Precious Metals

October 6, 2025

3 min

Precious Metals

The silver market is currently in the spotlight, with the price of the metal recently trading above $48/oz in early October 2025. This price movement occurs alongside a long-term, fundamental trend in the market: a growing supply shortage.

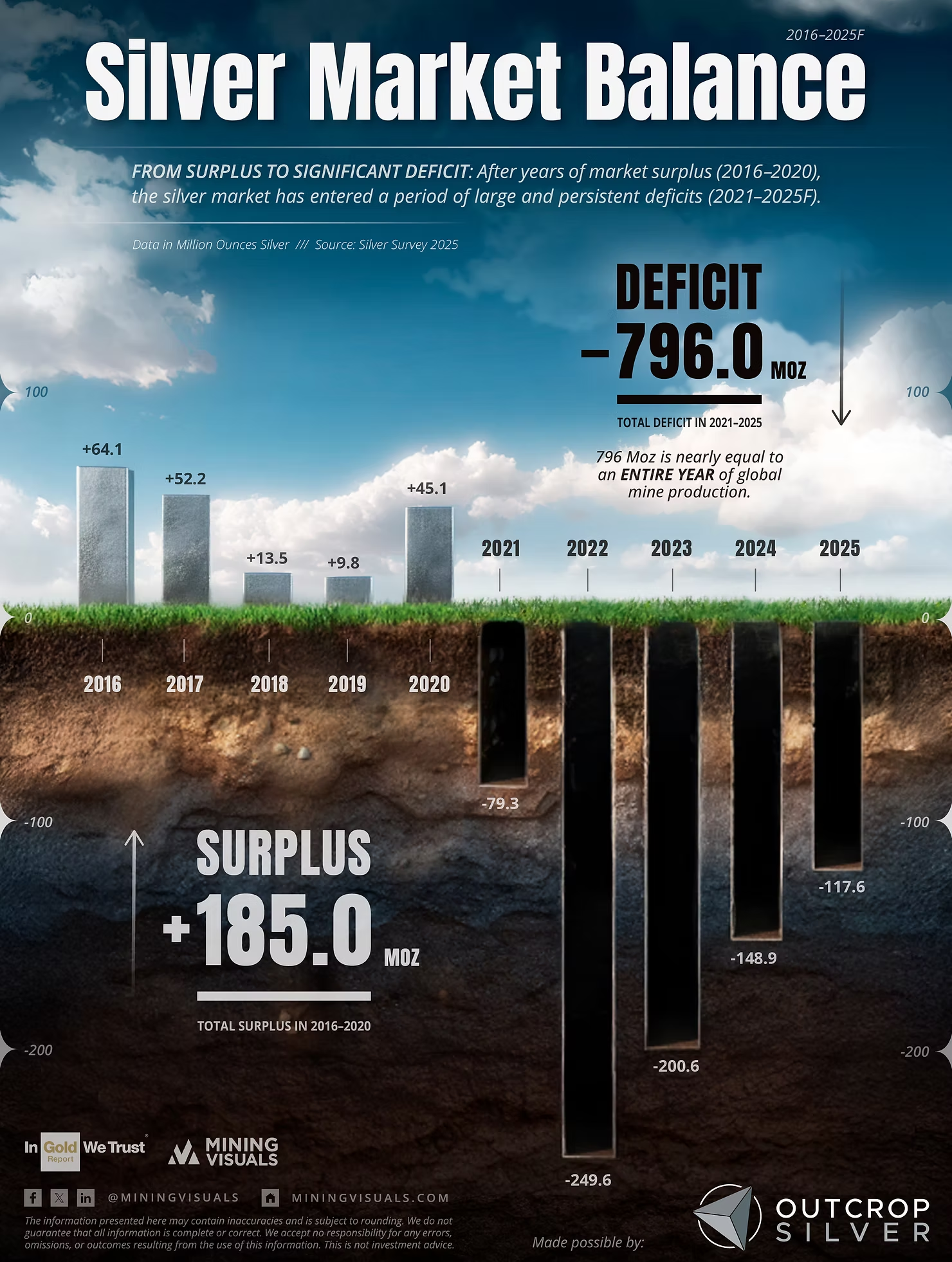

As shown in the accompanying chart, the market has been in a structural deficit—where demand exceeds supply—for five years running. According to the World Silver Survey 2025, the cumulative supply deficit from 2021 through the end of the 2025 forecast period is expected to reach 796 million ounces (Moz). This figure is nearly equivalent to one full year of global silver mine production.

The following points from the 2025 report explain the primary reasons for this ongoing deficit and the factors influencing the price:

1. Industrial Demand

The key driver for silver's market strength is its essential role in manufacturing. The 2025 Survey confirms that industrial fabrication demand reached a new all-time high in 2024.

This demand is mainly powered by:

- Photovoltaics (Solar Energy): The solar sector remains the single largest engine of industrial demand growth.

- Automotive: The increasing complexity of vehicles, especially electric vehicles (EVs) and advanced driver-assist systems, requires more silver.

- Next-Generation Electronics: The expansion of 5G infrastructure and developments in AI-related consumer electronics are also contributing to higher demand.

2. Supply Growth Remains Slow

While industrial consumption is rising quickly, the supply response has been modest. Global mine production saw only a small increase in 2024 and is not expected to keep up with the pace of demand growth. This disparity between surging industrial consumption and limited new output is the main factor tightening the market and causing these supply shortfalls.

3. Investor Interest Returns

After a period of reduced activity in Western markets, investor demand has shown a noticeable uptick in 2025. This renewed appetite is visible in the positive inflows into silver-backed ETFs, reversing the outflows of the past two years. This surge in investor interest, combined with favorable macroeconomic conditions like anticipated U.S. Federal Reserve interest rate cuts, provides a major tailwind supporting market activity.

Conclusion

The data from the World Silver Survey 2025 highlights a clear and continuing structural deficit in the silver market. The combination of record industrial usage, slow supply growth, and renewed investment interest creates a robust fundamental picture for silver, which has been reflected in the recent price movement to multi-year highs. The underlying supply-demand dynamics are key factors for market observers to consider.

Sponsored by:

Outcrop Silver is a leading explorer and developer focused on advancing its flagship Santa Ana high-grade silver project in Colombia. Leveraging a disciplined and seasoned team of professionals with decades of experience in the region. Outcrop Silver is dedicated to expanding current mineral resources through strategic exploration initiatives.

At the core of our operations is a commitment to responsible mining practices and community engagement, underscoring our approach to sustainable development. Our expertise in navigating complex geological and market conditions enables us to consistently identify and capitalize on opportunities to enhance shareholder value.

With a deep understanding of the Colombian mining landscape and a track record of successful exploration, Outcrop Silver is poised to transform the Santa Ana project into a significant silver producer, contributing positively to the local economy and setting new standards in the mining industry.

Learn more about Outcrop Silver at https://outcropsilver.com/

Source: World Silver Survey 2025, The Silver Institute

Disclaimer: This infographic and accompanying article are provided for informational and illustrative purposes only and should not be construed as financial, investment, or professional advice. They are not an offer to sell or a solicitation to buy any securities. Investing in precious metals and securities involves inherent risks, including the risk of loss, and past performance is not indicative of future results. Market data, statistics, and analysis are based on publicly available information from third-party sources believed to be reliable, but their accuracy and completeness cannot be guaranteed. Readers should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions.

Explore More

View All

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

In early 2026, the artificial intelligence narrative shifted abruptly from software capabilities to physical hardware constraints. With tech giants committing hundreds of billions to new infrastructure—pushing global hyperscaler capital expenditures past $600 billion this year—the industry has collided with a new primary bottleneck: a severe power and thermal crunch.

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Somewhere inside a pressurized-water reactor, an alloy that is four-fifths silver is absorbing neutrons to keep the core in check, a job most silver investors have never heard of. It is a useful reminder that the metal people picture as coins and jewelry mostly works elsewhere, across industry.

Ranked: The Countries That Produced the Most Silver in 2025

Ranked: The Countries That Produced the Most Silver in 2025

Mexico remained the world's top silver-producing country in 2025, mining 172.9 million ounces (Moz), roughly a fifth of global supply, according to the World Silver Survey 2026, produced for the Silver Institute by Metals Focus. But Mexico's lead narrowed: its output fell 5% for a third straight year, while second-place Peru climbed 7%. Global mine production rose 3% to 846.6 Moz, even as the ranking's top tier told a story of one leader sliding and its closest rival closing in.

Electric Vehicles Are Set to Become the Auto Industry's Biggest Silver Consumer by 2027

Electric Vehicles Are Set to Become the Auto Industry's Biggest Silver Consumer by 2027

Most of silver's 2026 story has been told from the supply side: a sixth straight year of structural deficit and a record price near $121 in January. Less examined is where the next leg of industrial demand actually comes from. With solar, silver's largest industrial use, now facing thrifting and substitution, the Silver Institute points to a quieter end-use picking up the slack: the automotive sector. A December 2025 study from Oxford Economics and the Silver Institute quantifies that shift, and the engine behind it is the electric vehicle.