Tin

May 27, 2025

1 min

Tin

The following content is sponsored by Eloro Resources

Tin. It's the hidden hero in your smartphone, a key player in the green energy revolution, and a critical component in countless modern technologies. But as demand surges, the world is waking up to a stark reality: the global tin supply is heavily concentrated.

Our latest infographic highlights this concentration and this article digs deeper into the topic, exploring Asia's production powerhouse and why the world is increasingly looking towards supply diversification.

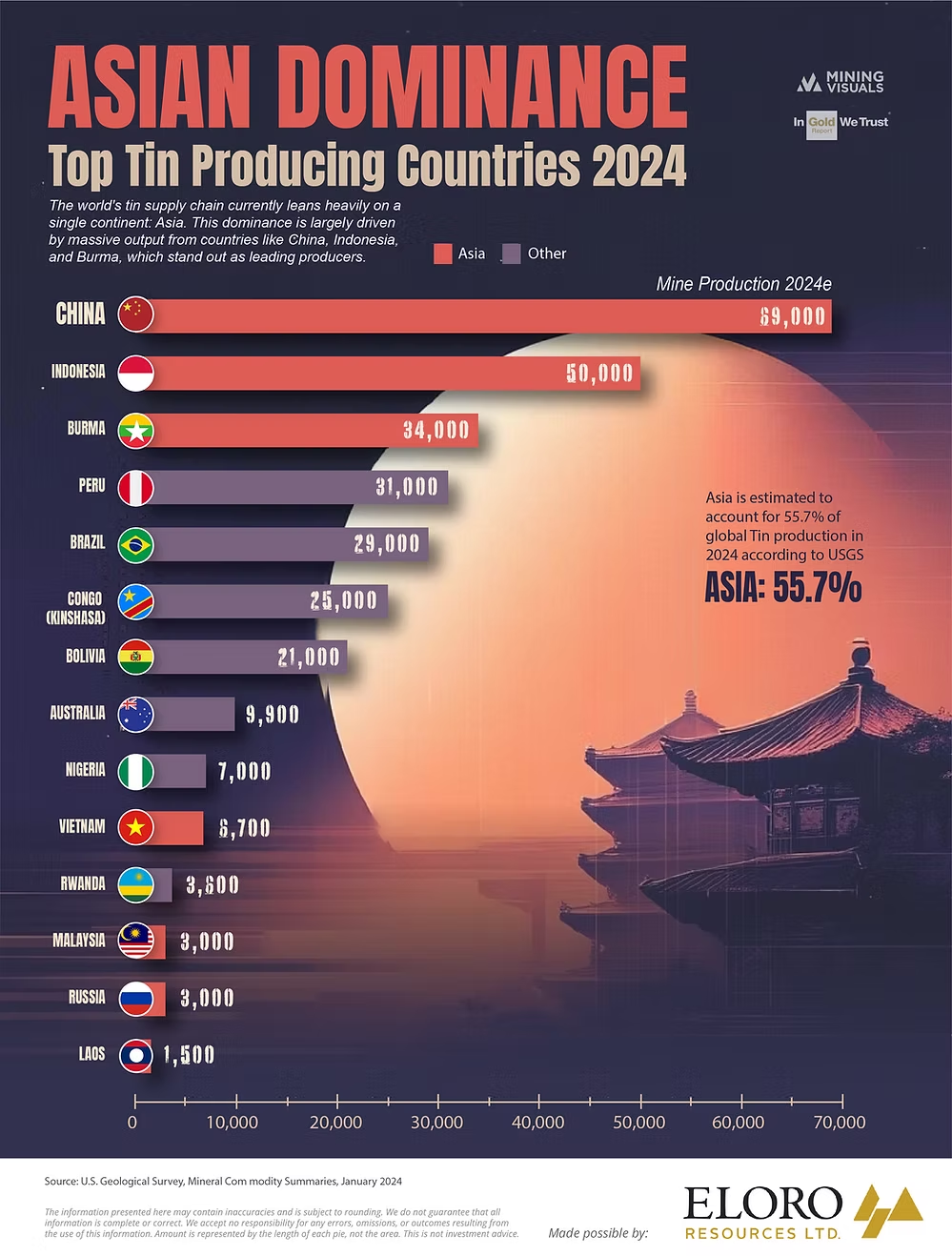

Asia: The Undisputed Tin Capital

When it comes to tin mining, Asia is in the driver's seat. In 2024, the continent was responsible for an estimated 55.7% of the world's entire mine output, according to the U.S. Geological Survey. This isn't just a slight lead; it's a commanding position primarily built on the output of three nations:

- China: The world's top producer by a significant margin. The engine behind this output is largely the Yunnan Tin Company Group (YTC), one of the largest and most integrated tin producers globally, with sprawling operations in Yunnan province.

- Indonesia: A global tin giant, with state-controlled PT Timah Tbk leading extensive mining activities, both onshore and via offshore dredging, around the historic tin islands of Bangka and Belitung.

- Myanmar: A major regional supplier, with substantial production coming from the Man Maw mining area (often called the 'Wa Mine') in Wa State, a key source of tin concentrate, especially for smelters in China.

While other Asian countries like Vietnam, Malaysia, and Laos contribute, these three, along with their flagship operations, form the bedrock of global tin supply. (For precise 2024 production figures from these entities, industry reports from the International Tin Association (ITA) and others provide detailed breakdowns).

The Rest of the World: A Smaller Slice of the Pie

Compared to Asia's output, production from other regions is notably smaller. Key players include:

- South America: Led by Peru, Brazil, and Bolivia.

- Africa: With contributions from Congo (Kinshasa), Nigeria, and Rwanda.

- Oceania: Primarily Australia.

Collectively, these regions make up the balance, but no single country outside Asia currently rivals the output of the top Asian producers. Adding another layer to this, Asia isn't just a production hub; it's also a major consumer of tin, especially within its vast electronics manufacturing industry.

Why Concentration Matters: The Push for a Diversified Supply

This heavy geographic concentration, while showcasing Asia's production capabilities, isn't without potential challenges for the global supply chain. As our infographic touches upon, reliance on a few key regions can expose the market to risks:

- Geopolitical Instability: Regional conflicts or political shifts can disrupt mining and export activities.

- Policy Changes: National decisions on export quotas, taxes, or environmental regulations can quickly alter supply dynamics.

- Logistical Hurdles: Interruptions to shipping or infrastructure can create bottlenecks.

Given tin's vital role in everything from a simple solder joint to advanced solar panels and batteries, ensuring a resilient and secure global supply is becoming a top priority.

This is why developing new tin projects and supporting operations in diverse regions like South America, Africa, and Oceania is gaining traction. A more geographically spread-out supply chain is increasingly seen as crucial for global industries to confidently meet future demand and navigate a complex world.

Sponsored by:

Eloro Resources Ltd. is a mineral exploration company advancing a world-class silver and tin project in Bolivia’s historic Potosí Department. Its flagship asset, the Iska Iska Project, ranks among the top five undeveloped global resources in terms of scale for both tin and silver.

This significant grassroots discovery remains open in multiple directions, offering substantial potential for continued expansion and resource enhancement. Iska Iska benefits from strong infrastructure access and a deeply rooted presence in Bolivia, supported by an experienced management team and meaningful community engagement.

Eloro’s strategy is focused on resource growth, strategic partnerships, and establishing a leading position within the global mining sector.

Learn more at elororesources.com.

Disclaimer: The information provided in this article and the accompanying infographic is for informational purposes only and should not be considered as financial or investment advice. While MiningVisuals has made every effort to ensure the accuracy and reliability of the information presented, which is based on the sources cited, we do not guarantee its completeness or accuracy. Market forecasts, projections, and analyses are based on data available at the time of publication and are inherently subject to change due to various factors. Readers are encouraged to conduct their own research and consult with a qualified financial advisor before making any investment decisions.

Sources:

- Energy News / Oedigital. (2025, April 2). "The tin market is nearing a three-year high on tightness and short-covering." (Referenced for general market conditions context in the infographic's sub-headline).

- International Tin Association (ITA). (Covering 2023/2024). Reports and surveys. (General reference for detailed industry data and analysis on production/consumption).

- U.S. Geological Survey (USGS). (Covering 2024). Mineral Commodity Summaries / Reports. (Referenced for global production percentages).

Explore More

View All

Three Weeks Public, SpaceX Already Approaches the Value of Every Listed Miner on Earth

Three Weeks Public, SpaceX Already Approaches the Value of Every Listed Miner on Earth

For 24 years SpaceX stayed private. Then, on June 12, 2026, it began trading on the Nasdaq in the largest IPO in history, priced at a $1.77 trillion valuation. Barely three weeks later the rocket and satellite maker is worth even more. As of early July, SpaceX carried a market capitalization of about $2.1 trillion, the seventh-highest of any public company on Earth, and it joins the Nasdaq-100 on July 7

Mapped: Zinc's Use Across Five Industries and the 2030 Demand Outlook

Mapped: Zinc's Use Across Five Industries and the 2030 Demand Outlook

We've covered zinc's role in energy, health, and sustainability before, alongside the supply base concentrated in a handful of mega-mines and the production map that has shifted toward Asia since the mid-1990s. The story of 2025 is what changed on the demand side. In November, the U.S. Geological Survey retained zinc on its final 2025 List of Critical Minerals.

Lithium Use Cases: Batteries Now Consume 88% of Global Supply

Lithium Use Cases: Batteries Now Consume 88% of Global Supply

In February 2026, the U.S. Geological Survey put a fresh number on a transformation that has been building for a decade: batteries now account for 88% of global lithium end-use, up from 87% a year earlier. The metal that once quietly toughened ceramics and thickened industrial greases has been almost entirely repurposed by the battery economy. As covered in our reporting on the shift from surplus to deficit, the supply side of this story is tightening.

Sort First, Grind Later: The sensor technology reshaping polymetallic processing

Sort First, Grind Later: The sensor technology reshaping polymetallic processing

Sensor-based sorting lets miners reject barren rock before it's ever crushed, saving energy, water, and tailings volume at industrial scale. Polymetallic deposits, the orebodies that carry multiple economically valuable metals in a single rock, present a distinctive processing challenge: the valuable minerals are locked together with each other and with vast volumes of barren rock, demanding both heavy grinding and complex multi-stage separation.