Precious Metals

April 23, 2026

1 min

Precious Metals

Key takeaways

- Merger Momentum: First Majestic’s 84% production surge was the year's single largest volume jump, driven by the Gatos Silver acquisition.

- Expansion Payoffs: Coeur Mining and Hecla Mining reached critical milestones at Rochester and Lucky Friday, establishing new operational baselines.

- Yield Efficiency: Despite grade challenges, Fresnillo maintained its lead, while Newmont leveraged record free cash flow to optimize its byproduct output.

The silver market opened 2026 with historic volatility, peaking at a record $121.64/oz in January before undergoing a sharp 38% correction by the end of March. While prices shifted, the operational reports for the 2025 calendar year reveal a sector defined by massive infrastructure completions and aggressive M&A. With the 2025 audited figures now finalized, the data shows that production growth was not uniform, but concentrated in companies that successfully executed major expansion projects.

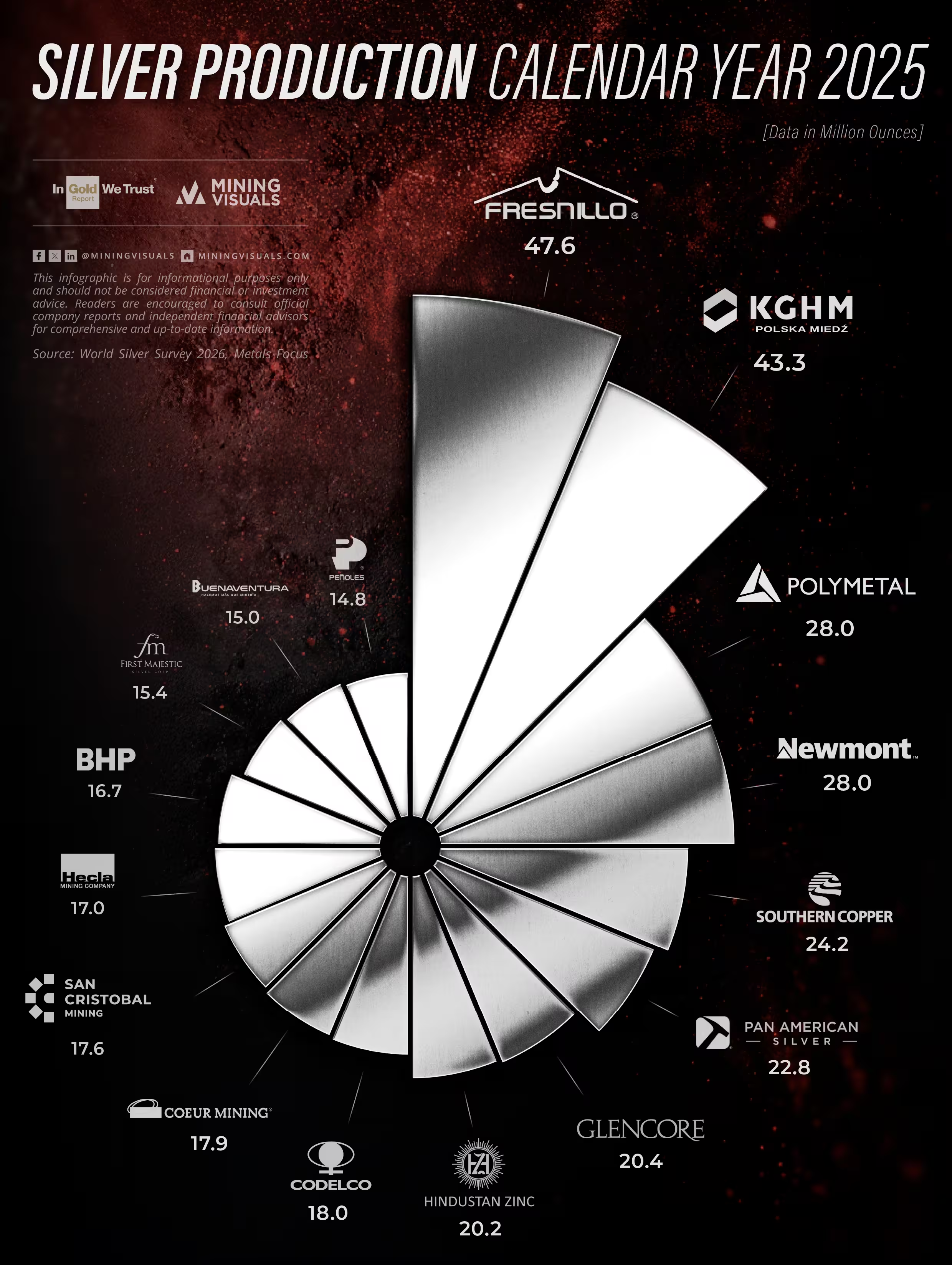

The Expansion Leaders: Coeur and Hecla

2025 marked a transformative year for U.S.-based output. Coeur Mining reported 17,900,000 ounces for the year, a 57% increase over 2024 levels. This growth was specifically driven by the Rochester expansion in Nevada reaching its full design capacity of 32 million tons per year in the fourth quarter. Similarly, Hecla Mining reported 17,026,785 ounces, noting that production at its Lucky Friday mine reached a record high following its full return to operations and technical recovery earlier in the year.

Strategic Consolidation: First Majestic and Pan American

The most significant volume shift in the mid-tier sector came from First Majestic Silver, which reported a record 15,435,506 ounces. The 84% increase was almost entirely attributed to the integration of Gatos Silver. In a similar vein, Pan American Silver exceeded its annual guidance with 22,837,000 ounces, citing higher throughput rates and optimized recoveries at the Juanicipio mine as the primary catalyst for the beat.

Byproduct Power: Newmont and Southern Copper

For diversified miners, 2025 was a year of extreme fiscal efficiency. Newmont Corporation leveraged its silver byproduct output of 28,000,000 ounces to help generate a record $7.3 billion in free cash flow. Meanwhile, Southern Copper reported a 15% increase in annual silver production to 24,188,000 ounces, even as it reported a massive $3.1 billion in net income, highlighting the profitability of silver as a secondary metal in large-scale copper circuits.

Grade Pressure and Outlook

While Fresnillo PLC remains the global leader with 48,723,000 ounces, its report highlighted the challenges of maturing assets, leading to a downward revision of its 2026 production outlook despite beating gold production targets in 2025. This move signals a pivot toward grade-stabilization strategies for the coming year, a trend likely to be mirrored by other primary silver miners entering the latter half of the decade.

Sources: Fresnillo PLC, Newmont Corp, Southern Copper Corp, Pan American Silver, First Majestic Silver, Hecla Mining, Coeur Mining, Crux Investor

MiningVisuals Disclaimer: The information presented here may contain inaccuracies and is subject to rounding. We do not guarantee that all information is complete or correct. We accept no responsibility for any errors, omissions, or outcomes resulting from the use of this information. This is not investment advice.

Explore More

View All

Solar Is Silver's Largest Industrial Market, and Not Easily Replaced

Solar Is Silver's Largest Industrial Market, and Not Easily Replaced

When LONGi Green Energy, the world's largest solar module maker, told investors on January 5, 2026 that it would begin mass-producing base-metal solar cells in the second quarter, it put a number on a pressure the whole industry feels. Solar is the largest single application within silver's industrial demand, and as the metal ran to a record above $121 an ounce in January, rising silver costs pushed manufacturers to accelerate efforts to reduce the metal per cell.

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

In early 2026, the artificial intelligence narrative shifted abruptly from software capabilities to physical hardware constraints. With tech giants committing hundreds of billions to new infrastructure—pushing global hyperscaler capital expenditures past $600 billion this year—the industry has collided with a new primary bottleneck: a severe power and thermal crunch.

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Somewhere inside a pressurized-water reactor, an alloy that is four-fifths silver is absorbing neutrons to keep the core in check, a job most silver investors have never heard of. It is a useful reminder that the metal people picture as coins and jewelry mostly works elsewhere, across industry.

Ranked: The Countries That Produced the Most Silver in 2025

Ranked: The Countries That Produced the Most Silver in 2025

Mexico remained the world's top silver-producing country in 2025, mining 172.9 million ounces (Moz), roughly a fifth of global supply, according to the World Silver Survey 2026, produced for the Silver Institute by Metals Focus. But Mexico's lead narrowed: its output fell 5% for a third straight year, while second-place Peru climbed 7%. Global mine production rose 3% to 846.6 Moz, even as the ranking's top tier told a story of one leader sliding and its closest rival closing in.