Precious Metals

June 10, 2025

2 min

Precious Metals

The global silver market is on track for a 117.7 million ounce (Moz) deficit this year, according to data from the World Silver Survey 2025, visualized in our latest infographic. This marks a significant period of market tightness. While robust demand (detailed in our main analysis here) tells one side of the story, a closer look at the supply landscape reveals critical, contrasting trends shaping silver's availability in 2025.

Mine Production: A Long-Term Contraction

Global silver mines are projected to yield 835 Moz in 2025. This output signifies a 7.23% decrease compared to 2016 levels, based on World Silver Survey 2025 data. Such a long-term decline in primary silver supply points to persistent challenges within the mining sector.

Industry analyses, including reports like the World Silver Survey, indicate these can stem from factors such as the maturation of major orebodies, shifting capital investment cycles, the extended timelines required for new mine development, fluctuating operational costs, and evolving regulatory environments in key silver-producing nations. This decrease from mining operations is a crucial factor in this year's overall market deficit.

Recycling Ramps Up, Offering Partial Relief

In contrast to falling mine output, silver recycling is experiencing a significant uptick. Projections from the World Silver Survey 2025 data show an anticipated 195 Moz from secondary sources in 2025, a notable increase of 24.06%. This rise in recycled volumes is often linked to improved efficiencies in collecting and processing end-of-life silver-bearing products, particularly industrial and electronic scrap. Supportive silver prices can also incentivize the flow of materials back into the supply chain. While this growth in recycling provides an important contribution, its overall volume is still considerably smaller than primary mine production.

The Bottom Line: A Persistent Market Imbalance

Despite the commendable growth in recycling, the increase from these secondary sources is not projected to fully offset the decrease in mine production and meet total global demand. The interplay of these supply dynamics—reduced primary output and increased, yet insufficient, recycling—is a key reason for the forecast market deficit in 2025.

Sponsored by:

Eloro Resources Ltd. is a mineral exploration company advancing a world-class silver and tin project in Bolivia’s historic Potosí Department. Its flagship asset, the Iska Iska Project, ranks among the top five undeveloped global resources in terms of scale for both tin and silver.

This significant grassroots discovery remains open in multiple directions, offering substantial potential for continued expansion and resource enhancement. Iska Iska benefits from strong infrastructure access and a deeply rooted presence in Bolivia, supported by an experienced management team and meaningful community engagement.

Eloro’s strategy is focused on resource growth, strategic partnerships, and establishing a leading position within the global mining sector.

Learn more at elororesources.com.

Sources: World Silver Survey 2025, published by The Silver Institute. Infographic by MiningVisuals.

Disclaimer: This analysis is based on data and projections sourced from the World Silver Survey 2025. While we believe the information to be reliable, we do not guarantee its accuracy or completeness. The views and forecasts expressed are subject to change without notice. This article is intended for general informational purposes and does not constitute financial or investment advice. Market conditions, including supply, demand, and prices, can fluctuate.

Explore More

View All

Ghana's Gold Mining Landscape: A Story Written in Ancient Rock

Ghana's Gold Mining Landscape: A Story Written in Ancient Rock

Ghana is one of the world's most significant gold-producing countries, and in 2025 it remained the largest in Africa, with national output reaching about 6 million ounces. But the numbers are only the surface. Ghana's gold reaches back more than two billion years into the rock beneath it, shaped by ancient mountain-building forces and worked by human hands for well over a century.

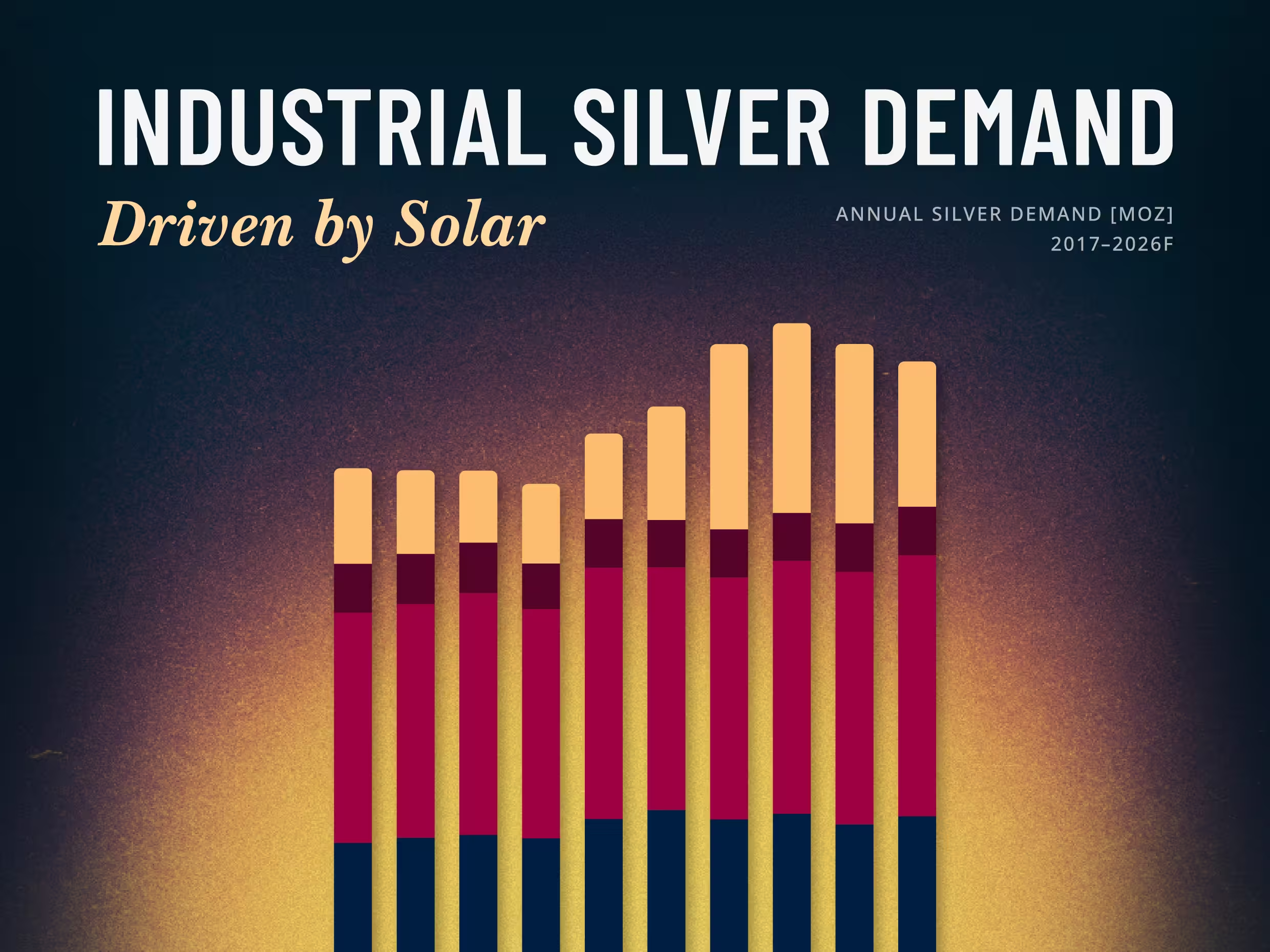

Solar Is Silver's Largest Industrial Market, and Not Easily Replaced

Solar Is Silver's Largest Industrial Market, and Not Easily Replaced

When LONGi Green Energy, the world's largest solar module maker, told investors on January 5, 2026 that it would begin mass-producing base-metal solar cells in the second quarter, it put a number on a pressure the whole industry feels. Solar is the largest single application within silver's industrial demand, and as the metal ran to a record above $121 an ounce in January, rising silver costs pushed manufacturers to accelerate efforts to reduce the metal per cell.

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

Silver in the Data Center: How AI's Power Crunch Is Building a New Pillar of Industrial Demand

In early 2026, the artificial intelligence narrative shifted abruptly from software capabilities to physical hardware constraints. With tech giants committing hundreds of billions to new infrastructure—pushing global hyperscaler capital expenditures past $600 billion this year—the industry has collided with a new primary bottleneck: a severe power and thermal crunch.

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Somewhere inside a pressurized-water reactor, an alloy that is four-fifths silver is absorbing neutrons to keep the core in check, a job most silver investors have never heard of. It is a useful reminder that the metal people picture as coins and jewelry mostly works elsewhere, across industry.