Precious Metals

July 24, 2025

3 min

Precious Metals

In our recent overview, "Silver Market 2025: Supply, Demand & Deficit Projections," we explored the structural supply deficit that has come to define the modern silver market. This article complements that macro view by taking a detailed look at the engine driving this trend: the dramatic shifts within global silver demand.

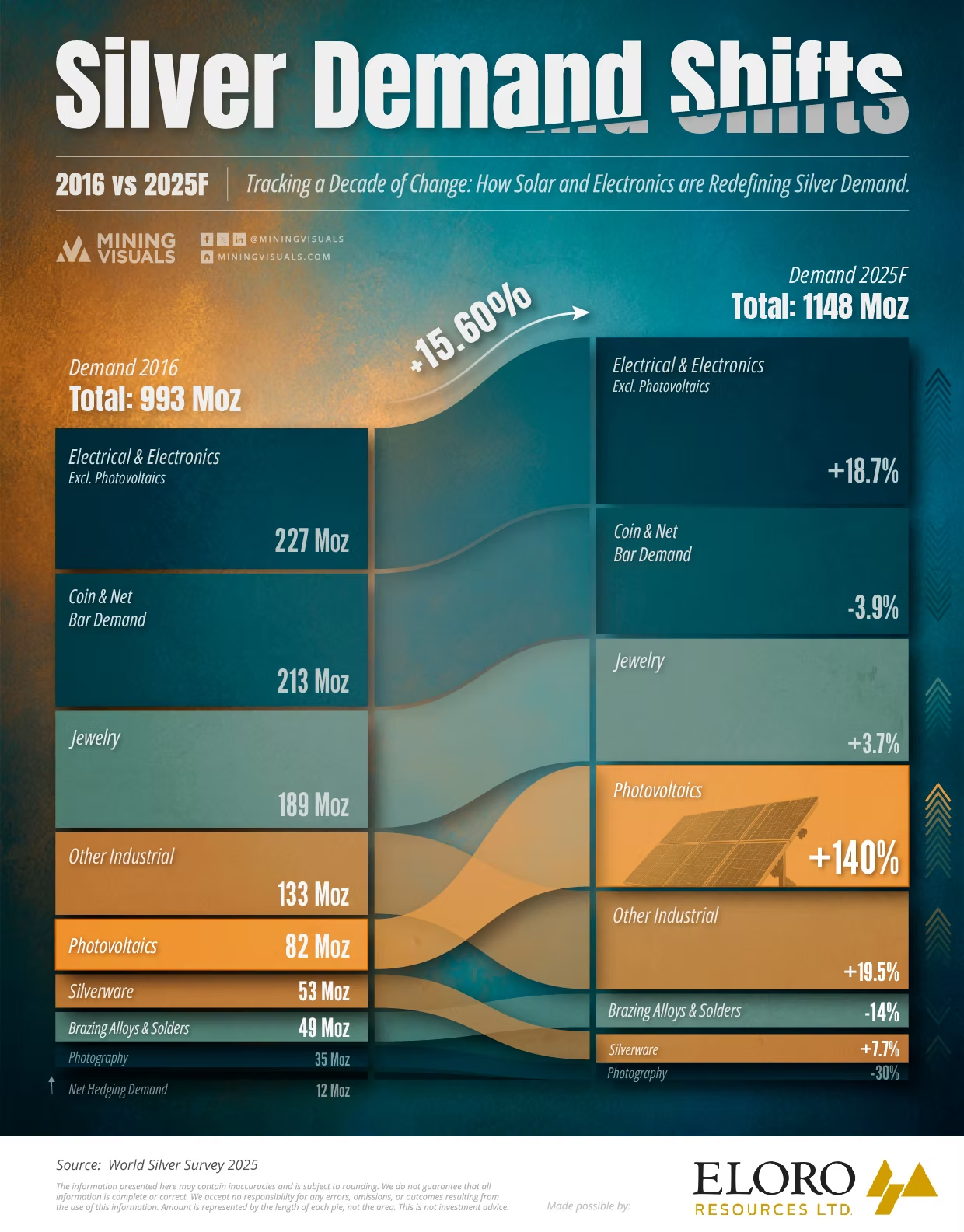

Silver's role in the global economy is evolving significantly, as illustrated in our latest infographic. Data from the World Silver Survey 2025, presented in the infographic, indicates that total silver demand is projected to grow by +15.60%, from 993 million ounces (Moz) in 2016 to a forecast 1,148 Moz by 2025.

Beyond this overall growth, the composition of silver demand is undergoing a notable realignment. This article examines these shifts in more detail, providing context to the numbers and exploring the forces reshaping silver's applications.

Key Growth Drivers: Photovoltaics and Electronics

Two sectors are particularly prominent in driving the changes in silver demand:

- Photovoltaics (Solar Power): Silver demand from solar applications is forecast to show substantial growth of +140% between 2016 and 2025F, increasing from 81.6 Moz to a projected 195.7 Moz. This significant growth, as detailed in the World Silver Survey 2025, is a direct result of the global expansion of renewable energy. Silver's high electrical conductivity makes it an essential material in the photovoltaic cells that convert sunlight into electricity.

- Electrical & Electronics (excluding PV): This traditionally large sector for silver demand continues to show consistent growth, with a projected +18.7% increase. Demand is forecast to rise from 227 Moz in 2016 to 269.5 Moz by 2025F. Applications such as consumer electronics, advanced automotive systems, 5G technology, and the Internet of Things (IoT) all utilize silver for components like contacts and circuitry.

Traditional Demand Segments: Varied Trends

Silver's more traditional applications are exhibiting varied trends, according to World Silver Survey 2025 data:

- Jewelry: The jewelry sector is expected to see modest growth of +3.7%, with demand rising from 189 Moz in 2016 to approximately 196.0 Moz by 2025F. This suggests a relatively stable consumer interest in various global markets.

- Coin & Net Bar Demand (Investment): Physical silver investment is projected for a slight decrease of -3.9% from its 2016 level of 213 Moz, to a forecast 204.7 Moz in 2025F. This segment is typically influenced by investor sentiment and broader economic conditions.

Other Industrial and Legacy Applications: Evolving Demand

The broader industrial category and some legacy uses also show distinct shifts:

- The "Other Industrial" segment (which stood at 133 Moz in 2016) is forecast to grow by +19.5% overall by 2025F.

- Within more specific industrial applications:

- Brazing Alloys & Solders (non-electronic industrial) are projected to grow by +7.7% from their 49 Moz base in 2016 (to ~52.8 Moz by 2025F).

- Photography, historically a notable silver consumer, is expected to see demand fall further by -30% from 35 Moz in 2016 (to ~24.5 Moz), due to the prevalence of digital imaging.

The period from 2016 to 2025F is clearly transforming silver's demand landscape. This growth in industrial applications, particularly in the solar and electronics sectors, is the primary reason for the overall market deficit.

Sponsored by:

Eloro Resources Ltd. is a mineral exploration company advancing a world-class silver and tin project in Bolivia’s historic Potosí Department. Its flagship asset, the Iska Iska Project, ranks among the top five undeveloped global resources in terms of scale for both tin and silver.

This significant grassroots discovery remains open in multiple directions, offering substantial potential for continued expansion and resource enhancement. Iska Iska benefits from strong infrastructure access and a deeply rooted presence in Bolivia, supported by an experienced management team and meaningful community engagement.

Eloro’s strategy is focused on resource growth, strategic partnerships, and establishing a leading position within the global mining sector.

Learn more at elororesources.com.

Disclaimer: The information provided in this article and the accompanying infographic is for informational purposes only and should not be considered as financial or investment advice. While MiningVisuals has made every effort to ensure the accuracy and reliability of the information presented, which is based on the sources cited, we do not guarantee its completeness or accuracy. Market forecasts, projections, and analyses are based on data available at the time of publication and are inherently subject to change due to various factors. Readers are encouraged to conduct their own research and consult with a qualified financial advisor before making any investment decisions.

Sources:

- World Silver Survey 2025. (Data from this survey is referenced and utilized within the MiningVisuals "Silver Demand Shifts 2016 vs 2025F" infographic and this analysis).

Explore More

View All

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

In early 2026, the artificial intelligence narrative shifted abruptly from software capabilities to physical hardware constraints. With tech giants committing hundreds of billions to new infrastructure—pushing global hyperscaler capital expenditures past $600 billion this year—the industry has collided with a new primary bottleneck: a severe power and thermal crunch.

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Somewhere inside a pressurized-water reactor, an alloy that is four-fifths silver is absorbing neutrons to keep the core in check, a job most silver investors have never heard of. It is a useful reminder that the metal people picture as coins and jewelry mostly works elsewhere, across industry.

Ranked: The Countries That Produced the Most Silver in 2025

Ranked: The Countries That Produced the Most Silver in 2025

Mexico remained the world's top silver-producing country in 2025, mining 172.9 million ounces (Moz), roughly a fifth of global supply, according to the World Silver Survey 2026, produced for the Silver Institute by Metals Focus. But Mexico's lead narrowed: its output fell 5% for a third straight year, while second-place Peru climbed 7%. Global mine production rose 3% to 846.6 Moz, even as the ranking's top tier told a story of one leader sliding and its closest rival closing in.

Electric Vehicles Are Set to Become the Auto Industry's Biggest Silver Consumer by 2027

Electric Vehicles Are Set to Become the Auto Industry's Biggest Silver Consumer by 2027

Most of silver's 2026 story has been told from the supply side: a sixth straight year of structural deficit and a record price near $121 in January. Less examined is where the next leg of industrial demand actually comes from. With solar, silver's largest industrial use, now facing thrifting and substitution, the Silver Institute points to a quieter end-use picking up the slack: the automotive sector. A December 2025 study from Oxford Economics and the Silver Institute quantifies that shift, and the engine behind it is the electric vehicle.