metrics provide a definitive look at how the world's top miners closed out the year. While overall volumes remain heavily concentrated among a few historic industry giants, the true Q4 narratives emerged further down the list, as mid-tier producers leveraged flagship asset expansions to hit multi-year highs and offset the sector's ongoing struggle with declining ore grades.