Precious Metals

September 25, 2025

3 min

Precious Metals

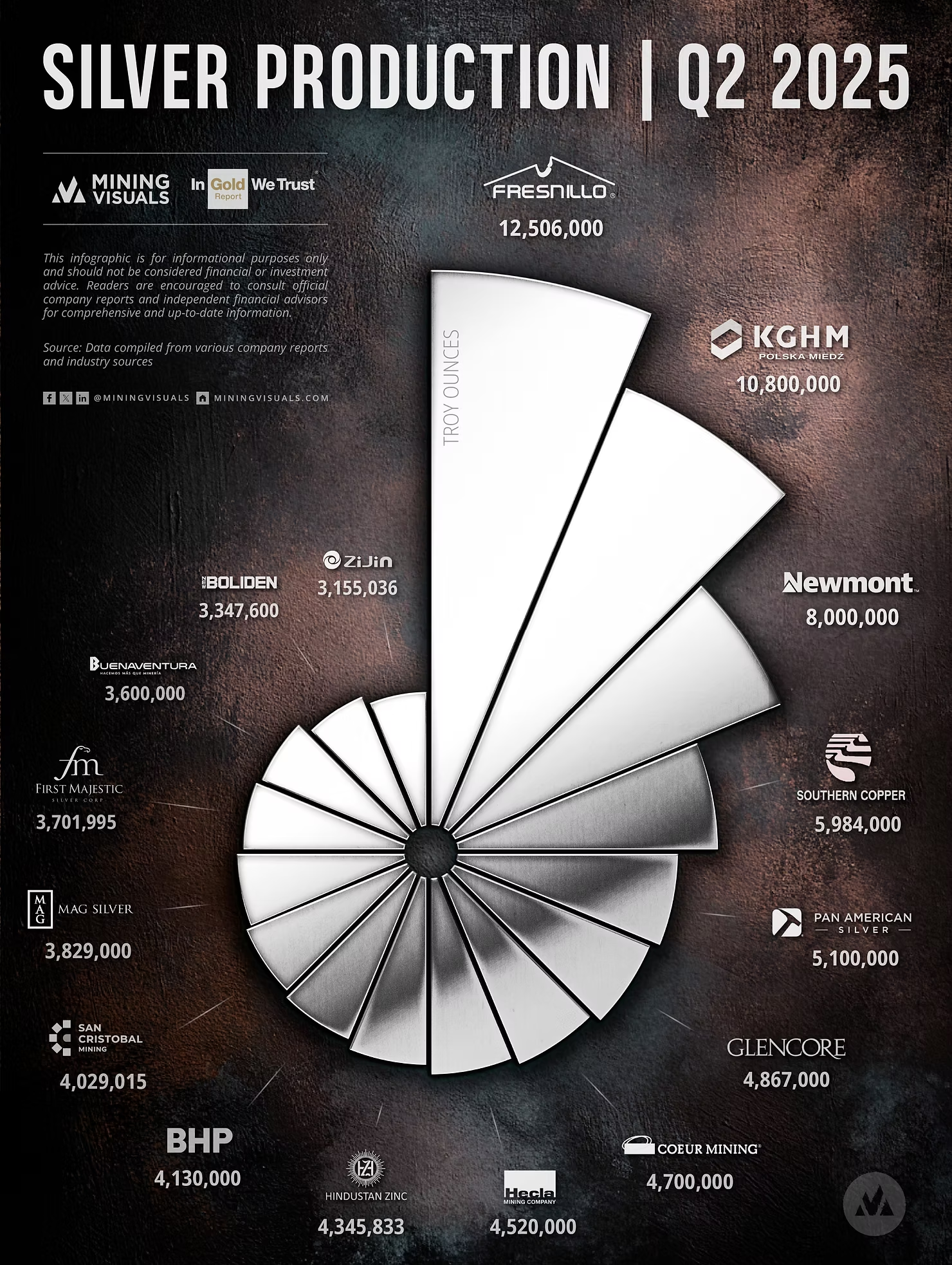

The silver market remained robust in Q2 2025, with strong prices benefiting the entire sector. However, company production results show a clear divide between miners successfully executing on their operational plans and those navigating challenges. The quarter's results were not driven by market sentiment, but by on-the-ground factors ranging from successful mine ramp-ups to planned maintenance and grade variability. This analysis compares Q2 2025 production results with those from the same quarter last year.

How the Top Producers Fared

- Fresnillo Plc (-14.66%): The world's top producer reported output of 12,506,000 ounces. The primary drivers were the planned cessation of mining at the San Julián Disseminated Ore Body and a significant labor strike at the Tizapa mine. Additionally, lower silver grades in the ore processed at the Fresnillo and Ciénega mines contributed to the reduced output, yielding less silver per tonne of material.

- KGHM Polska Miedz (-7.21%): As a primary copper producer, KGHM's silver output is a byproduct. The company's 7.21% drop to 10,800,000 ounces was primarily due to a planned maintenance shutdown at its Głogów II Copper Smelter and Refinery. Because silver is recovered as a by-product of copper processing, this temporary halt in operations directly reduced the total silver output.

- Newmont Corporation (Negligible Change): The gold giant's silver production remained nearly flat, registering a negligible change at approximately 8,000,000 ounces. This steady output was a direct result of planned mine sequencing at its Peñasquito mine in Mexico. While the company successfully processed ore with higher gold grades, a deliberate move to a different area of the pit meant the ore contained less silver compared to the previous year. This balanced performance underscores the company's long-term strategy for managing the complex, polymetallic deposit.

Growth Leaders: Ramping Up and Exceeding Plans

- Coeur Mining Inc. (+80.77%): Coeur posted the most dramatic growth, with production surging 80.77% to 4,700,000 ounces. This increase was largely driven by strong performance at its Rochester mine in Nevada. The increase reflects the successful ramp-up of the new Plan of Operations Amendment 11 (POA 11), leading to higher stacking and processing rates on the new Stage VI leach pad.

- First Majestic Silver Corp. (+75.94%): First Majestic's impressive 75.94% production increase to 3,701,995 ounces was primarily due to higher-grade ore from the Ermitaño mine feeding the Santa Elena mill. This, combined with improved recovery rates and increased throughput at the San Dimas mine following key operational upgrades, significantly boosted overall silver production.

Headwinds and Strategic Shifts

Conversely, the largest production decreases were the result of specific, planned operational events:

- MAG Silver Corp (-23.42%): The significant 23.42% drop in production to 3,829,000 ounces. The decline in silver production in the second quarter of 2025 was attributed to planned mine sequencing at the Juanicipio project. The change was due to the processing of ore with a lower average silver grade, an expected variation consistent with the operator's (Fresnillo) long-term mine plan.

- Zijin Mining (-17.36%): Zijin's 17.36% decrease was a result of a strategic decision at its Čukaru Peki mine in Serbia. The company intentionally processed lower-grade polymetallic ore during the quarter to prioritize a waste-stripping campaign that will provide better access to the high-grade copper-gold zones later in the year.

As producers head into the second half of 2025, their ability to deliver on mine plans and manage operational complexities will continue to be the primary driver of shareholder value.

Source: Data compiled from various company reports and industry sources

This content is for informational purposes only and should not be considered financial or investment advice. Readers are encouraged to consult official company reports and independent financial advisors for comprehensive and up-to-date information.

Explore More

View All

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Silver's Use Cases: A Visual Guide to Where the Metal Actually Goes

Somewhere inside a pressurized-water reactor, an alloy that is four-fifths silver is absorbing neutrons to keep the core in check, a job most silver investors have never heard of. It is a useful reminder that the metal people picture as coins and jewelry mostly works elsewhere, across industry.

Ranked: The Countries That Produced the Most Silver in 2025

Ranked: The Countries That Produced the Most Silver in 2025

Mexico remained the world's top silver-producing country in 2025, mining 172.9 million ounces (Moz), roughly a fifth of global supply, according to the World Silver Survey 2026, produced for the Silver Institute by Metals Focus. But Mexico's lead narrowed: its output fell 5% for a third straight year, while second-place Peru climbed 7%. Global mine production rose 3% to 846.6 Moz, even as the ranking's top tier told a story of one leader sliding and its closest rival closing in.

Electric Vehicles Are Set to Become the Auto Industry's Biggest Silver Consumer by 2027

Electric Vehicles Are Set to Become the Auto Industry's Biggest Silver Consumer by 2027

Most of silver's 2026 story has been told from the supply side: a sixth straight year of structural deficit and a record price near $121 in January. Less examined is where the next leg of industrial demand actually comes from. With solar, silver's largest industrial use, now facing thrifting and substitution, the Silver Institute points to a quieter end-use picking up the slack: the automotive sector. A December 2025 study from Oxford Economics and the Silver Institute quantifies that shift, and the engine behind it is the electric vehicle.

Silver Market Balance: A 2026 Update

Silver Market Balance: A 2026 Update

For the fifth year running, the world used more silver than it produced in 2025, and the World Silver Survey 2026 expects 2026 to extend that streak to six. The report, released in April by the Silver Institute and researched by the London consultancy Metals Focus, pegs the 2025 deficit at 40.3 million ounces and forecasts a wider gap of 46.3 million ounces this year. Each shortfall draws on above-ground stocks, leaving less metal readily available even as total inventories have held up.