Copper

September 16, 2025

3 min

Copper

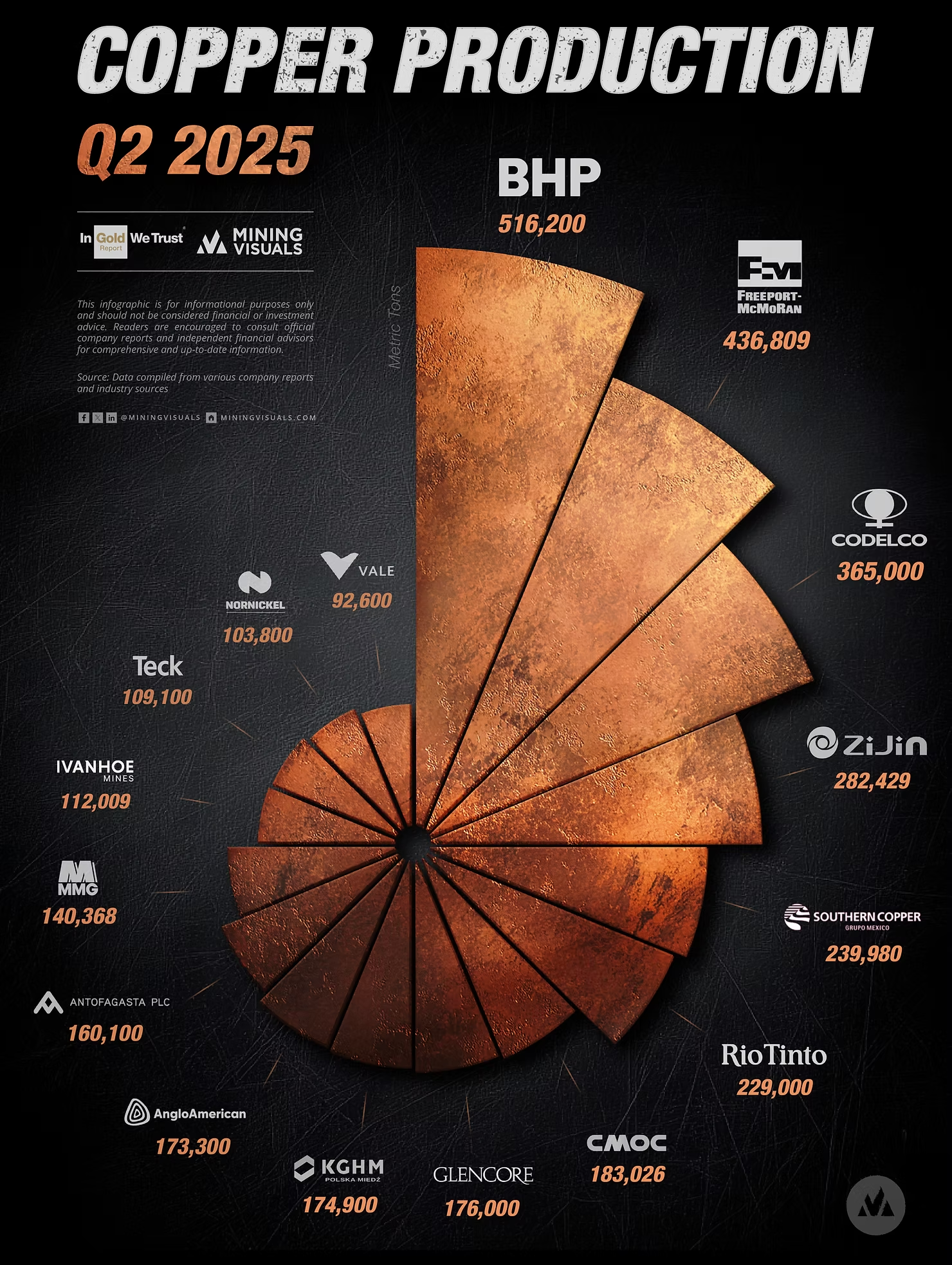

Global copper production data for Q2 2025 is in, offering fresh insight into how the world’s largest miners are performing. This quarter’s rankings of the top 16 producers reveal a mix of recovery, resilience, and growth across the industry.

Chile’s state-owned Codelco posted a strong rebound, while other major producers continued to grapple with operational challenges. At the same time, companies ramping up new projects delivered impressive gains, reshaping the competitive landscape.

In this article, we break down the output of the top producers and explore the key year-over-year trends shaping global copper supply.

Top 3 Producers: A Story of Stability, Headwinds, and Recovery

- BHP Group solidified its position as the world's top copper producer, with an output of 516,200 tonnes in Q2, a 2.24% increase year-over-year. According to the company's operational report, this growth was fueled by record-breaking performances across its portfolio. Key drivers included the Escondida mine achieving its highest production in 17 years due to record concentrator throughput and higher grades. Additionally, the Spence mine in Chile and the Copper South Australia operations both delivered record quarterly production. These results underscore the success of BHP's strategy to expand its copper portfolio, particularly through the integration of the acquired OZ Minerals assets.

- Freeport-McMoRan held the second spot with 436,809 tonnes, though production was down -7.14% compared to Q2 2024. The decline was primarily due to lower ore grades at Indonesia's Grasberg mine, driven by a recalibrated draw point flow model, and increased in-process inventory from a new copper smelter, causing timing mismatches. South America's Cerro Verde also faced lower ore grades. Despite this, higher copper prices ($4.42/lb) and cost efficiencies supported earnings.

- Codelco secured third place with a powerful performance, producing 365,000 tonnes. The Chilean state-owned miner posted a remarkable 18.12% year-over-year increase, signaling a significant turnaround. This strong result was driven by the successful ramp-up of its "structural projects," including the Chuquicamata Underground Mine, and a recovery in throughput at its El Teniente division after overcoming previous operational difficulties.

Standout Growth: Ramp-Ups and Turnarounds Fueling Gains

Several other producers delivered impressive double-digit growth in the second quarter.

- MMG once again led the pack with a massive 54.30% surge in copper cathode plus copper in copper concentrate, reaching 140,368 tonnes. This growth is primarily attributed to its Khoemacau mine in Botswana operating at near full capacity for the entire quarter. This was supported by stable operations and ore throughput at the Las Bambas mine in Peru.

- Vale reported a robust 17.81% increase, producing 92,600 tonnes, the best Q2 since 2019. Key drivers: higher grades at Sossego (0.98% to 1.21%), Salobo at nominal capacity, and Voisey's Bay expansion ramp-up.

- Rio Tinto also delivered strong growth of 15.00%, totaling 229,000 tonnes. The increase was underpinned by the continued, successful ramp-up of the high-grade underground mine at Oyu Tolgoi in Mongolia, complemented by higher grades and improved recoveries at its Kennecott operation in the USA.

Major Declines: Miners Navigating Operational Challenges

Some of the industry's biggest names continued to navigate headwinds, leading to year-over-year production declines.

- Glencore saw the largest drop among major producers at -21.04%. The decrease was primarily due to planned lower grades at the Collahuasi mine in Chile and maintenance at the Antamina operation in Peru, compounded by ongoing operational challenges at its African copper assets.

- Anglo American's production fell by -11.58%. This was mainly due to the PGM demerger (Q2 2025 covers only April-May) and lower grades at Collahuasi. Quellaveco and Los Bronces showed gains, up 4.7% and strong performance QoQ.

Source: Data compiled from various company reports and industry sources

This content is for informational purposes only and should not be considered financial or investment advice. Readers are encouraged to consult official company reports and independent financial advisors for comprehensive and up-to-date information.

Explore More

View All

Ranked: The World's Largest Copper Mines (2025)

Ranked: The World's Largest Copper Mines (2025)

Copper has spent 2026 setting records, touching an intraday COMEX high of $6.71 per pound on May 13 amid AI-driven demand and supply shocks, against a backdrop where the ICSG now forecasts a 150,000-tonne deficit for 2026. In a market this tight, where the deficit thesis turns on lost tonnes, the question of where the world's copper actually comes from carries unusual weight.

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper on Track for Its Highest Monthly Close on Record: A Look at the Drivers

Copper has spent most of 2026 doing something it had not done in a quarter century: setting fresh records every few weeks. The COMEX contract printed an intraday all-time high of $6.71 per pound on May 13, and the May monthly close looks set to land at the top of the historical chart. In London, copper traded above $14,000 per tonne in mid-May, touching $14,196.50, within reach of the LME's January 29 record of $14,527.50.

The Cost of Mining Copper: A 2024–2025 Update

The Cost of Mining Copper: A 2024–2025 Update

Copper futures touched an all-time high above $6.58 per pound on May 12, 2026, capping a 40.86% gain over the prior twelve months as supply tightness collided with structural demand from grid build-out, electric vehicles, and AI data centers. Earlier in the year, the LME benchmark rallied 22% to a record $13,387 per tonne on January 6, 2026. Behind the price action lies a less-discussed story: what it actually costs the world's largest miners to pull a pound of copper out of the ground.

Copper Production Q4 2025

Copper Production Q4 2025

As power-hungry AI data centers drive a projected 2-million-ton surge in global copper demand by 2030, market attention remains fixated on the supply side. Fourth-quarter 2025 metrics provide a definitive look at how the world's top miners closed out the year. While overall volumes remain heavily concentrated among a few historic industry giants, the true Q4 narratives emerged further down the list, as mid-tier producers leveraged flagship asset expansions to hit multi-year highs and offset the sector's ongoing struggle with declining ore grades.